Why talk about payment gateways and Lifetime Value in 2025?

Payment methods have moved from being a pure cashier matter to becoming one of the most reliable predictors of player Lifetime Value (LTV). In a market where acquisition costs continue to climb—average first-time-deposit (FTD) costs reached $248 in Q1 2025 according to SoftSwiss—operators can no longer rely on welcome bonuses alone. They need players who deposit more often, for a longer period, and with lower operational friction.

Enter the debate: crypto vs. fiat gateways. Which route actually yields a higher LTV? And is the answer the same for every market or vertical? Let’s dive into data from recent white papers, operator panels, and our own benchmarks at Spinlab Studio to unpack this question.

Defining the metrics: Beyond “total deposits”

Operators often track LTV as total deposits minus withdrawals per player. That metric is incomplete. A modern LTV model includes:

- Net Gaming Revenue (NGR) generated by the player

- Bonus cost attributed

- Payment processing fees and chargebacks

- Fraud write-offs

- Support & VIP overhead

When comparing payment rails, we therefore have to look at:

- Average deposit size and frequency

- Time to first deposit

- Processing cost and volatility risk

- Fraud/chargeback ratio

- Churn probability and reactivation rates

How crypto gateways fare on each dimension

| Dimension | Crypto (BTC, ETH, USDT, etc.) | Comments |

|---|---|---|

| Avg. deposit size | 1.7–2.3× higher than fiat (SoftSwiss 2025) | High-rollers love the anonymity & speed |

| Deposit frequency | Slightly lower (−12 % vs. e-wallet users) | Bigger tickets mean fewer top-ups |

| Time to first deposit | 43 % faster when casino offers direct wallet connect | KYC friction can cancel this advantage if not automated |

| Processing fees | 0.5 %–1 % + network gas | Cheaper than cards but more volatile |

| Chargebacks | Practically zero | Irreversible nature of blockchain |

| Fraud | Account fraud 35 % lower, but bonus abuse 18 % higher | Multiple wallets / VPN stacking |

| Churn | 9 % lower over 12 months (SOFTSWISS) | Strong community factor |

TL;DR

Crypto tends to create fewer but bigger, longer-staying players with lower payment costs, provided that volatility and regulatory screens are handled.

How fiat gateways compete

| Dimension | Cards & e-wallets | Comments |

|---|---|---|

| Avg. deposit size | Baseline | $47 worldwide average in 2024 (Envoy report) |

| Deposit frequency | 2.1× crypto | Smaller but more frequent micro-bets (slots, casual tables) |

| Time to first deposit | Fast in EU (PSD2 Instant), slower in LATAM | 3-D Secure can add friction |

| Processing fees | 1.8 %–4 % + FX | Negotiated tiers for top operators |

| Chargebacks | 0.6 %–1.1 % of volume | Card schemes favor consumers |

| Fraud | Higher on stolen-card attempts, lower on bonus abuse | Tools like 3-D Secure 2.3 help |

| Churn | Neutral baseline | Loyalty driven by content, not payment method |

TL;DR

Fiat still dominates casual gaming, mass markets, and heavily regulated jurisdictions. Higher frequency can offset smaller ticket sizes, but the cost of disputes and higher payment fees eat into margin.

The macro forces changing the equation in 2025

- Stablecoin normalization: With PayPal’s PYUSD and Circle’s expansion in Europe, stablecoins reduce volatility risk, bringing crypto one step closer to mainstream cash.

- Emerging-market leapfrog: Nigeria, Argentina, and Turkey are seeing >40 % of iGaming deposits via USDT because local fiat is either restricted or hyperinflationary.

- RegTech automation: AI-driven KYC (Jumio 2025 edition) verifies a crypto user in <45 seconds, cutting the old “crypto = no KYC” myth while keeping regulators happy.

- MiCA & U.S. state bills: The EU’s Markets in Crypto-Assets regulation and state-level bills in New Jersey and Nevada define clearer compliance rails, making crypto adoption less risky for operators.

Calculating LTV by payment rail: A worked example

Imagine two cohorts of 10,000 FTDs acquired from the same media source in Q2 2025.

