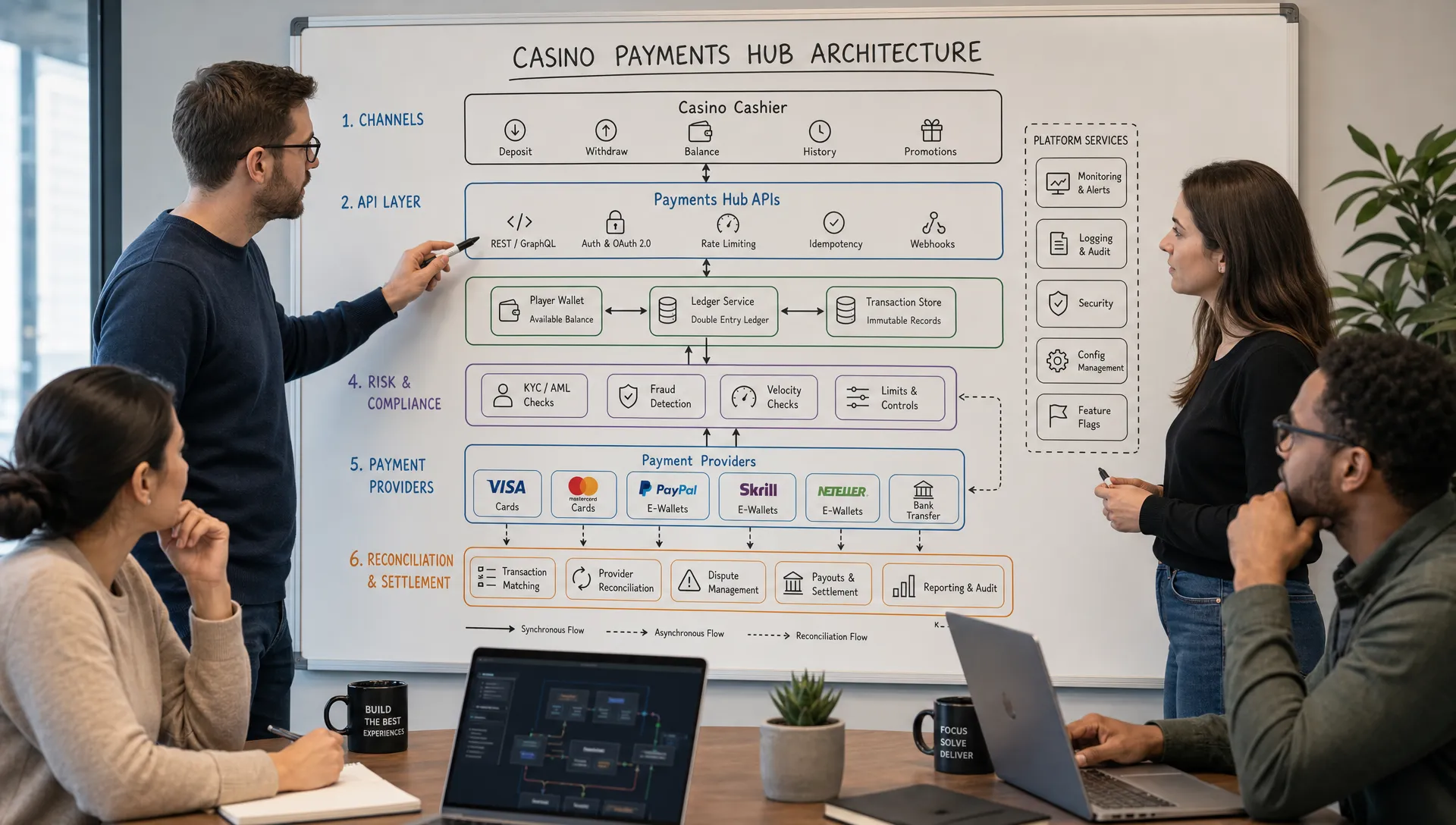

A casino payments hub is the control layer that sits between your cashier, wallet, payment service providers, risk tools, compliance checks, and finance operations. Done well, it lets an online casino add payment methods, route deposits intelligently, accelerate withdrawals, reduce reconciliation work, and support crypto or fiat rails without rebuilding the whole stack every time a market changes.

