Withdrawal holds sit at the intersection of trust and risk. Pay too slowly and you train good players to churn, pay too fast and you invite fraud, bonus abuse, AML exposure, and payment-rail reversals.

A modern online casino should treat withdrawal holds as a product and risk decisioning system, not an ops habit. The goal is simple:

- Auto-pay the majority of withdrawals (fast, predictable, low support load).

- Route only high-signal cases to review (better loss control, cleaner audits, fewer false positives).

Below is an operator-focused framework for deciding when to review and when to auto-pay, plus the instrumentation you need to prove it is working.

What a “withdrawal hold” actually is (and why players hate it)

A withdrawal hold is any deliberate delay between a player requesting a cashout and funds leaving your control. Holds exist for legitimate reasons:

- KYC completion and identity re-checks (especially when risk signals change)

- AML and sanctions controls, including source-of-funds prompts and transaction monitoring

- Fraud prevention, such as account takeover (ATO) and stolen payment instruments

- Bonus and promo enforcement, to prevent “deposit, bonus, cashout” loops

- Payment-rail constraints, including settlement timing and chargeback windows (rail-dependent)

Players rarely object to compliance itself. They object to uncertainty.

If the only state they see is “Pending,” your hold becomes a story they tell themselves: “This casino will never pay.” Your job is to replace that with a clear, auditable process that both players and regulators recognize.

The core principle: minimize holds without removing controls

A practical policy for 2026 is not “no holds” or “hold everything.” It is:

- Default to auto-pay for low-risk, well-known players

- Use step-up checks (automated or semi-automated) when signals warrant it

- Reserve manual review for cases where a human can meaningfully reduce risk

This mirrors how high-performing fintechs run withdrawals: most transactions are straight-through processed (STP), while exceptions enter a queue with strict SLAs.

