Card deposits are still a workhorse for online casinos, but the moment you scale across geos, acquire aggressively, or run high-velocity campaigns, your card stack starts living on a knife edge: approval rate vs fraud loss vs player friction.

3-D Secure (3DS) sits right in the middle of that trade-off. Used well, it can unlock approvals, reduce chargebacks, and keep you compliant in Strong Customer Authentication (SCA) markets. Used poorly, it can tank first-time deposit conversion, especially on mobile.

This guide breaks down when 3DS for casino deposits helps, when it hurts, and how to deploy it as a risk-based tool instead of a blanket rule.

What 3DS actually does in a casino deposit

3DS is a cardholder authentication protocol (EMV 3-D Secure, often “3DS2”) that lets an issuer confirm the person attempting a deposit is the legitimate cardholder. In practical terms, it adds an extra decision step between “player clicks deposit” and “funds credited.”

In a typical 3DS2 flow:

- Your payment gateway or PSP requests authentication from the issuer’s Access Control Server (ACS).

- The issuer either returns a frictionless authentication (no challenge shown) or triggers a challenge (OTP, banking app approval, biometrics).

- The resulting authentication data is attached to the authorization request.

For iGaming operators, 3DS is rarely “just a security feature.” It is a commercial lever that changes:

- Approval rates (some issuers approve more readily after successful authentication)

- Chargeback exposure (liability can shift depending on scenario and rules)

- UX and time-to-credit (especially when challenges occur)

