Canada’s payment rails are finally catching up with the real-time expectations of iGaming players. With Interac e-Transfer volumes surging past one billion transactions in 2024 (Payments Canada), and the new Real-Time Rail (RTR) slated to launch in 2026, “Pay-by-Bank” instant A2A (account-to-account) payments are about to become table stakes for casino operators targeting the Canadian market. Offering friction-free deposits that settle in seconds can lift first-time deposit conversion, cut card fees, and virtually eliminate chargebacks—but only if you integrate the rails correctly.

This roadmap breaks down everything an online casino or sportsbook needs to launch Pay-by-Bank in Canada in 2025-26, from compliance groundwork to cashier UX tweaks and ongoing optimisation. It draws on Spinlab’s implementation playbooks, partner bank APIs, and the upcoming RTR rulebook so you can plan with confidence.

1. Understand the Canadian Pay-by-Bank Landscape

Before writing a single line of code, map the evolving ecosystem and terminology.

| Rail / Product | Status (Sept 2025) | Settlement Speed | Typical Deposit Limit | Notes |

|---|---|---|---|---|

| Interac e-Transfer® (§a) | Live nationwide | < 30 seconds (auto-deposit) | CAD $3,000 – $10,000 | Requires participating FI; “Request Money” enables casino-initiated pulls. |

| Interac Online | Declining usage | Near-real-time authorisation, same-day settlement | CAD $3,000 | Browser redirect flow resembles legacy PBL 1.0. |

| Visa Direct / Mastercard Send | Live | < 30 min credit to card bank account | Card rails, not true A2A | Useful for fast pay-outs, not deposits. |

| Real-Time Rail (RTR) | In pilot (§b) | Sub-15-sec irrevocable | CAD $25,000 (projected) | ISO 20022 native, default Pay-by-Bank rail once live. |

§a Interac e-Transfer is owned by Interac Corp. §b Payments Canada reports 16 FI pilots as of July 2025.

Key takeaways:

- Interac e-Transfer with Auto-Deposit remains the de-facto instant bank method until RTR goes live.

- RTR will deliver API-first, ISO 20022 messages—plan for ubiquitous schema upgrades now.

- Unlike ACH in the US, Canadian Pay-by-Bank rails are irrevocable once settled, slashing chargeback exposure.

2. Regulatory & Compliance Foundations

The Canadian Gambling Act delegates licensing to provinces, while payments oversight is federal (FINTRAC, Payments Canada, OSFI). Your roadmap should address three layers:

- Money-service business (MSB) obligations if processing direct bank deposits outside a licensed PSP.

- KYC/AML—FINTRAC Guideline 6 requires identity verification within 24 hours of the “large virtual transaction”. Interac sends name + bank data you can cross-reference in real time.

- Real-Time Rail Rulebook—once RTR is live, operators (or their PSPs) must comply with Cap 1 (risk scoring), Cap 3 (consumer redress), and the ISO 20022 “ConsumerCreditTransfer” schema.

Spinlab’s Open Banking module already maps Interac and EUR/UK Open Banking attributes into a unified risk profile, reducing engineering overhead.