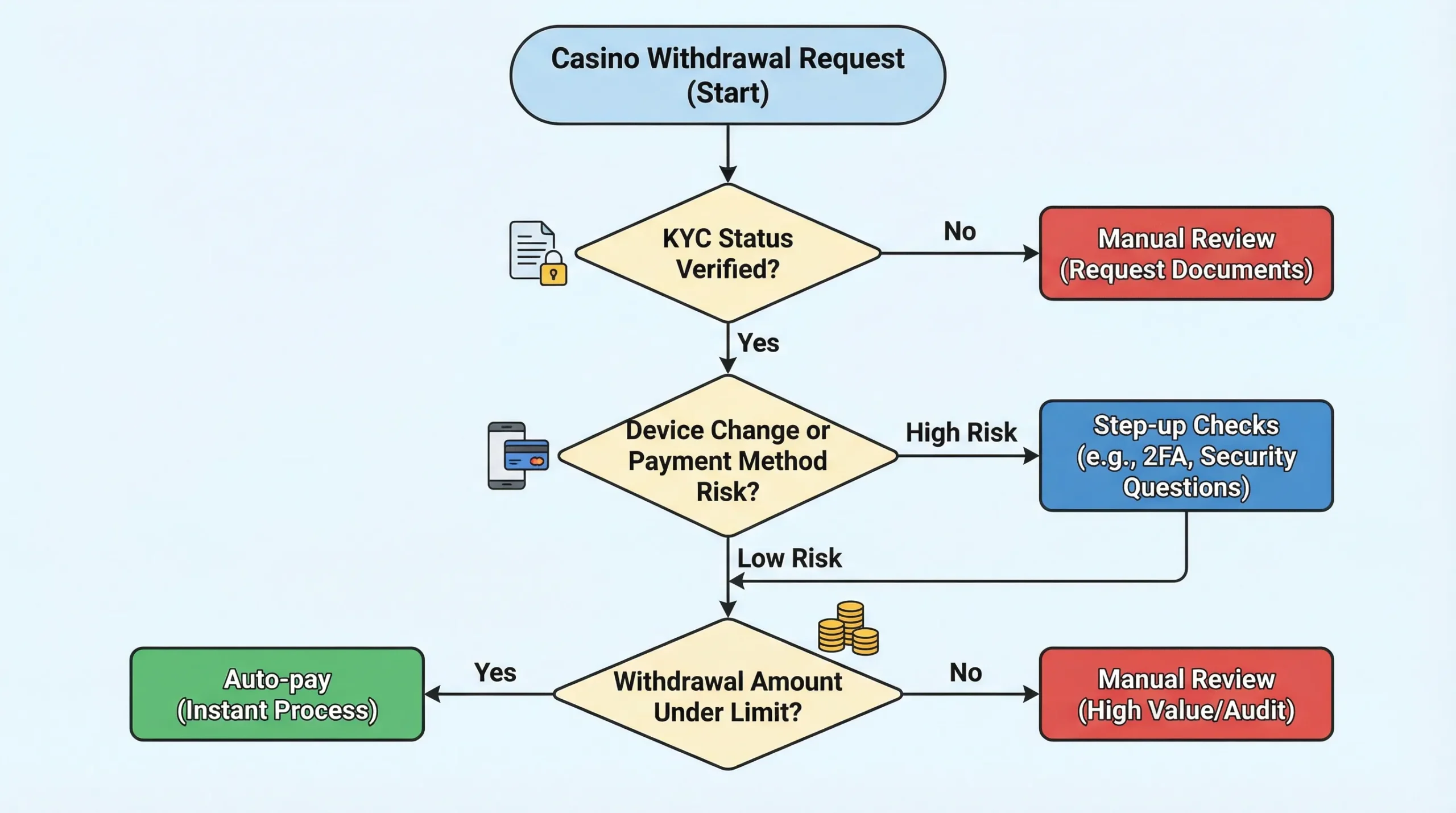

Build a tiered decision model (not a single rule)

If you only have one rule, like “first withdrawal requires manual review,” you will either:

- create a permanent bottleneck, or

- loosen it until it stops protecting you

Instead, define a tiered decision model that considers player profile, withdrawal context, and rail behavior.

A simple, implementable decision matrix

Use a matrix like this to align risk, compliance, and ops.

| Scenario | Risk signal summary | Recommended action | Why this works |

|---|---|---|---|

| Returning player, stable device, KYC complete, same payout method as deposits | Low | Auto-pay | STP reduces churn and tickets, risk is already priced-in |

| Returning player, KYC complete, but new device or new IP/geo pattern | Medium | Auto-pay with step-up | You keep speed while verifying it is not ATO |

| First-time withdrawal, KYC not complete | High | Hold for KYC | Regulators and PSPs expect identity controls before outflows |

| Large withdrawal relative to player’s typical activity | Medium to high | Step-up, then review if needed | Catches mule patterns and bonus abuse while limiting false holds |

| Crypto withdrawal to a new address, or high-risk chain exposure | High | Automated KYT + review | On-chain risk is measurable, humans handle ambiguity |

| Promo-eligible withdrawal where bonus terms may be breached | Medium | Automated rules check | Most cases can be resolved without a human |

The key is that “review” is not a default, it is a destination reached only after signals justify it.

When to auto-pay: eligibility rules that are defensible

Auto-pay does not mean “no controls.” It means controls happen before or within milliseconds of payment execution.

Most casinos can safely auto-pay when the following are true:

Identity and account integrity

- KYC is complete (or your jurisdiction allows tiered KYC and the player is within allowed limits)

- No recent credential changes (password reset, email change, phone change) within your defined “cooldown” window

- No strong ATO signals (impossible travel, device fingerprint mismatch, abnormal login pattern)

Payment method consistency

- The withdrawal method is linked to the player and consistent with historical behavior

- No third-party payment indicators (mismatched names, unusual funding sources, repeated method churn)

Clean operational history

- No open disputes, negative balances, or unresolved chargeback exposure

- No recent failed withdrawals caused by incorrect details (which can hide mule behavior)

Bonus and wagering rules are already satisfied

- Wagering completion is computed deterministically from your ledger and game events

- Promo restrictions are evaluated automatically (eligible games, max bet, excluded providers)

Risk score is below threshold

This is where many operators get stuck. The fix is to define a risk score that is:

- explainable (you can justify it in an audit)

- measurable (you can backtest it)

- tunable (you can adjust it without rewriting your entire cashier)

A common architecture is hybrid: deterministic rules plus a scoring layer that weights signals.

When to review: “high-signal” triggers that deserve human time

Manual review is expensive, slow, and inconsistent, but sometimes necessary. The mistake is sending low-signal cases to humans, which creates queues and teaches fraudsters how to blend in.

Route to review only when the case is both meaningfully risky and meaningfully resolvable by a human.

1) KYC and AML escalation cases

- KYC failed, repeated resubmissions, or document inconsistency

- Name/date-of-birth discrepancies that need interpretation

- AML monitoring triggers (unusual transaction patterns, structuring)

For AML context, align your monitoring approach with risk-based principles described by the Financial Action Task Force (FATF), then implement it in a way that is auditable inside your backoffice.

2) First withdrawal plus friction signals

A first withdrawal is not automatically risky, but it is a common point for:

- bonus abuse

- mule activity

- support disputes

Review becomes justified when first withdrawal is paired with signals like:

- short time between deposit and withdrawal

- method churn (multiple deposit methods, new withdrawal destination)

- abnormal session behavior (minimal gameplay, immediate cashout)

3) Payment-rail specific red flags

Different rails have different failure modes.

