UPI is the closest thing India has to a default checkout button. For casino operators targeting Indian players (or Indian diaspora markets where it is legally permitted), supporting UPI can lift deposit conversion primarily by reducing “payment effort”: players do not need to type long card numbers, they already trust their UPI app, and authorization happens inside a familiar flow.

But UPI is not “just another payment method.” It is a domestic scheme with strict ecosystem rules, data expectations, and operational realities (asynchronous confirmations, handle-based identity, and dispute workflows) that can break both compliance and UX if you bolt it on like cards.

This guide focuses on two things product and ops teams actually need: compliance guardrails and cashier UX patterns that reduce abandonment without creating regulatory or fraud exposure.

What makes UPI different for online casinos

UPI (Unified Payments Interface) is a real-time bank-to-bank payment system operated by NPCI. It is commonly initiated through mobile apps, and users authenticate with a UPI PIN within their banking or third-party UPI app. NPCI maintains high-level technical and product documentation for UPI rails on its official site, which is a useful starting point for terminology and flow differences.

For casinos, the practical differences versus cards and even many APMs show up in three areas:

- Flow ownership: authorization happens inside a UPI app, not inside your cashier. Your UI must hand off cleanly and recover gracefully.

- State management: you will see more “pending” outcomes than with cards. Treat UPI as asynchronous by design.

- Identity and compliance signals: you are not getting a PAN, CVV, or 3DS signal. You are getting a payer handle (VPA) and bank rails behavior, which changes how you do fraud prevention and reconciliation.

Compliance reality check (before you build anything)

India’s gambling legality and payments acceptance are not one-size-fits-all. Online gambling rules can vary materially by state, and payment providers may have their own prohibitions even where a product is arguably legal. So start with a simple principle: do not treat UPI integration as a workaround, treat it as a regulated payment rail that must align with (1) your licensing posture, (2) your payment partner’s rules, and (3) your internal AML and responsible gambling framework.

Here are the core compliance areas that typically decide whether a UPI project succeeds or stalls:

1) Market legality and geo-controls

If you cannot confidently describe where, to whom, and under what license you are offering gambling products, UPI will amplify the risk because it is tightly connected to domestic banking.

Operationally, this usually means you need:

- Geo enforcement (at registration and at cashier) with documented controls.

- Jurisdiction-specific payment availability, so UPI only appears where you have a defensible legal basis.

- Clear terms and audit logs for eligibility decisions.

2) KYC and AML alignment

UPI does not replace KYC. A casino still needs a risk-based KYC program, and in higher-risk scenarios you may need Enhanced Due Diligence. If you are building processes that reference Indian KYC expectations, the Reserve Bank of India publishes KYC Master Directions and related circulars that help frame what regulated entities typically do (even if your licensing is offshore, aligning to strong KYC standards is often expected by banks and PSPs).

Your cashier decisions should reflect that:

- Use KYC gates before enabling higher limits or withdrawals.

- Link UPI deposits to a player identity record (not just an order ID).

- Store minimum necessary payment identifiers and retain them according to your compliance retention policy.

3) Provider and scheme restrictions

Many PSPs and banking partners restrict or prohibit processing for gambling categories, regardless of UX. Do not invest in a full front-end build before you have written confirmation of:

- Supported merchant category and transaction types

- Refund and dispute handling expectations

- Data fields you must display to the payer (merchant name, reference, purpose)

- SLA for success callbacks and settlement reporting

If you are still sourcing partners, treat vendor outreach like a pipeline. Teams often underestimate how much time is lost on back-and-forth just to confirm capabilities, limits, and approval requirements. Using an automated prospecting tool such as Orsay can help operators and B2B teams qualify PSP, aggregator, and compliance vendors faster, especially when you need multiple options due to category restrictions.