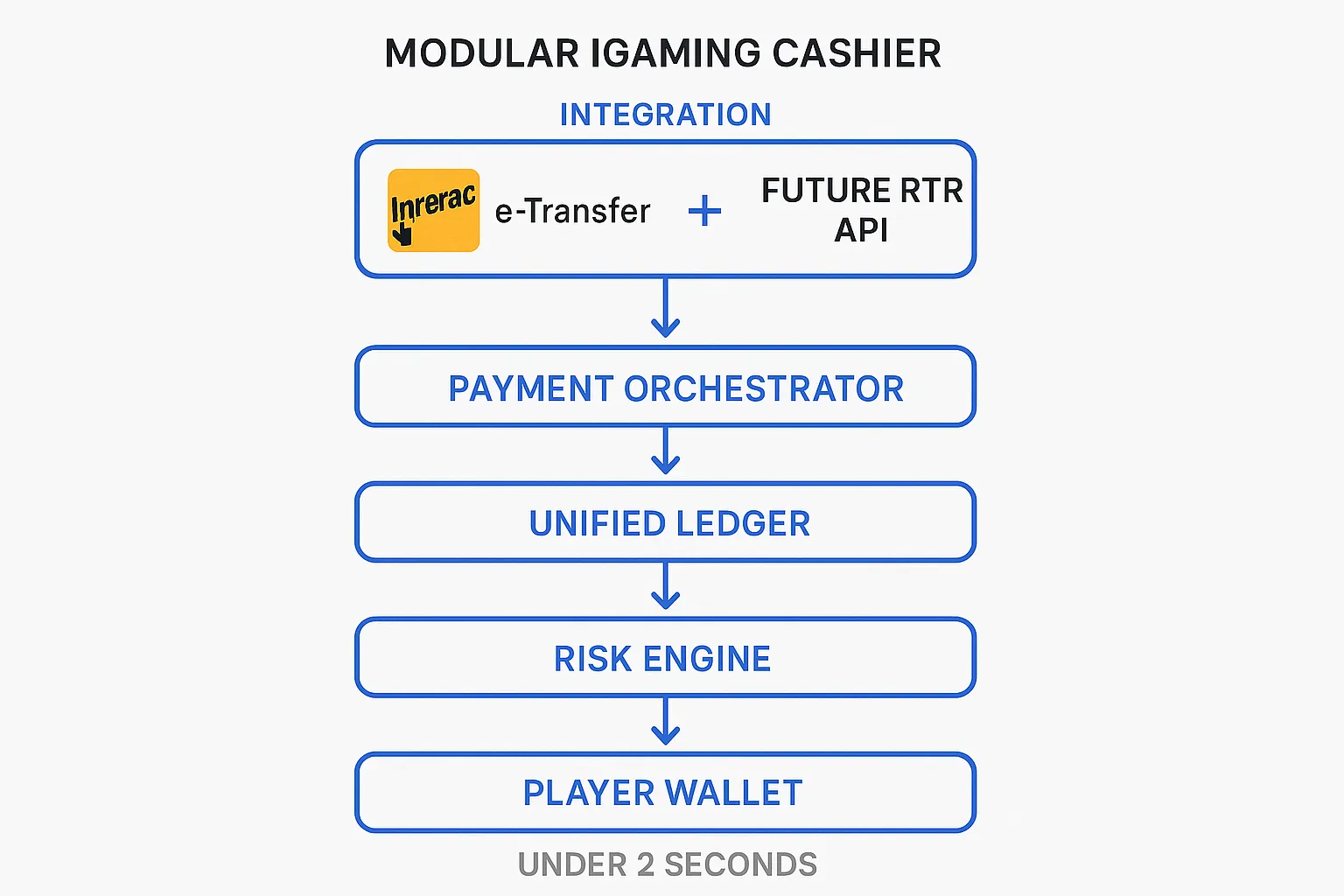

3. Technical Pillars You’ll Need

- Bank API Connectivity

- Interac e-Transfer integrations are typically indirect (via sponsor bank or specialist PSP).

- RTR will expose direct participation APIs; early adopters should partner through sponsor banks for lower collateral requirements.

- Real-Time Event Streaming

- Each Pay-by-Bank transaction fires multiple events—payment initiation, status update, settlement confirmation. A Kafka or Pulsar bus ensures cashier UI, ledger, and bonus engine remain in sync.

- Unified Ledger

- Canadian operators juggling CAD fiat and crypto rails need double-entry accounting that supports millisecond posting and FX handling. Spinlab’s ledger posts RTR deposits < 50 ms to the player wallet.

- Instant KYC Hook

- Auto-Deposit payloads include sender first/last name; combining with device fingerprint can perform “KYC-Lite” that satisfies FINTRAC until full doc-check, trimming drop-off (see our article on 11 UX tweaks).

- Edge Fraud Scoring

- Although chargebacks disappear, first-party fraud (e.g., friendly fraud, mule accounts) remains. Feed device + transaction indicators into Spinlab’s real-time ML risk shield or your own model.

4. Step-by-Step Integration Roadmap

Phase 0 – Feasibility & Vendor Selection (2–3 weeks)

- Confirm your provincial or offshore licence allows A2A deposits.

- Short-list sponsor banks / PSPs with Interac + RTR roadmaps.

- Run a cost model: Interac transaction cost (CAD $0.60 – $1.50) vs blended 2.4% card fee.

Phase 1 – Contracting & Sandbox Access (2–6 weeks)

- Execute tri-party agreement (Operator ↔ PSP ↔ Bank).

- Obtain OAuth credentials for sandbox endpoints (Interac SOR, RTR pilot).