- Compliance posture in regulated markets

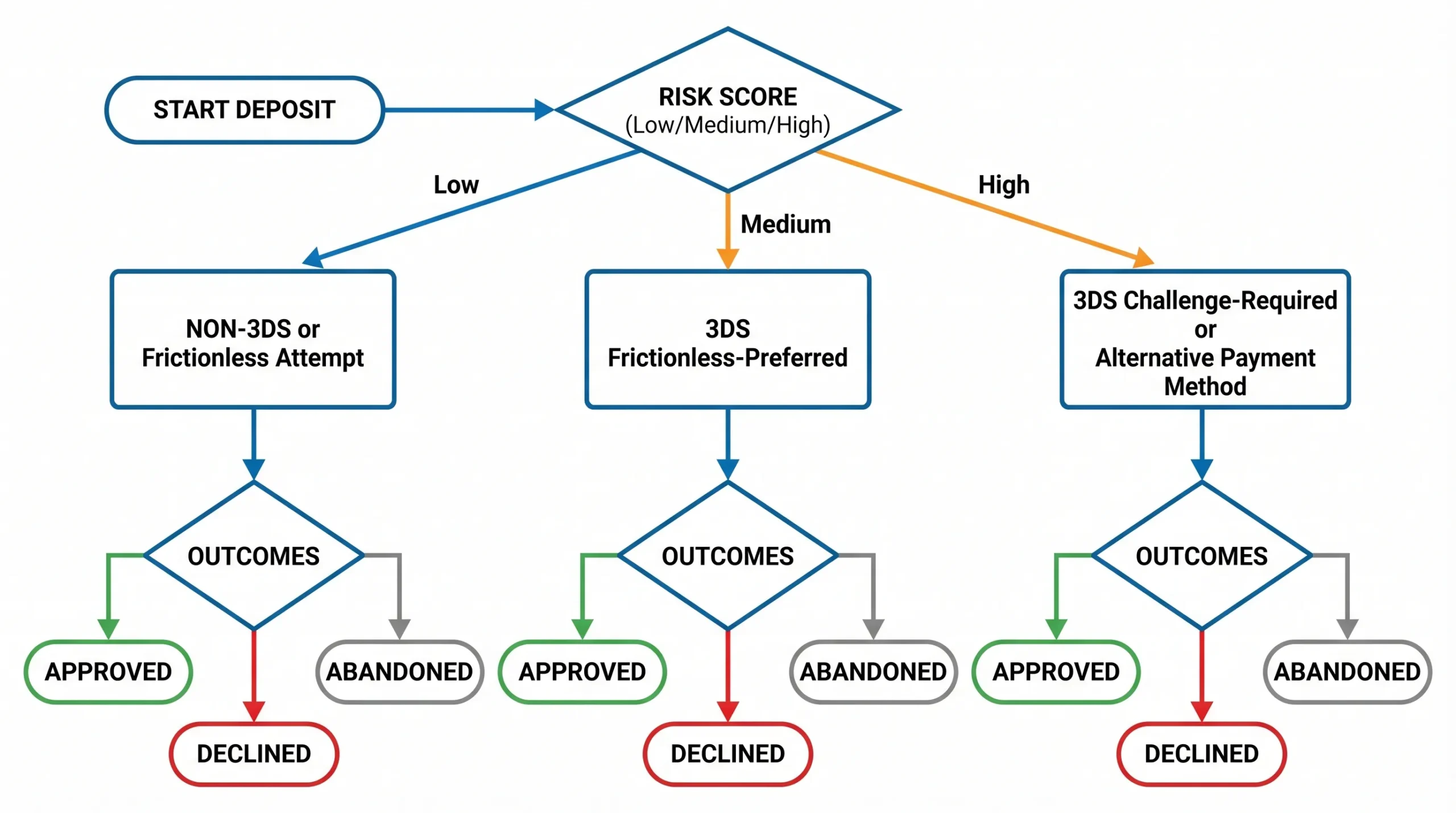

The two outcomes that matter: frictionless vs challenge

If your team treats 3DS as binary (on/off), you will almost always end up with unnecessary friction. The real question is: how often will your deposits go challenge and what is the completion rate when they do?

Challenge frequency varies by issuer, country, device, transaction pattern, and your risk settings. A casino with heavy cross-border card traffic and high velocity will see more challenges than a local, returning-player heavy brand.

When 3DS helps casino deposits

1) You operate in SCA-heavy markets (or sell into them)

In the EEA and UK, SCA rules have made issuer expectations much stricter for many online card-not-present transactions. For regulated operators, 3DS can be the cleanest path to satisfying authentication expectations.

Even outside Europe, more issuers are effectively using “SCA-like” risk signals. If you see a pattern of issuer declines that improve when authentication data is present, 3DS becomes a revenue tool, not just a compliance checkbox.

2) Your chargeback rate is limiting scale

Chargebacks are not just a loss line. They threaten:

- your PSP relationship

- your card scheme monitoring exposure

- your ability to add new acquirers or expand geos

3DS can reduce “friendly fraud” disputes where the cardholder claims they did not authorize the deposit, because authentication strengthens your evidence position.

Important nuance: liability shift and dispute outcomes depend on the exact scenario and scheme rules, and they can differ by region and transaction type. You should treat 3DS as a way to improve dispute defensibility, not as a guarantee you are immune.

3) You acquire aggressively from “cold” traffic

Paid media and affiliate traffic that pushes high volumes of first-time depositors tends to come with:

- less issuer trust (new merchant, cross-border, inconsistent device fingerprints)

- higher fraud attempt pressure

- more mismatches (IP vs BIN country, billing data gaps)

In these cohorts, a step-up to 3DS for higher-risk attempts can keep approvals stable without opening the fraud floodgates.

4) You see heavy cross-border card usage

Cross-border card deposits are a classic recipe for issuer caution. If you are routing traffic to an acquiring setup that the issuer already “likes,” you may not need 3DS. But when issuer trust is lower, authentication can be the difference between a soft decline and an approval.

5) You need a controlled response to card-testing or high-velocity attacks

When card-testing hits (many small authorizations, repeated declines, abnormal velocity), operators often respond by tightening fraud rules in ways that also block legitimate players.

A more surgical approach is:

- block obvious bot patterns

- step-up suspicious, human-like attempts to 3DS

- divert the rest to alternative rails

Done right, 3DS becomes part of a layered defense that protects approval rate for legitimate traffic.