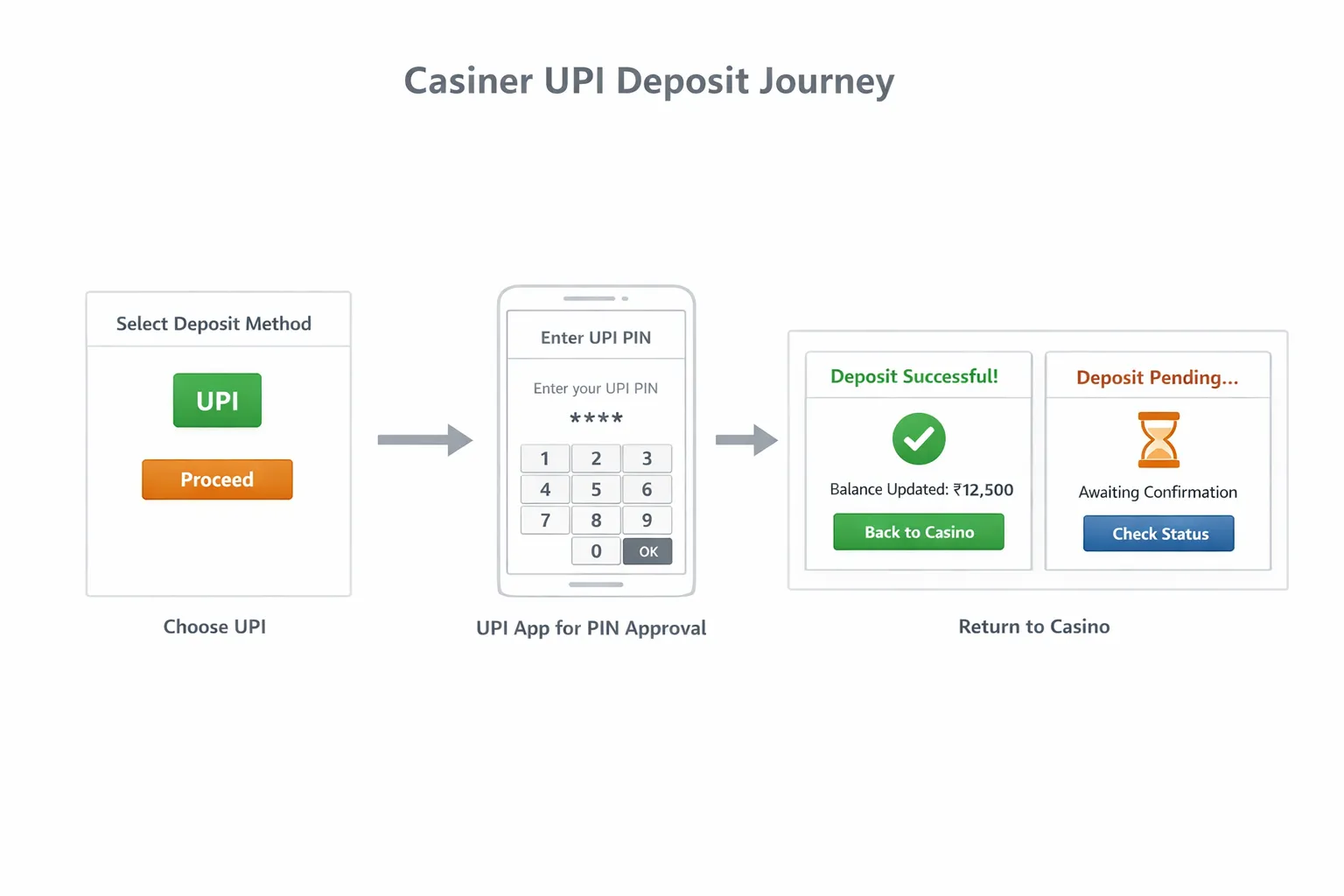

Pick the right UPI flow: intent, collect, or QR

A common mistake is choosing a UPI flow based on what is easiest for engineering, instead of what best matches player behavior on mobile.

