Open Banking Is Finally Hitting the Casino Cage

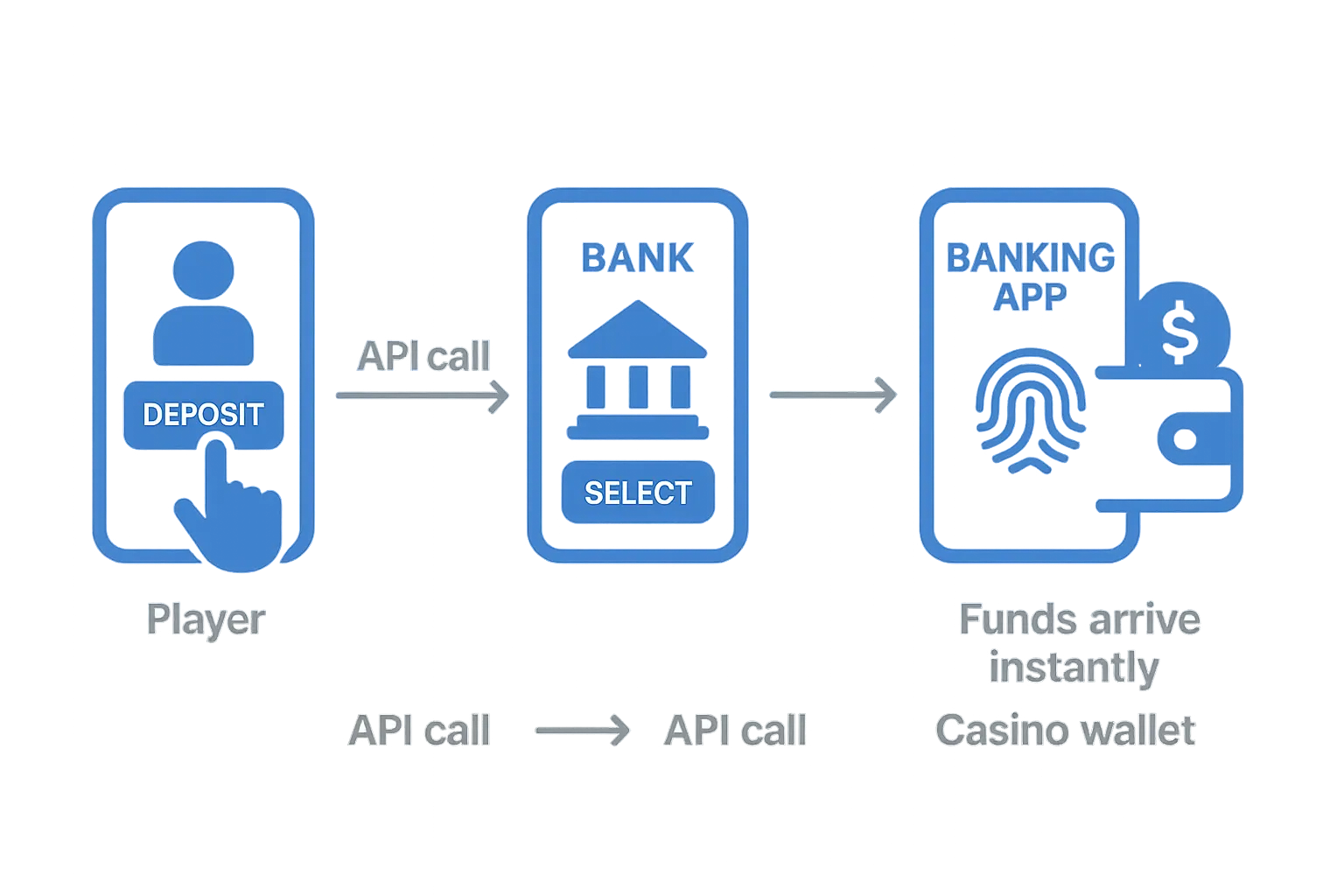

When PSD2 cracked Europe’s banking silos a few years ago, the iGaming world watched from the sidelines. Fast-forward to 2025 and open-banking APIs are now battle-tested, regulator-approved, and every bit as fast as card or crypto rails. For casino operators, that means you can invite players to deposit straight from their bank accounts—instantly, securely, and at a fraction of card fees.

Below are seven concrete ways open banking will reshape the deposit experience over the next 12-18 months, plus a quick look at how to plug this new rail into your cashier without rebuilding your tech stack.

1. True Instant Deposits—No Cards, No Waiting

Open-banking payments are account-to-account (A2A). In Europe they ride SEPA Instant; in the UK, Faster Payments; and in Brazil, Pix. The money leaves the customer’s account and lands in your merchant wallet in seconds, 24/7/365.

What it means for casinos:

- First-time players can jump from registration to wagering in <10 seconds.

- Weekend and holiday peaks stay cash-positive—no “pending” card batches.

- You can safely raise daily deposit limits because settlement risk disappears.

A 2024 Tink study found that 73 % of gamers who tried A2A deposits rated them “faster” than cards, and 61 % said they would switch permanently if the option were consistently available.