When 3DS hurts casino deposits

1) You are optimizing first-time deposit conversion on mobile

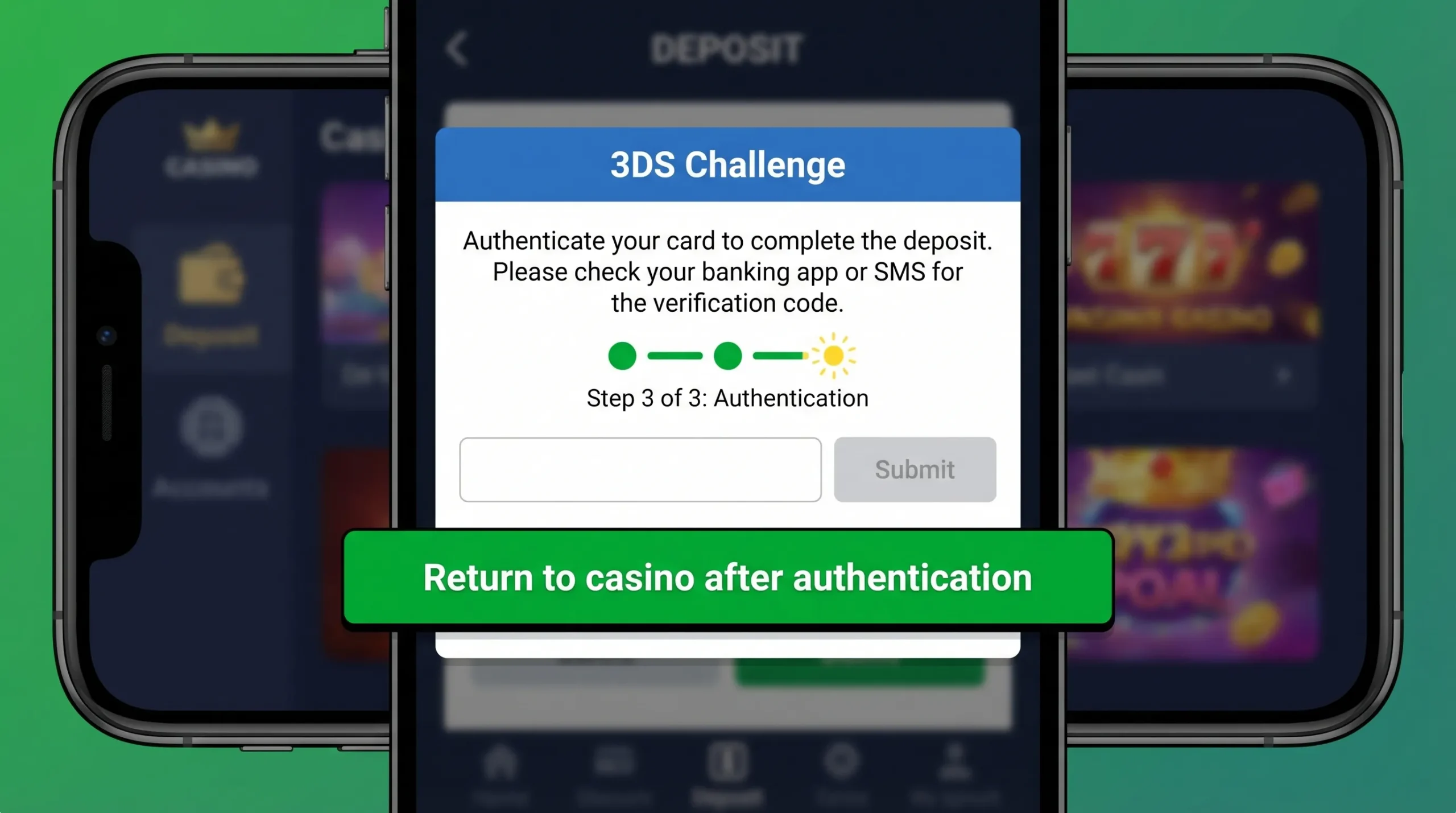

A challenged 3DS flow is one of the most fragile moments in the entire funnel:

- context switching to a banking app breaks attention

- OTP delivery can be delayed

- embedded webviews can misbehave

- players abandon instead of retrying

If your acquisition mix is mobile-heavy and your product promise is “deposit and play in seconds,” blanket 3DS can quietly erase your marketing gains.