The key is openness. A payments hub built with open APIs should not be a black box that forces every new payment method through a single vendor roadmap. It should expose clear interfaces for deposits, withdrawals, wallet updates, KYC events, fraud checks, provider webhooks, settlement files, and reporting. That is what makes the hub adaptable enough for global iGaming growth.

This guide breaks down how to design a casino payments hub with open APIs, from architecture and ledger design to fraud controls, crypto readiness, and rollout planning.

What a casino payments hub actually does

A payment gateway processes transactions. A casino payments hub coordinates the entire money movement lifecycle around the player account.

That distinction matters. In iGaming, a payment is not just a card authorization or bank transfer. It affects player balance, bonus eligibility, withdrawal limits, fraud risk, AML monitoring, customer support, affiliate economics, and accounting. If those systems do not speak the same language, the operator ends up with duplicated balances, missing settlements, slow withdrawals, and manual finance work.

A strong payments hub should be able to answer questions like:

- Has the player passed the required checks for this transaction?

- Which payment method should be shown first for this market and currency?

- Which provider should receive the transaction if the primary route is down?

- When should a deposit be credited to the casino wallet?

- Has a withdrawal been reserved, approved, paid, rejected, or reversed?

- Do provider settlements match internal ledger entries?

If you are modernizing an existing setup, start by mapping today’s payment flows before writing new code. Spinlab’s guide on how to audit your casino payments stack is a useful companion for identifying gaps in cashier UX, provider routing, ledger integrity, KYC, AML, and reconciliation.

The core layers of an open API payments hub

A payments hub should be modular, but not fragmented. Each layer needs a clear responsibility, stable APIs, and reliable event handling.

| Layer | Main responsibility | Why it matters in casino payments |

|---|---|---|

| Cashier API | Presents available deposit and withdrawal methods to the player | Supports localization, mobile UX, limits, and method ordering |

| Orchestration layer | Routes transactions to PSPs, banks, wallets, or crypto providers | Enables fallback routing, cost optimization, and market expansion |

| Wallet and ledger | Records player balances and financial movements | Protects balance accuracy and supports auditability |

| Risk and compliance | Runs KYC, AML, fraud, sanctions, and velocity checks | Reduces regulatory and fraud exposure |

| Provider adapters | Normalizes different payment gateway and PSP integrations | Lets the operator add or replace providers faster |

| Reconciliation and reporting | Matches internal transactions with provider settlements | Gives finance teams confidence in deposits, withdrawals, fees, and reserves |

Open APIs make these layers replaceable and extensible. For example, an operator should be able to add a new PSP adapter without changing the wallet ledger, or test a crypto onramp without rewriting the cashier.

This is also where platform choice matters. If the underlying iGaming platform does not expose wallet, player, transaction, and reporting APIs, the payments hub becomes a workaround instead of a true operating layer. For a broader evaluation framework, see Spinlab’s guide on how to choose casino software with open APIs.

Start with a reference architecture

A practical casino payments hub usually follows this pattern:

The player starts in the cashier. The cashier calls the platform API to fetch eligible payment methods based on market, currency, device, account status, KYC state, risk score, and configured limits. When the player selects a method, the payments hub creates a payment intent, runs pre-transaction checks, routes the transaction to the selected provider, receives asynchronous provider updates through webhooks, and updates the wallet only when the correct final or provisional state is reached.

For withdrawals, the flow is stricter. The hub should reserve funds in the wallet, check KYC and AML rules, run fraud controls, submit the payout to the provider, then release, settle, or reverse the reservation depending on the provider result.

The important principle is simple: providers should not be the source of truth for player balance. The internal ledger should be. Payment providers report events, but the casino platform decides how those events affect the wallet.