Here is a practical comparison of the three patterns most product teams evaluate:

| UPI flow option | Best for | UX upside | UX risk | Operational/compliance notes |

|---|---|---|---|---|

| Intent (app deep link) | Mobile-first audiences with UPI apps installed | Fast, low typing, familiar authorization | Breaks if deep link fails, user returns without status | Needs robust “return to merchant” handling and a strong pending state strategy |

| Collect request (VPA entered) | Players who know their UPI ID and prefer approving inside their app | No app switching required until approval | Higher input friction, VPA typos cause abandonment | Strong validation and clear timeout messaging are critical |

| QR code | Desktop traffic or users who prefer scanning from another device | Simple mental model | Slower on mobile, can feel clunky in-app | Good fallback path when deep links fail |

Most casinos end up with a primary flow plus a fallback. For example, intent as default on mobile, and QR as fallback when the app handoff fails.

UX tips: how to make UPI deposits feel “instant” even when they are not

UPI can be extremely fast, but your users will not experience it as fast unless your UI is designed for handoffs, ambiguity, and waiting states.

1) Show UPI as a first-class option (but only when eligible)

Players in India often look for UPI immediately. If it is hidden behind “Other,” conversion drops. At the same time, showing UPI to ineligible users creates trust damage and support load.

A strong pattern is:

- Detect likely eligibility (geo, currency, device) and surface UPI prominently

- If not eligible, do not tease it. Hide it entirely rather than showing an error later

2) Use “handoff-first” microcopy

The biggest point of confusion is that the player must complete authorization inside another app.

Good microcopy clarifies three things in one breath:

- Where the authorization happens (their UPI app)

- What they need to do (approve with UPI PIN)

- What happens after (return to the casino)

Example approach (adapt to your tone and legal requirements): “You’ll be redirected to your UPI app to approve this deposit. After approval, you’ll return here automatically.”

3) Design for the “pending” outcome as a normal state

Treating pending as an exception leads to broken balances and angry users. Make it a product feature.

A good pending screen has:

- A clear status label (Processing, Awaiting confirmation)

- A timer or expectation window (without promising exact seconds)

- A single safe action (for example, “Check status”)

- A support escape hatch that attaches the transaction reference automatically

4) Prevent accidental double deposits

UPI’s speed can encourage rapid retries when the UI is unclear. That creates chargeback-like disputes and support tickets.

Use:

- One-tap “Check status” instead of “Pay again”

- Temporary locking of the pay button for the same amount and session

- Idempotency keys server-side so “repeat submit” cannot create multiple orders

5) Make failure states specific and recoverable

Avoid generic “Payment failed.” UPI failures vary: app not installed, deep link not supported, collect request expired, bank outage, payer declined.

Map errors into player-actionable categories:

- “Approval declined” (try again or choose another method)

- “No UPI app detected” (switch to QR or card)

- “Timed out” (check status, then retry)

- “Bank unavailable” (try later, suggest alternate method)

6) Keep the cashier lightweight on mobile

UPI is often chosen because it is frictionless. If your cashier page is heavy, the “redirect and return” loop becomes fragile.

Prioritize:

- Fast load time on 3G/4G

- Minimal third-party scripts on the deposit step

- A resilient return URL handler (even after app switching)

Compliance meets UX: the controls that also improve conversion

The best UPI implementations do not treat compliance as a separate layer. They build compliance checks into a smoother, safer flow.

Risk-based KYC gating (without killing first deposit)

UPI can bring high-intent users. Do not automatically force maximum KYC on every first deposit if your risk model does not justify it, but do implement a clear step-up policy.

A practical approach is:

- Allow a small first deposit with minimal friction (where legal and risk-acceptable)

- Trigger step-up KYC before withdrawals, higher limits, or unusual patterns

- Communicate the “why” in plain language to avoid support escalations

Responsible gambling controls that feel native

UPI makes depositing easy, which increases the importance of responsible gambling UX.

Consider:

- Deposit limit prompts that appear right after first successful deposit

- Cooling-off prompts when repeated deposits happen in a short window

- A clear ledger of deposit history and limit usage

These controls reduce regulatory risk and can reduce buyer’s remorse disputes.

Backend and ops tips: don’t let UPI break your ledger

Most “UPI problems” are actually ledger and reconciliation problems that surface as UX issues.