- CPA: $250 each (same campaign)

- Bonus: 100 % up to $200 (identical terms)

Cohort A – Crypto users (60 % BTC, 25 % USDT, 15 % ETH)

- Avg. first deposit: $145

- Avg. total deposits 12 mo: $790

- Net withdrawal: 42 % of deposits

- Processing fees: 0.8 %

- Chargeback loss: $0

- Fraud write-off: 0.15 %

- Retention 12 mo: 36 %

Cohort B – Fiat users (Visa/Mastercard/e-wallet)

- Avg. first deposit: $52

- Avg. total deposits 12 mo: $410

- Net withdrawal: 48 % of deposits

- Processing fees: 2.4 %

- Chargeback loss: 0.65 %

- Fraud write-off: 0.25 %

- Retention 12 mo: 28 %

LTV per cohort (simplified NGR model)

LTV = (Total Deposits – Withdrawals) × 0.35 (NGR margin) – Costs – Bonus

- Crypto: (($790×0.58)×0.35) – (0.008×$790) – $200 bonus ≈ $61.9

- Fiat: (($410×0.52)×0.35) – (0.024×$410) – $200 bonus ≈ $14.5

That is a 4.2× higher LTV for the crypto group. Retention and lower processing spend carry most of the difference.

Caveat: This model assumes equal regulatory cost. In some markets, crypto compliance overhead can add $5–$12 per active player.

Why many operators still start with fiat first

- Brand trust: New casinos often showcase Visa/Mastercard logos to establish legitimacy.

- Affiliate expectations: Review sites list card payout times as a key score factor.

- Licensing restrictions: Certain regulators (UKGC, MGA) still exercise additional scrutiny over crypto, slowing approvals.

Yet, operators that layer crypto early reap a compound benefit. SoftSwiss data shows that offering a crypto cashier on day 1 increases the share of crypto FTDs from 9 % to 27 % after six months without extra marketing spend—players self-select.