Design APIs around the payment lifecycle

Open APIs are only useful when they model real operational states. A generic “success” or “failure” callback is not enough for iGaming, where transactions can be pending, challenged, reversed, disputed, partially settled, or manually reviewed.

A good payments hub starts with a canonical lifecycle. For deposits, common states include initiated, pending player action, processing, succeeded, failed, reversed, disputed, and settled. For withdrawals, common states include requested, reserved, pending review, approved, processing, paid, rejected, reversed, and settled.

The exact naming can vary, but the principle should not: every state transition must be intentional, logged, and safe to replay.

| API concept | Purpose | Example use case |

|---|---|---|

| Payment intent | Creates a normalized transaction before provider routing | A player starts a card, bank, e-wallet, or crypto deposit |

| Payout request | Reserves and initiates a withdrawal | A player requests a withdrawal to an approved method |

| Payment method API | Lists available options for a player context | Cashier shows local methods for Canada, Brazil, or the EU |

| Webhook receiver | Accepts asynchronous provider events | PSP sends succeeded, failed, chargeback, or settlement updates |

| Ledger entry API | Records balance movements | Deposit credit, withdrawal reserve, bonus adjustment, reversal |

| Reconciliation API | Imports and matches provider reports | Finance compares PSP settlement files with internal records |

Every write endpoint should support idempotency keys. This prevents duplicate deposits or duplicated withdrawal reservations when a player refreshes the cashier, a provider retries a webhook, or a network call times out.

Webhook handling should also be idempotent. A provider may send the same event more than once, or events may arrive out of order. The hub should store the raw provider event, verify signatures, map it to the canonical transaction model, and apply only valid state transitions.

Build the ledger before adding more payment methods

Many casino payment problems start with a tempting shortcut: integrating one payment gateway directly into the cashier, then adding another, then another. It works at first, but the operator soon has provider-specific balance logic scattered across services.

A casino payments hub should be ledger-first. That means every balance movement is recorded as a structured financial event, not as a side effect of a PSP callback.

At minimum, the ledger should separate:

- Real-money cash balance

- Bonus balance and wagering-related adjustments

- Pending withdrawal reservations

- Provider fees and reversals

- Chargebacks, refunds, and disputed transactions

- Manual adjustments with operator identity and reason codes

For higher integrity, many operators use double-entry accounting principles. In simple terms, every movement has an equal and opposite entry, which helps finance teams trace funds from player wallet activity to provider settlement and operator accounts.

This is especially important when adding new payment rails. Cards, open banking, e-wallets, vouchers, bank transfers, and crypto do not settle the same way. If each method changes balances differently, the platform becomes fragile. Spinlab covers this specific challenge in its article on how to add new payment methods without breaking your ledger.

Use provider adapters, not provider-specific product logic

A payments hub should normalize provider complexity behind adapters. Each PSP, acquirer, open banking provider, or crypto onramp has different field names, error codes, redirect flows, webhook formats, settlement reports, and refund rules. The rest of the casino platform should not have to care.

A provider adapter translates between the external provider and your internal payment model. It should handle authentication, request formatting, provider-specific metadata, webhook verification, status mapping, and retry behavior.

This gives the operator more leverage. If one provider becomes expensive, unreliable, or unsuitable for a market, you can route around it or replace it without reworking the wallet, cashier, reporting, and risk systems.

It also makes testing safer. You can run contract tests against each adapter, simulate provider events, and confirm that every provider maps into the same internal lifecycle.

Add intelligent routing without creating balance risk

Payment routing is one of the biggest reasons to build a hub. The operator can choose the best route for a transaction based on cost, approval rate, provider uptime, market, currency, player segment, risk score, and payment method.

Routing logic might consider factors such as:

- Player country and currency

- Deposit or withdrawal amount

- Provider availability and recent error rates

- Method type, such as card, bank transfer, e-wallet, voucher, or crypto

- Player risk profile and transaction history

- PSP fees, settlement timing, and chargeback exposure

The danger is duplicate processing. If the first route times out and the hub retries with another provider, the system must know whether the original attempt might still succeed. That is where payment intents, idempotency, provider reference IDs, and cautious state transitions become essential.

