Deposit approvals are one of the few levers in iGaming that can move revenue immediately. But most teams hit the same wall: every time you “open the gate” to lift approval rates, fraud, chargebacks, and bonus abuse creep up behind it.

The goal of this playbook is different: improve casino deposit approval rates without more fraud by reducing false declines, fixing avoidable technical and data issues, and using risk-based step-up controls instead of blunt blocking rules.

Start by measuring the right approval rate

A single “approval rate” number is almost always misleading. To improve outcomes without increasing fraud, you need two views of the same funnel:

- Payments view (attempts, auth outcomes, PSP performance)

- Risk view (fraud loss, chargebacks, bonus abuse cost, manual review load)

Here’s a simple metric set that keeps both teams honest.

| Metric | What it answers | Why it matters for “no more fraud” |

|---|---|---|

| Attempt-to-authorized rate | “Are issuers/PSPs approving deposits?” | Pure approval signal, but can be gamed by accepting bad traffic |

| Authorized-to-credited rate | “Are successful auths becoming playable balance?” | Catches wallet-credit bugs, async APM delays, reconciliation gaps |

| Fraud-adjusted approval rate | “How many approved deposits stay legitimate?” | Forces the trade-off into one KPI instead of internal debates |

| Chargeback rate (by rail, BIN, cohort) | “Are approvals turning into disputes?” | Detects approval gains that are actually future losses |

| Manual review rate and SLA | “How much human friction did we add?” | Manual queues are hidden conversion killers |

Practical definition:

- Fraud-adjusted approval rate = (Deposits credited and not reversed for confirmed fraud/chargeback within your measurement window) / (Deposit attempts)

Pick a window that matches your reality (for cards, many operators watch both a 7-day early signal and a 45 to 90-day maturity view).