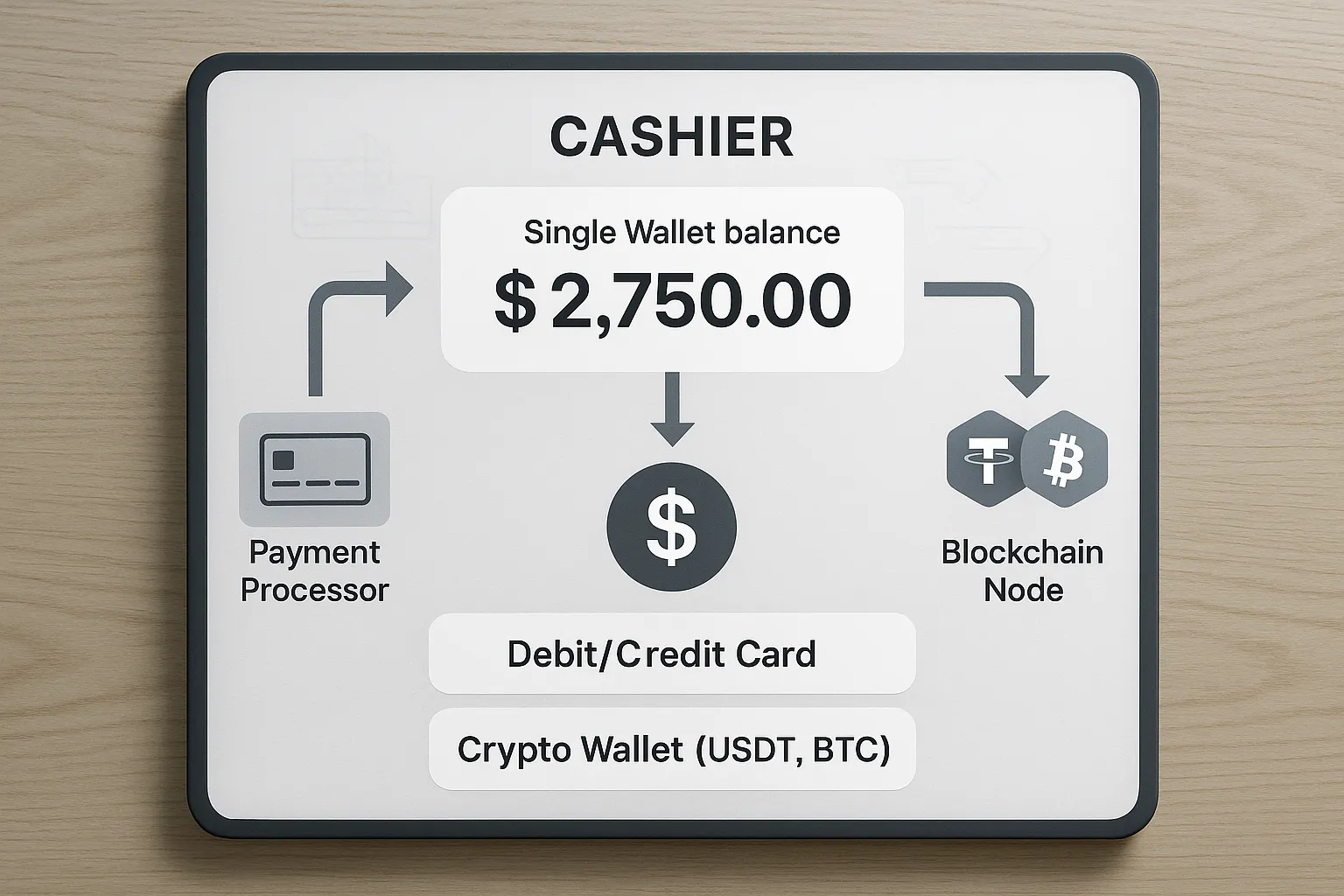

Hybrid cashier: The best of both worlds

Rather than choosing, high-performing brands build a hybrid cashier that lets the player switch fluidly between rails. Key best practices:

- Unified wallet: The player sees one balance. Behind the scenes, you tokenise deposits into stable internal credits.

- Smart routing: The gateway decides whether to process via card, ACH, or on-chain based on cost and risk.

- Real-time FX: Lock deposit value the moment the transaction hits mempool to eliminate volatility.

- Tiered KYC: Light verification for small fiat deposits; full KYC + proof-of-funds for large crypto inflows. Built-in orchestration in a platform such as Fullhouse slashes manual work.

Key takeaways for product managers and CFOs

- Crypto players are fewer but worth more. Expect 2–4× the LTV but layer on volatility safeguards.

- Payment diversity improves acquisition. Affiliates convert better when more cashier logos show up on landing pages.

- Cost discipline matters. Routing just 20 % of your card volume to on-chain stablecoins can shave 100 bps off processing spend—often your entire CRM budget.

- Regulation is stabilising. With MiCA and emerging U.S. frameworks, compliance risk is shifting from “unknown” to “manageable”.

- Technology is turnkey. Platforms like Fullhouse natively support multi-currency cashier modules, on-chain settlements, and real-time risk scores, making the decision less about IT bandwidth and more about acquisition strategy.

Action plan: How to pilot crypto without derailing operations

- Start with a capped rollout: Offer BTC and USDT to VIP segments first. Monitor fraud KPIs and churn.

- Enable instant swaps to stablecoins: Reduce BTC/ETH volatility by converting to USDT on receipt.

- Adjust bonus engine rules: Prevent multiple-wallet abuse with device fingerprinting and velocity checks.

- Educate support staff: Create canned responses for blockchain confirmation times, gas fees, and privacy questions.

- Market it smartly: Crypto Twitter, Telegram communities, and streamers yield up to 3× higher CTR on crypto cashier banners.

Conclusion: It’s (mostly) not a choice—do both, but know your goals

If your KPI is gross player volume, fiat remains essential. If your KPI is profit per player and operational efficiency, crypto outperforms in 2025. The optimal mix is dynamic: as licensing frameworks mature and stablecoin use rises, expect the LTV gap to shrink but not disappear.

With an all-in-one platform like Fullhouse iGaming Platform, you can toggle payment rails without re-coding your cashier, aggregate analytics across both rails, and let real-time data decide the best route for each transaction.

In short: let players pay how they want—then let the data show you which gateway truly drives value.