A safe routing engine never credits a player simply because a request was sent. It credits based on a verified event, a trusted provider response, or a defined provisional-credit policy approved by risk and finance teams.

Build for fiat, crypto, and hybrid cashier journeys

Modern casino operators increasingly need to support both fiat and crypto payment experiences. The technical challenge is not only accepting digital assets. It is making crypto fit into the same operational model as fiat: limits, KYC, AML, risk, wallet crediting, refunds, reporting, and reconciliation.

A crypto-ready solution may include crypto onramp providers, merchant custodial wallets, blockchain confirmation tracking, exchange-rate handling, and wallet risk screening. The payments hub should normalize these flows without treating crypto as an isolated side system.

For example, a crypto deposit may need to move through states like address generated, pending blockchain confirmation, confirmed, credited, flagged for review, or rejected. A fiat card deposit may use different provider events, but both should ultimately map to the same internal ledger rules.

Operators should also consider AML obligations around virtual assets. The FATF Recommendations provide a widely referenced global framework for anti-money laundering and counter-terrorist financing controls, although specific requirements vary by jurisdiction. Always validate market-specific rules with qualified legal and compliance advisors.

Treat compliance and fraud as first-class API services

Payments, KYC, AML, and fraud prevention cannot be bolted on at the end. They should be part of the transaction decisioning flow.

Before a deposit or withdrawal is allowed, the hub may need to check player identity status, country restrictions, sanctions results, self-exclusion status, payment method ownership, deposit limits, affordability requirements, velocity patterns, and bonus abuse signals. Which checks apply depends on the market, license, risk policy, and payment method.

Open APIs help by allowing the payments hub to call specialized services at the right moment. A KYC provider can return identity status. A fraud engine can return a risk score. A compliance service can evaluate AML rules. The platform can then approve, block, review, or limit the transaction.

Security also matters at the API layer. The OWASP API Security Top 10 is a practical reference for common API risks such as broken object-level authorization, weak authentication, excessive data exposure, and unsafe consumption of APIs. For card payments, operators and vendors should also align with the relevant PCI Security Standards Council requirements. In many cases, tokenization and hosted payment fields can reduce direct exposure to sensitive card data.

Make reconciliation non-negotiable

A payments hub is not complete until finance can reconcile it.

Reconciliation compares internal ledger records with external provider data. It answers whether deposits, withdrawals, refunds, chargebacks, fees, rolling reserves, and settlements match what the operator expected.

At a practical level, the hub should store:

- Internal transaction ID

- Player ID and wallet account reference

- Provider name and provider transaction reference

- Payment method and currency

- Gross amount, net amount, fees, and exchange rate where applicable

- Transaction status and state history

- Settlement batch or report reference

- Raw webhook and reconciliation file references

When reconciliation is designed early, disputes become easier to investigate. Support teams can see what happened. Finance can close periods faster. Compliance teams can review suspicious flows with a complete audit trail.

Real-time dashboards are useful, but they should not replace structured settlement matching. A dashboard shows what is happening now. Reconciliation proves what actually settled.

Plan observability, alerts, and incident workflows

Payments are operational infrastructure. If a major deposit method fails on a Friday night, the operator needs to know immediately.

A production-grade payments hub should monitor transaction approval rates, failure codes, provider latency, webhook delays, payout processing time, reconciliation breaks, chargeback trends, KYC drop-off, and cashier conversion. It should also alert teams when a provider’s performance drops below a defined threshold or when unusual transaction patterns appear.

Incident workflows should be documented before launch. For example, if a PSP webhook is delayed, should deposits remain pending, be provisionally credited, or be blocked? If an open banking provider is down, which method becomes the fallback? If a crypto network is congested, how many confirmations are required before crediting?