2. Processing Fees Drop by Up to 80 %

Visa and Mastercard interchange keeps creeping up. Open banking bypasses the card scheme toll booths entirely. PSPs typically charge a flat €0.10–€0.20 per deposit—no ad-valorem percentage—plus a modest platform fee.

For a casino handling €20 million a month with an average 2 % card fee, migrating just 40 % of volume to open banking saves roughly €160,000 annually.

Pro tip: Reinforce the switch with player-facing incentives—e.g., no deposit fees, faster withdrawals, or an instant cashback bonus—financed by the savings.

3. Built-In KYC, Affordability & AML Signals

Because the player authorizes a direct connection to their bank, you receive verified account identity (name, IBAN, sometimes address) as part of the payment payload. Many data providers enrich that with:

- Salary and recurring income streams

- Average balance over time

- Risk flags (overdraft frequency, gambling spend)

That lets compliance teams perform source-of-funds and affordability checks before funds hit the cage—crucial under UKGC and forthcoming EU AML6 rules.

If you liked our deep dive on live compliance metrics in “Real-Time Analytics in iGaming” you’ll love how open-banking data plugs directly into the same dashboards.

4. Chargebacks All but Disappear

Card deposits carry a built-in 120-day dispute window. A2A transactions are irrevocable once authorized, which slashes:

- Friendly fraud—“I never made that bet.”

- Costly scheme dispute fees (€25–€35 each).

- Rolling reserves demanded by acquirers.

According to TrueLayer, iGaming merchants using A2A saw chargeback ratios fall below 0.05 %—ten times lower than card benchmarks. The knock-on benefit: higher scheme approval rates for the card volume you still keep.

5. Symmetric Pay-Ins & Pay-Outs Keep Players Loyal

Nothing frustrates a high-roller like waiting three days for withdrawals when deposits were instant. Open banking supports push and pull, so verified customers can receive winnings back to the same bank in seconds. Operators report up to 12 % higher second-time deposits when payout speed matches deposit speed.

Spinlab’s cashier exposes both directions through a single REST endpoint, so you don’t juggle separate PSPs for deposits and withdrawals.

6. Responsible Gambling Tools Go Real-Time

Because you can poll a player’s balance and incoming salary (when they consent), you can:

- Trigger hard stops if gambling spend exceeds, say, 30 % of disposable income.

- Offer personalized cooling-off periods based on genuine liquidity rather than arbitrary limits.

Expect these data-driven controls to become standard in 2026 as regulators push for proactive intervention. Early adopters will score trust points with watchdogs and customers alike.

7. Hyper-Targeted Bonuses Powered by Banking Data

Imagine spotting that a player’s paycheck landed this morning and automatically offering a €20 matched bonus if they top up before midnight. Or noticing a regular Monday-night roulette fan got paid early and nudging them with free spins on new Pragmatic Play titles.

Open-banking insights combined with Spinlab’s bonus engine make such micro-moments possible. The result: higher CTRs and more efficient bonus spend compared with blanket email blasts.

How to Integrate Open Banking Without Ripping Out Your Cashier

- Choose a global aggregator: Providers like Tink, TrueLayer, and Yapily already cover >3,400 banks across the EU, UK, and parts of LATAM.

- Map flows to your compliance stack: Decide which KYC fields are mandatory to accept a deposit. Spinlab’s KYC module can auto-reconcile these fields to your existing player profile.

- Update the cashier UI: Position “Bank Transfer (Instant)” above cards and e-wallets. Conversion studies show that placement alone drives adoption.

- Educate VIP managers: Give them talking points on lower fees and faster payouts—they’ll push high-value players to switch.

- Analyze and iterate: Use the real-time dashboards we ship to track open-banking share, acceptance, and downstream LTV.

For operators already on Spinlab, the integration is largely plug-and-play: activate the Open Banking module in BackOffice, obtain your PSP API keys, and you’re live in under a week.

Frequently Asked Questions

Is open banking safe for my players?

Yes. Strong Customer Authentication (SCA) is enforced by the player’s own banking app—usually biometrics or a PIN—making it at least as secure as 3-D Secure card flows.

What if a player’s bank isn’t supported?

The cashier automatically falls back to traditional card or wallet options. Coverage in Europe now exceeds 95 % of active bank accounts.

Can I still accept crypto deposits alongside open banking?

Absolutely. Many operators run a hybrid cashier. See our breakdown in “Crypto vs Fiat: Which Payment Gateway Drives Higher Player Lifetime Value?” for optimization tips.

Are there limits on maximum transaction size?

Rails like SEPA Instant cap transfers at €100,000 per payment—well above typical consumer deposits. For VIPs needing larger moves, wire transfers or stablecoin rails remain available.

Do I need extra licenses to use open banking?

In most EU jurisdictions, your PSP holds the AIS/PIS licenses. You operate under your existing gaming license, but always check local guidance.

Ready to Cut Fees and Double Deposit Speed?

Open banking is no longer experimental—it’s fast becoming the default cashier option for regulated markets. If you’d like to see a live demo of instant A2A deposits inside Spinlab’s white-label casino platform, book a 30-minute call with our payments team today.

Book a Demo →