2) Your issuer mix is challenge-prone

Some markets and issuer segments trigger challenges more often. If your 3DS configuration or PSP setup pushes too many transactions into challenge, your abandonment can spike.

This is why you should track challenge rate by BIN/issuer/country/device and not just overall.

3) You apply 3DS to returning, low-risk players

If a player has a stable pattern (same device, same instrument, consistent behavior, clean history), forcing them through repeat challenges can reduce:

- repeat deposit frequency

- trust (it feels like something is wrong)

- session momentum (especially for live casino)

A common anti-pattern is “3DS on all cards forever.” Returning-player deposits are exactly where you want low-friction flows.

4) Your UX and messaging are not designed for authentication

3DS fails are often not “fraud” and not “issuer hates you.” They are UX failures:

- unclear instructions (what is happening, why it matters)

- no recovery path (retry, switch method, contact support)

- no deposit status visibility

If you do not treat 3DS as a product surface, it will behave like a random outage in the player’s mind.

5) You already have better rails for your audience

In many regions, the best conversion is not achieved by “fixing cards,” but by offering the right alternatives:

- pay-by-bank or instant bank rails

- local APMs

- crypto deposits for crypto-native cohorts

If your audience strongly prefers non-card methods, pushing cards through 3DS can be the wrong fight.

A decision matrix: should this deposit attempt use 3DS?

You will get the best results when 3DS is a risk-based step-up, not a default.

| Situation | 3DS recommendation | Why |

|---|---|---|

| EEA/UK regulated brand, cards are a primary rail | Use 3DS broadly, optimize for frictionless | Improves SCA compliance posture and issuer confidence |

| New player, cross-border card, high velocity, or mismatched signals | Step-up to 3DS (challenge possible) | Converts “risky” attempts into authenticated approvals, reduces dispute exposure |

| Returning player with strong history and stable device/instrument | Prefer non-3DS or frictionless-first | Preserves repeat deposit conversion |

| Mobile-heavy acquisition where time-to-credit is critical | Minimize challenges, use smart routing | Challenges increase abandonment |

| Market with strong local APM adoption | Use 3DS selectively, expand APMs | Cheaper and higher-converting alternatives may exist |

How to deploy 3DS without killing conversion

Treat 3DS as “step-up,” not “always-on”

Operationally, this means you decide at runtime whether to request authentication based on risk and business context.

A practical step-up policy often includes signals like:

- new account or first deposit

- device mismatch (new device, suspicious environment)

- velocity thresholds (attempt frequency, retries)

- BIN country vs IP country mismatch

- high-risk geos or affiliate sources

- recent chargeback history on the player identity graph

Instrument the funnel with 3DS-specific events

If you cannot measure where players drop, you cannot tune.

At minimum, log these events with consistent IDs across your cashier, PSP responses, and ledger:

- deposit_initiated

- 3ds_started

- 3ds_frictionless

- 3ds_challenged

- 3ds_challenge_completed

- 3ds_failed (with reason bucket)

- auth_approved / auth_declined

- deposit_credited

- deposit_abandoned

Then analyze by segment (issuer, device, geo, affiliate, KYC state). This is where real-time analytics helps because 3DS issues can appear suddenly when issuer behavior changes.

Design a recovery path (this is where most casinos lose money)

When a 3DS challenge fails or is abandoned, you want a controlled “Plan B” that feels intentional.

Common recovery options include:

- retry with clearer instructions

- offer a different rail (APM or pay-by-bank)

- suggest a smaller amount (when appropriate)

- prompt KYC step-up if it increases acceptance for certain rails

If you want the recovery flow to actually convert, it should be built with conversion rate optimization discipline. Partnering with specialists for funnel diagnostics and UX testing can help, for example via a boutique team like WRM Design for SEO and conversion strategy.