- Cards: higher dispute risk and instrument testing patterns

- Bank rails: identity mismatch and beneficiary manipulation

- Crypto: address risk, chain hopping, and sanctions exposure

Your policy should be rail-aware. A “one size fits all” hold policy is usually a sign your stack cannot make nuanced decisions.

4) Large or anomalous withdrawals

Instead of hardcoding a universal number, define “large” as a function of:

- player lifetime deposits and net position

- expected player value tier

- jurisdictional limits

- your treasury and liquidity constraints

A useful trigger is deviation: “How far is this request from the player’s normal withdrawal pattern?” Humans add value here because they can assess context, communications, and case history.

5) Responsible gambling and harm signals

Some jurisdictions and internal policies require intervention when behavior indicates harm, especially if a withdrawal is tied to volatility spikes or distressed play.

The point is not to block withdrawals as punishment. It is to ensure your RG controls are applied consistently and logged.

Step-up checks: the middle path that preserves speed

Most operators underuse step-up checks. They jump from auto-pay to manual review, which is where ticket volume and trust problems appear.

Step-up checks are automated gates that run when risk increases, without forcing a full case review.

Common step-up checks include:

- re-authentication (2FA or passkey prompt)

- liveness check for high-risk identity events

- confirming a payout destination (bank account verification or crypto address confirmation)

- lightweight source-of-funds prompt at defined thresholds

The design goal is to keep 80 to 95 percent of withdrawals out of a human queue, while still tightening controls when signals change.