These are business decisions as much as technical decisions. The hub should make them configurable, auditable, and consistent.

A practical rollout roadmap

Building a casino payments hub does not need to happen in one massive release. A phased rollout reduces risk and gives teams time to validate assumptions.

- Map current payment flows: Document every deposit, withdrawal, refund, chargeback, manual adjustment, KYC check, provider webhook, settlement file, and finance report.

- Define the canonical transaction model: Standardize statuses, reason codes, provider references, player references, currencies, amounts, fees, and timestamps.

- Design the wallet and ledger rules: Decide exactly when funds are credited, reserved, released, reversed, disputed, or written off.

- Create provider adapters: Normalize your first PSP, bank rail, or crypto onramp before adding more providers.

- Add risk and compliance decision points: Integrate KYC, AML, fraud, sanctions, limits, and manual review workflows into the payment lifecycle.

- Build reconciliation workflows: Import provider reports, match settlement records, surface breaks, and create finance-friendly exports.

- Instrument observability: Track conversion, latency, errors, provider health, webhook performance, payout speed, and reconciliation status.

- Roll out by market or method: Start with a controlled segment, compare results, then expand to more payment methods, currencies, and regions.

The most important rule is to avoid mixing migration with uncontrolled expansion. Stabilize the hub with a small number of methods first, then use the open API architecture to scale.

Build versus buy: when a platform approach makes sense

Some large operators build payment hubs from the ground up. That can make sense when they have mature engineering teams, complex licensing footprints, and high transaction volume. But for many online casino brands, building every layer internally slows down launch and creates ongoing maintenance overhead.

A modular white label casino platform can shorten that path if it already supports the foundations operators need: fiat and crypto payments, open API integration, KYC and AML workflows, fraud prevention, game aggregation, mobile optimization, real-time analytics, backoffice controls, multi-currency support, crypto onramps, custodial wallets, and configurable casino operations.

Spinlab is built around that modular approach. It gives operators a faster way to launch and scale an online casino while keeping the platform flexible enough for payment integrations, market localization, and operational control. For teams that want a more Shopify-like setup experience without giving up core iGaming infrastructure, a platform-led approach can be more practical than stitching together every component from scratch.

Frequently Asked Questions

What is a casino payments hub? A casino payments hub is the orchestration layer that connects the cashier, wallet ledger, payment providers, KYC, AML, fraud tools, reconciliation, and reporting. It manages the full lifecycle of deposits and withdrawals, not just payment processing.

How is a payments hub different from a payment gateway? A payment gateway processes a transaction through a specific provider or acquiring route. A payments hub coordinates multiple gateways and payment methods while controlling routing, wallet updates, compliance checks, risk rules, and reconciliation.

Why are open APIs important for casino payments? Open APIs let operators add payment methods, integrate risk tools, connect crypto onramps, automate reporting, and replace providers without rebuilding the entire platform. They reduce vendor lock-in and make market expansion easier.

Should the PSP or the casino ledger be the source of truth? The casino ledger should be the source of truth for player balance. PSPs provide transaction events and settlement data, but wallet credits, reversals, reserves, and adjustments should be controlled by the platform ledger.

Can one payments hub support both fiat and crypto? Yes, if it uses a canonical transaction model. Fiat and crypto flows have different provider events and settlement mechanics, but they can still map into shared wallet, risk, compliance, and reconciliation processes.

What should operators prioritize first when building a payments hub? Start with transaction modeling, ledger rules, idempotency, webhook handling, and reconciliation. Adding more payment methods is easier and safer once those foundations are stable.

Build a more flexible casino payments layer

A casino payments hub is not just a technical upgrade. It is the foundation for faster market entry, better cashier conversion, safer withdrawals, cleaner reconciliation, and more control over the player money journey.

If you want to build on a modular iGaming platform with open API integration, crypto and fiat payment support, compliance tooling, fraud prevention, analytics, game aggregation, and a customizable backoffice, Spinlab can help you launch and scale with less operational complexity.