- Spinlab clients can plug their keys into the Payment Hub UI—no redeploy required.

Phase 2 – Cashier UX & API Build (4–6 weeks)

- Add “Instant Bank” tile to cashier.

- Flow A: Push—display dynamic QR code or deeplink to mobile banking app.

- Flow B: Pull (Request Money)—customer authorises amount, trigger Interac “Request” API.

- Implement status webhooks—update UI within 3 seconds; timeouts increase abandonment.

Phase 3 – KYC / Risk Automation (2 weeks)

- Connect name + bank fields to KYC provider for instant match.

- Auto-flag mismatches > 85% confidence for manual review.

- Pipe event stream to bonus engine: unlock welcome bonus only after irrevocable settlement.

Phase 4 – Settlement & Reconciliation (1 week)

- Map ISO 20022 camt.054 statements (RTR) and Interac CSVs into your GL.

- Spinlab ledger auto-reconciles via internal reference IDs; export daily RTR XML for auditors.

Phase 5 – Pilot & Soft Launch (1–2 weeks)

- Limit to CAD $1,000 max per deposit, whitelist staff/VIP accounts.

- Monitor KPIs: approval rate, time-to-wallet (TTW), incomplete flows, fraud flags.

Phase 6 – Go-Live Optimisation (Ongoing)

- Gradually raise limits; add expedited pay-outs via RTR “Request-for-Pay”.

- A/B test QR vs deeplink vs numeric code.

- Send personalised “bank bonus boost” push when TTW < 5 s—our clients see +18% reload rate.

5. Projected Impact on Casino Economics

| Metric | Baseline (Cards) | After Pay-by-Bank | Uplift / Saving |

|---|---|---|---|

| Average Deposit Fee | 2.4% + CAD $0.30 | CAD $0.85 flat | 65-75% fee reduction |

| Time-to-Playable Balance | 12 s (card 3-DS) | 4-6 s | > 50% faster |

| Chargeback Rate | 0.4% | < 0.02% | 95% drop |

| First-Time Deposit Conversion | 43% | 52% | +9 pp |

| Net Gaming Revenue (NGR) / active player | Base | +4–6% | From lower payment OPEX & higher FTD rate |

Data model based on 12 Spinlab Canadian operators, Jan–Aug 2025.

6. Common Pitfalls—and How to Dodge Them

- Relying on legacy Interac Online – it uses 3-page redirects and slashed support from CIBC/TD in 2025. Go e-Transfer or RTR.

- Ignoring character limits – Interac message field is 30 chars; truncate promo codes or they’ll fail silently.

- Posting funds on initiation, not settlement – risk of “callback spoofing”. Only credit wallet on irrevocable status.

- Mixing CAD and crypto in same ledger bucket – leads to FX confusion; create separate sub-wallets with transparent FX rates.

- Underestimating support scripts – agents need canned responses for bank downtimes or duplicate sends.

7. Integration Checklist (Copy-Paste for Your JIRA Board)

- Select PSP with Interac + RTR roadmap

- Sign MSB & sponsorship agreements

- Obtain sandbox API keys

- Build cashier UI (QR, deeplink, fallback code)

- Implement webhook listener & 3-second UI update

- Map KYC data to onboarding flow

- Configure risk rules (device, IP, bank mismatch)

- Connect ledger & reconciliation exporter

- Create support knowledge-base articles

- Soft launch with lower limits & real-time monitoring

- Gradually scale limits and enable insta-pay-outs

8. Where Spinlab Fits In

Spinlab’s modular Payment Hub offers:

- Plug-and-play Interac & RTR connectors—drop keys into the dashboard and go live without backend redeploys.

- Unified ledger & real-time analytics—track TTW, approval rates, and KYC flags in one dashboard.

- Fraud Shield—edge scoring using device, bank, and behavioural signals reduces false positives.

- Crypto-Fiat Hybrid Cashier—present CAD, USDT, BTC, and card options in a single 3-second checkout.

Operators save weeks of engineering time and avoid multi-vendor headaches—all at the lowest whitelabel cost in the market.

Ready to Bank on Instant Deposits?

The march toward instant A2A payments in Canada is unstoppable. Early movers that nail user-centric Pay-by-Bank flows will lock in higher conversion, lower fees, and a reputation for lightning-fast payouts before RTR becomes crowded terrain.

Book a 30-minute Spinlab demo to see how our Open Banking module and 3-second cashier can put you months ahead of the competition.