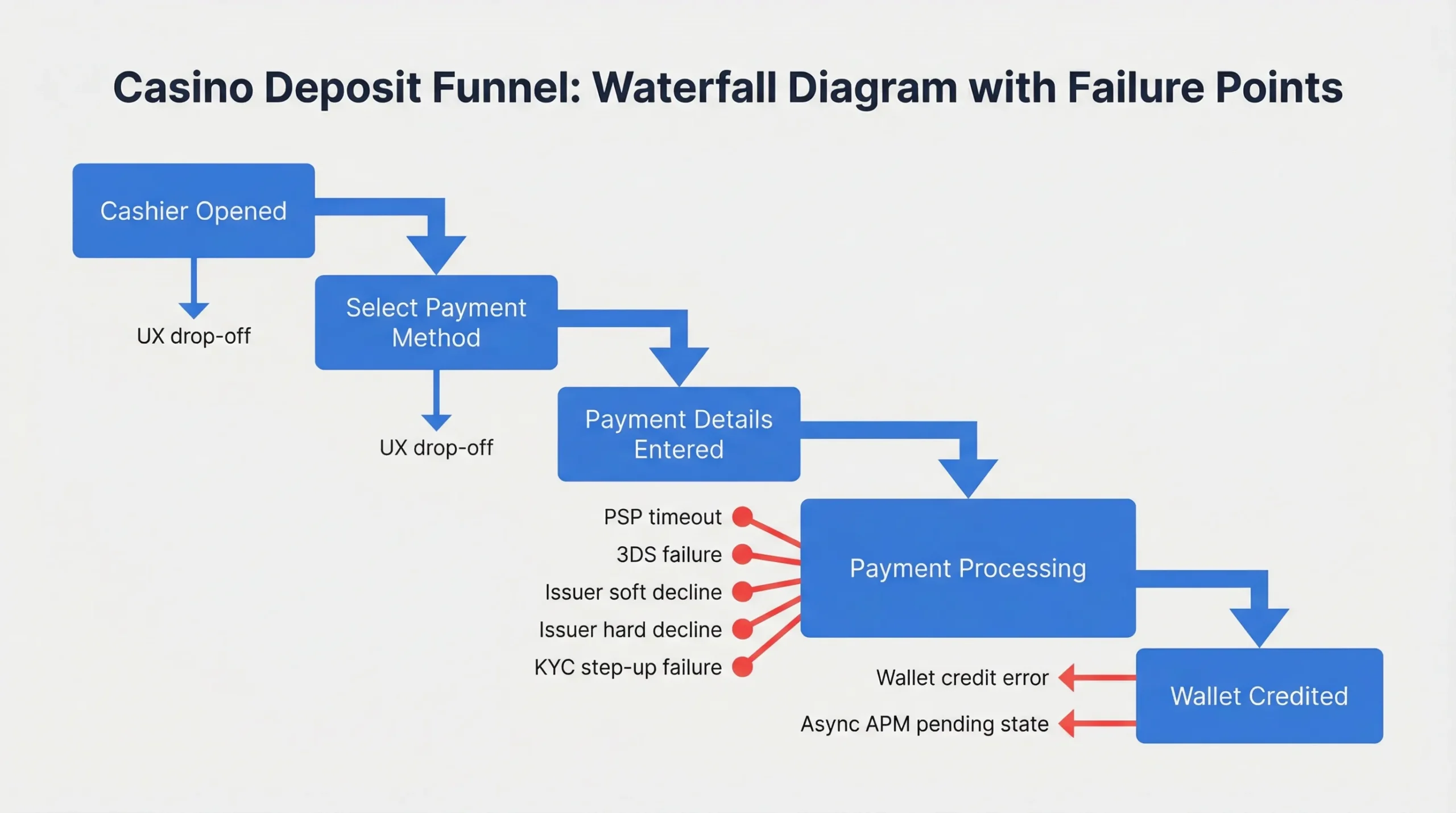

Build a decline “waterfall” before you change rules

A lot of “low approval” is not issuer decline. It’s messy plumbing.

Map the deposit journey as a waterfall so you can localize the leakage:

- Cashier opened

- Deposit initiated

- Payment request created

- PSP response received

- Issuer authorized (or APM accepted)

- Funds settled (async rails)

- Wallet credited

- Player returned to game

If you cannot answer “where exactly did it fail?” you will end up guessing, usually by loosening fraud checks.

Classify declines into a small, operational taxonomy

Keep it boring and consistent. You want categories that route to an owner.

| Decline category | Typical signals | Primary owner |

|---|---|---|

| Issuer hard decline | Do not honor, invalid account, lost/stolen | Payments ops, acquirer, routing |

| Issuer soft decline / auth required | 3DS required, SCA needed, insufficient funds | Payments + UX + risk |

| PSP/provider failure | timeouts, 5xx, provider down | Engineering + PSP AM |

| Risk decline | device/IP velocity, negative list hit | Fraud/risk |

| Compliance step-up fail | KYC required, sanction screen hit | Compliance + product |

| Data/format error | invalid field, currency mismatch | Engineering |

| User abandon | no submission, rage click, field errors | Product + UX |

This classification is where “higher approval without more fraud” becomes possible, because it separates false declines (fixable) from true risk (should be blocked or stepped-up).

Fix the hidden approval killers that look like fraud controls

Many casinos accidentally create their own decline spikes by shipping “risk controls” that are really UX and data issues.

1) Remove unnecessary mismatches that trigger issuer risk models

Issuers and PSP fraud tools are sensitive to inconsistencies. Common offenders:

- Geo mismatch: IP country, phone country code, and BIN country do not align (especially for travelers and expats).

- Name/address mismatch: avoid forcing “billing address” when you do not need it for your PSP flow.

- Currency confusion: player sees EUR, request is sent as USD, or you apply FX after auth.

- Descriptor ambiguity: unclear merchant descriptor leads to “friendly fraud” later.

These are not theoretical. They directly influence authorization outcomes and post-approval disputes.

Implementation tip: log a compact “risk context” object on every deposit attempt (country, BIN country, device type, IP ASN, amount, currency, account age, KYC state, previous approvals). Even if you do not build a full decision engine today, this single object makes analysis possible.

2) Make 3DS/SCA a conversion tool, not a blanket requirement

For regulated markets, SCA is unavoidable, but your usage of it can lift approvals.

- Use 3DS when the issuer signals it, or when your risk score crosses a threshold.

- Avoid forcing step-up on every low-value, low-risk repeat depositor.

- Treat 3DS failures as a recoverable state, not a dead end.

If you need a standards reference, EMVCo maintains the 3-D Secure program documentation at EMVCo.

3) Don’t “KYC surprise” your highest-intent depositors

A common pattern: a player completes registration, tries to deposit, then hits a full KYC wall with unclear instructions. The result is a rage-quit that looks like “low approvals.”

Instead, use progressive verification:

- Allow low-risk deposits to proceed with light checks (where your licensing/regulatory model allows).

- Trigger step-up KYC when risk increases (higher amounts, unusual geo/device changes, rapid retries).

- Show a clear pending state and explain why verification protects both the player and the casino.

This kind of trust-building flow is not unique to gambling. Other high-value industries do it too, including investment onboarding, where you’ll often see clear sequencing and expectations similar to Azimira’s real estate investment onboarding experience.

Improve approvals using “decline-aware recovery,” not blind retries

When a deposit fails, many operators do one of two bad things:

- Bad approach A: let the player spam retry (higher issuer risk, more fraud surface).

- Bad approach B: stop the flow completely (lost FTD).

A better strategy is decline-aware recovery: do the minimum change that increases the probability of success, while limiting fraud and operational load.

Recovery patterns that usually work (and why)

Soft decline, auth required (3DS/SCA)

- Offer an immediate 3DS retry inside the same cashier session.

- Keep the amount constant for the first retry (amount changes can look like testing behavior).

Insufficient funds or limit issues

- Suggest a lower preset amount (with one tap).

- Offer a local rail alternative (APM, pay-by-bank) for faster success.

PSP timeout / technical error

- Do not show “declined.” Show “We couldn’t reach the bank, try again” and retry once with idempotency.