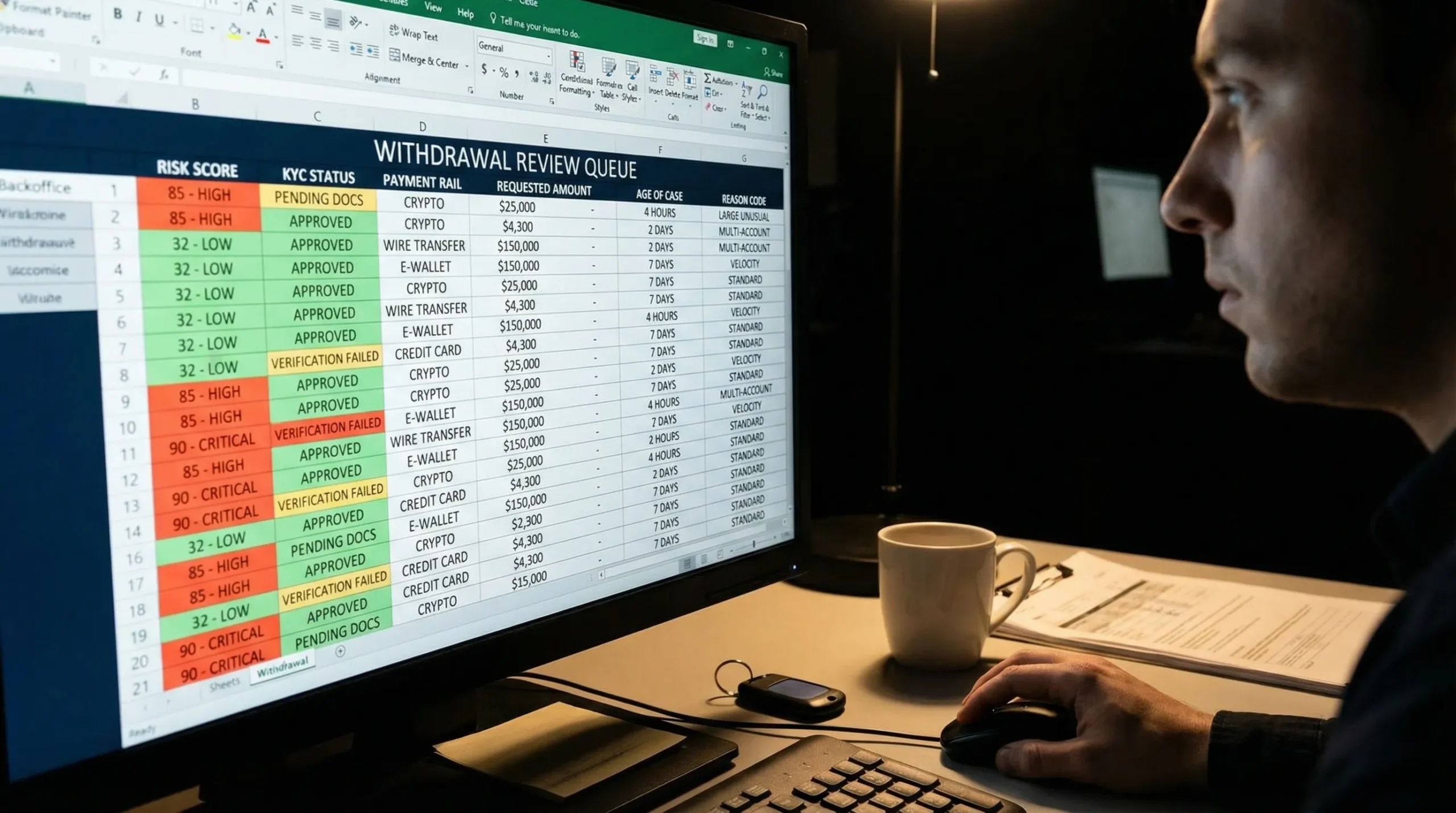

Make holds operationally safe: queues, SLAs, and reason codes

If you do manual review, treat it like production engineering, not a shared inbox.

Queue design that prevents backlogs

A good withdrawal review queue needs:

- prioritization (by risk, aging, VIP tier, and regulatory deadlines)

- deduplication (merge related events into one case)

- case timelines (player, device, payments, gameplay, bonus events)

- action logging (who did what, when, and why)

Reason codes matter more than you think

Every hold should map to a reason code that is both:

- player-explainable (in plain English)

- audit-defensible (in compliance language)

This improves training, reduces inconsistency, and makes analytics possible.

Player communication: copy that reduces tickets without giving away your controls

You do not need to reveal your entire fraud model. You do need to provide:

- a clear status

- expected timing ranges (even if broad)

- the next action required (if any)

One useful benchmark is to look outside gambling: high-trust consumer brands reduce inbound support by publishing clear policies and expectations. Even a non-gaming business can set the bar for transparency, for example how transparent customer policies are presented on sites like Lumina Skin Sanctuary.

In casino UX, the equivalent is a withdrawal tracker that answers “What is happening right now?” without forcing the player to open a ticket.

Metrics that tell you if your hold policy is healthy

If you cannot measure it, you cannot tune it. Track these weekly, and segment by country, rail, VIP tier, and cohort (new vs returning).

| Metric | What it indicates | Why it matters |

|---|---|---|

| P50 time-to-paid and P95 time-to-paid | Typical vs worst-case experience | P95 is where social complaints and churn are born |

| Manual review rate | Operational load and friction | High rates usually mean weak automation or overblocking |

| False positive rate (reviewed then paid) | Quality of your routing | Reduces queue volume when improved |

| Withdrawal failure rate | Rail health and data quality | Prevents repeated tickets and rework |

| Chargeback/dispute rate after withdrawals | Downstream risk leakage | Signals whether you are paying out compromised accounts |

| Bonus abuse loss per 1,000 withdrawals | Promo control effectiveness | Tells you if holds are masking weak bonus enforcement |

| Tickets per 1,000 withdrawals | Player confusion and ops friction | Strongly correlated with vague statuses |

A high-performing program does not just “speed up withdrawals,” it shifts volume from manual review to safe auto-pay while keeping losses flat or declining.

Implementation blueprint: how to move from manual holds to controlled auto-pay

You can roll this out without a year-long rebuild if your platform exposes the right events and decision points.

Phase 1: Instrumentation and baselining (1 to 2 weeks)

- Define your event taxonomy for withdrawals (requested, screened, held, released, paid, failed)

- Baseline P50 and P95 times by rail

- Tag each hold with a reason code

Phase 2: Build your routing rules (2 to 4 weeks)

- Define auto-pay eligibility (KYC state, rail constraints, account integrity signals)

- Add step-up checks for medium risk scenarios

- Create a manual queue for only the truly high-signal cases

Phase 3: Tune with feedback loops (ongoing)

- Backtest: which review cases were actually bad?

- Tighten or relax rules based on loss outcomes, not vibes

- Add new signals as fraud patterns evolve

This is where an integrated iGaming platform helps. Spinlab, for example, is built around modular components that matter for withdrawal decisioning, including payments (fiat and crypto), KYC and AML workflows, fraud prevention, and real-time analytics, so operators can centralize signals rather than stitching together five vendor dashboards.

The operator takeaway

Withdrawal holds are not a necessary evil, they are a system you can design.

- Auto-pay when identity is stable, payment behavior is consistent, and risk is low.

- Step-up when signals change, so you keep speed without going blind.

- Review only when a human can materially reduce exposure.

Done well, this turns withdrawals from a churn moment into a trust flywheel, while making compliance and fraud teams more effective, not more overloaded.