Use routing and orchestration to control who gets challenged

Not all PSPs and acquiring setups perform the same for iGaming traffic. Even within one PSP, configuration choices can change challenge behavior.

Payment orchestration lets you:

- route by BIN, country, currency, and risk score

- avoid cascading retries that look like fraud to issuers

- fail over when an ACS or provider has an incident

The goal is simple: keep low-risk deposits fast, and make high-risk deposits defensible.

Make sure your 3DS UX is mobile-first

A few non-negotiables if you care about conversion:

- show a clear “what happens next” message before redirecting

- keep the player inside your branded context where possible

- use explicit loading and status states (no blank screens)

- ensure the “return to merchant” step works reliably

The KPI set to judge 3DS honestly

If you only look at fraud reduction, you will overuse 3DS. If you only look at conversion, you will underuse it. You need both.

A balanced scorecard:

| KPI | What it tells you | Segment it by |

|---|---|---|

| Deposit approval rate | Revenue throughput | BIN, issuer, geo, PSP |

| 3DS challenge rate | Expected friction | BIN, device, country |

| Challenge completion rate | Whether your UX works | device, OS, browser/webview |

| Time-to-credit (P50/P95) | Session momentum impact | deposit method, geo |

| Abandonment after 3DS_started | True funnel cost | acquisition source, first vs repeat |

| Chargeback rate and reason codes | Dispute pressure | cohort month, instrument |

| Fraud-adjusted approval rate | Net performance | risk tier, player type |

Run the numbers as a cohort analysis, not as a weekly blended average. 3DS often looks “fine” in aggregate while silently crushing one high-value segment.

What about crypto deposits?

3DS is a card protocol, so it does not apply to native crypto transfers. For crypto-forward brands, this creates a strategic option: let cards be a regulated, authenticated rail, and let crypto be the fast, low-chargeback rail for users who prefer it.

If you support both crypto and fiat, you can route players to the most suitable deposit experience based on their preferences and risk profile.

Where Spinlab fits (without rebuilding your stack)

If your takeaway is “we need to tune 3DS like a product,” the hard part is that most teams cannot do it cleanly with a fragmented stack.

Spinlab Studio is built as a modular iGaming platform that combines the pieces you need to operationalize risk-based deposits in one place, including:

- fiat and crypto payment support (including crypto onramp flows)

- fraud prevention and compliance foundations (KYC/AML)

- a configurable backoffice and open APIs for routing and rules

- real-time analytics to monitor approval, friction, and funnel drop-off

If you are launching a new brand, Spinlab is also positioned as a cost-efficient white label option with a Shopify-like operator experience, which matters when you want fast iteration on cashier UX.

Frequently Asked Questions

Does 3DS increase casino deposit approval rates? It can, especially in markets and issuer segments that prefer authenticated e-commerce transactions. But if it triggers frequent challenges, approval gains can be offset by higher abandonment.

Should casinos force 3DS on every card deposit? Usually no. The best-performing setups use risk-based step-up so low-risk, returning players get faster deposits while higher-risk attempts are authenticated.

Is 3DS required for SCA compliance in Europe? 3DS is the most common way to meet SCA for card-not-present payments, but exemptions and alternative authentication approaches can exist depending on your PSP, acquirer, and context.

What is the biggest downside of 3DS for casino deposits? Player friction during challenges, particularly on mobile. This is why challenge rate, completion rate, and time-to-credit are critical KPIs.

How do I know if 3DS is hurting conversion? Track abandonment starting from 3ds_started and break it down by device, issuer/BIN, and acquisition source. If one segment spikes, tune routing or offer alternative rails.

Make 3DS a precision tool, not a tax on every deposit

If you want to scale cards without turning your cashier into an obstacle course, you need three things: a step-up policy, clean deposit instrumentation, and the ability to route deposits intelligently across rails.

Spinlab Studio helps operators launch and scale with an integrated, crypto-ready cashier and the analytics and control layer needed to measure friction and protect revenue.

Explore the platform at spinlab.studio or request a walkthrough to see how a modular payments and risk stack can support smarter 3DS decisions.