- Route to an alternative provider only after you confirm it is not a duplicate auth risk.

Risk decline

- Step-up (3DS, OTP, or KYC) instead of “try again.” Repeated risk declines are a strong fraud signal.

Add strict idempotency to protect approval rates and fraud controls

Without idempotency keys, retries create duplicate auths, double credits, or reconciliation anomalies. Those anomalies get interpreted as fraud, and teams respond by tightening rules, which lowers approvals.

If you do nothing else technically, implement:

- An idempotency key per deposit attempt

- A deterministic mapping between PSP transaction IDs and wallet ledger entries

- A clear pending state for async rails

Reduce false positives with risk-based step-up, not higher blocking

When fraud rises, teams often respond with broader declines. That is exactly how approval rates die.

A cleaner pattern is to keep your baseline permissive and use graduated actions:

- Approve normally

- Approve with step-up authentication

- Hold for review (rare, with tight SLA)

- Decline

Signals that tend to be high value for step-up decisions

You do not need hundreds of features. A small set often captures most of the risk delta:

- Account age (minutes since registration)

- Deposit velocity (attempts per hour, failed attempts per hour)

- Device reuse (same device across multiple accounts)

- IP/ASN anomalies (datacenter IPs, sudden country changes)

- Payment instrument reuse (same card across accounts)

- KYC state (unverified, pending, failed)

The key is governance: tune your thresholds against both approval uplift and fraud-adjusted approval rate, not approvals alone.

Expand your payments mix to lift approvals without loosening risk

Card approvals vary heavily by geography, issuer behavior, and player segment. If your cashier is card-first everywhere, you will fight a losing battle in certain markets.

Adding additional rails can raise overall approval rates while reducing fraud exposure in specific cases:

- Pay-by-bank/open banking: fewer chargebacks by design, strong user authentication in many flows.

- Local APMs: higher acceptance where cards are weak.

- Crypto deposits and onramps: can reduce chargeback exposure, but must be paired with strong AML/KYT and wallet controls.

The strategic point is not “more payment methods.” It is more payment methods that fit the player’s jurisdiction and risk profile, with clear governance on when each rail is offered.

If you want a deeper dive on routing logic, see Spinlab’s primer on casino payment orchestration and routing for higher approval.

Use analytics that connect approvals to fraud outcomes

Approval optimization fails when analytics are siloed:

- Payments dashboards show approvals and provider health.

- Fraud dashboards show disputes and abuse.

- Product dashboards show funnel conversion.

You need one shared view that can answer: Which approval gains are safe? Which are losses in disguise?

A simple weekly “approval quality” slice list:

- By country + currency

- By payment rail

- By BIN (first 6 to 8) and issuer

- By player lifecycle stage (FTD, first week, repeat depositor)

- By risk tier (low, medium, high)

A two-sprint implementation plan (practical and low drama)

Most teams can make meaningful progress in two sprints without re-platforming.

Sprint 1: Instrumentation and decline truth

Focus on visibility and classification.

- Implement event logging for deposit stages (initiate, request, response, 3DS start/complete, credit success/fail).

- Add a standardized decline taxonomy and make it mandatory in dashboards.

- Create a daily report: top decline categories by volume and by lost value.

Sprint 2: Targeted fixes and controlled experiments

Pick 2 to 3 changes with a clear hypothesis.

| Experiment | Hypothesis | Primary KPI | Guardrail |

|---|---|---|---|

| Risk-based 3DS step-up | Fewer issuer soft declines convert to approvals | Attempt-to-authorized | Chargeback rate |

| Decline-aware recovery UI | Fewer players abandon after a soft decline | Authorized-to-credited | Failed-attempt velocity |

| Add a local rail in one geo | Players switch away from low-approval cards | Overall approval rate in geo | Fraud-adjusted approval rate |

Run these as controlled rollouts (by country, by cohort, or by a percentage split), and keep a rollback plan.

Where an all-in-one platform helps (and where it doesn’t)

Improving approval rates without more fraud is mostly about systems working together: cashier UX, payments, fraud controls, KYC/AML, and real-time analytics.

If those components are fragmented across vendors, you pay an integration tax in three places:

- inconsistent decisioning (payments and fraud disagree)

- missing end-to-end logging (no “truth” about declines)

- slow iteration (every change needs multiple parties)

Spinlab’s modular iGaming platform is built around unifying those pieces (fiat and crypto payments, compliance, fraud prevention, analytics, game aggregation) so operators can iterate on approvals with fewer moving parts. If you’re evaluating whether a consolidated stack would help your specific approval bottlenecks, you can start at spinlab.studio.

The bottom line

Higher deposit approvals without more fraud do not come from one “magic PSP” or from loosening rules. They come from:

- measuring approvals with fraud outcomes attached

- building a decline waterfall so you fix the right layer

- using decline-aware recovery and idempotent retries

- applying risk-based step-up instead of broad blocking

- offering the right rails per market and player segment

If you treat approvals as a product-and-risk system, not just a payments metric, you can lift conversion and keep your loss curve flat.