1) Ledger postings must be event-driven and idempotent

Design around events like:

- Deposit initiated

- Deposit authorized (success)

- Deposit pending

- Deposit failed

- Deposit reversed/refunded

If you credit balances on “initiated” instead of “confirmed,” you will create negative balances later. If you process the same callback twice, you will duplicate credits.

2) Reconciliation needs a daily discipline

UPI-style rails can create mismatches between your internal ledger, PSP reports, and bank settlement timing.

At minimum, define:

- Which reference IDs are authoritative (your order ID, PSP ID, UPI reference)

- A daily reconciliation job with exception queues

- A clear ownership model between payments ops and finance

3) Fraud prevention must adapt to bank-to-bank behavior

UPI reduces some card-specific fraud (like card testing), but you still face:

- Mule activity and bonus abuse

- Account takeover (ATO) followed by fast deposits and withdrawals

- Social engineering disputes (“I didn’t authorize”) even when the bank says authorized

This is where device intelligence, velocity rules, and behavior monitoring matter.

The table below summarizes controls that are both practical and audit-friendly.

| Area | What to implement | Why it matters |

|---|---|---|

| Transaction state machine | Explicit pending/success/fail/refund states | Prevents phantom credits and support chaos |

| Idempotency | Idempotency keys per deposit attempt | Stops duplicate orders and double credits |

| Velocity limits | Per account, per device, per payment identifier | Reduces abuse without blocking normal users |

| KYC step-up rules | Risk-based triggers before withdrawals/high limits | Aligns AML needs with deposit UX |

| Evidence logging | Timestamped events, terms acceptance, references | Helps resolve disputes and regulator queries |

Implementation approach with a modular iGaming platform

If you are integrating UPI into an existing casino stack, the fastest path is usually treating UPI as an APM module inside a broader payment hub, not as a one-off checkout page.

For example, Spinlab’s modular iGaming platform is designed for multi-rail payments and fast onboarding, with building blocks that matter when you add a new local method:

- Open API integration for connecting PSPs and local rails

- KYC and AML compliance tooling to support risk-based gating

- Advanced fraud prevention and real-time monitoring

- Multi-currency support and a mobile-optimized casino experience

If your goal is to ship quickly while still keeping flexibility, a modular white label approach also reduces the risk of hard-coding UPI assumptions into your core wallet logic.

Frequently Asked Questions

Is UPI legal to use for online casinos in India? India’s online gambling legality is complex and can vary by state, product type, and licensing posture. Treat this as a legal question and get jurisdiction-specific counsel, then implement geo-controls and payment availability rules accordingly.

Which UPI flow converts best for casino deposits? Many mobile-first products see the best UX with an intent (deep link) flow, provided you have excellent return handling and a strong pending state design. A QR fallback is often valuable for reliability.

How do you handle UPI deposits that stay pending? Design pending as a normal state: keep a clear “check status” action, poll safely or rely on provider callbacks, and only credit balances on confirmed success. Operationally, reconcile pending items daily with an exception queue.

Does UPI reduce fraud compared to cards? It can reduce certain card-specific attack types, but it does not eliminate fraud. Expect bonus abuse, mule behavior, ATO-driven deposits, and disputes, then implement velocity limits, device signals, and risk-based KYC step-up.

Do you need KYC if you offer UPI? Yes. UPI is a payment method, not a substitute for a KYC/AML program. Use risk-based KYC to balance compliance with first-deposit conversion.

Build a UPI-ready cashier without slowing down your launch

If you want UPI to increase deposits instead of increasing support tickets, you need two things at the same time: a compliant operating model (KYC/AML, logging, geo-controls) and a cashier built for handoffs and pending states.

Spinlab helps operators build, launch, and scale online casinos on a modular platform with integrated payments, compliance tooling, fraud prevention, analytics, and a mobile-first UX. If you are planning to add UPI (alongside other local methods and crypto-ready options), explore the platform at spinlab.studio and align the integration to your licensing and risk requirements before you ship.