Open Banking has moved from “nice payments add-on” to a core iGaming conversion lever in many regulated markets. But the operators who win with Pay-by-Bank are rarely the ones who simply “turn it on.” They are the ones who treat it like a first-class payment rail, with its own state machine, ledger logic, risk controls, reconciliation, and UX.

This guide is written for casino founders, CTOs, payment product owners, and compliance leads who want a practical integration blueprint you can hand to engineering and ops.

What “Open Banking” means in iGaming (and what it does not)

In iGaming, “Open Banking” typically refers to account-to-account (A2A) payments initiated via bank APIs (often called payment initiation). Players authenticate with their bank (Strong Customer Authentication in many regions), then approve a transfer to the operator.

Two concepts are commonly mixed up:

- Payment initiation (PIS): used for deposits (and in some setups, withdrawals).

- Account information (AIS): used to read bank data, only with explicit player consent and within regulatory constraints.

Whether and how you can use AIS-style signals for affordability or safer payments depends on jurisdiction, your licensing setup, and your providers’ permissions. If you are operating in Europe or the UK, the high-level regulatory foundation comes from PSD2 and the SCA requirements in the RTS, as summarized by the European Banking Authority and enforced by national regulators.

Integration models: direct, via TPP, or via PSP

Most casinos should not connect bank-by-bank. The operational load (certificates, quirks, uptime variance, dispute handling, coverage changes) becomes a product of its own.

Here are the realistic models operators use:

| Model | What you integrate | Best for | Trade-offs |

|---|---|---|---|

| Open Banking aggregator/TPP | One API that connects to many banks | Fast coverage, less bank fragmentation | Per-transaction fees, dependency on provider uptime |

| PSP with Pay-by-Bank | Pay-by-Bank as a method inside your PSP stack | Simplified procurement, unified reporting | Less control over UX and state handling, provider constraints |

| Direct bank integrations | Individual bank APIs | Niche cases, very large scale with dedicated team | High engineering and compliance overhead |

A common “grown-up” approach is to integrate an aggregator/TPP through a payment orchestration layer so you can route by bank, geography, player segment, or provider health, similar to how you already route cards. (If you are building orchestration internally, align it with the patterns in your cashier routing strategy.)

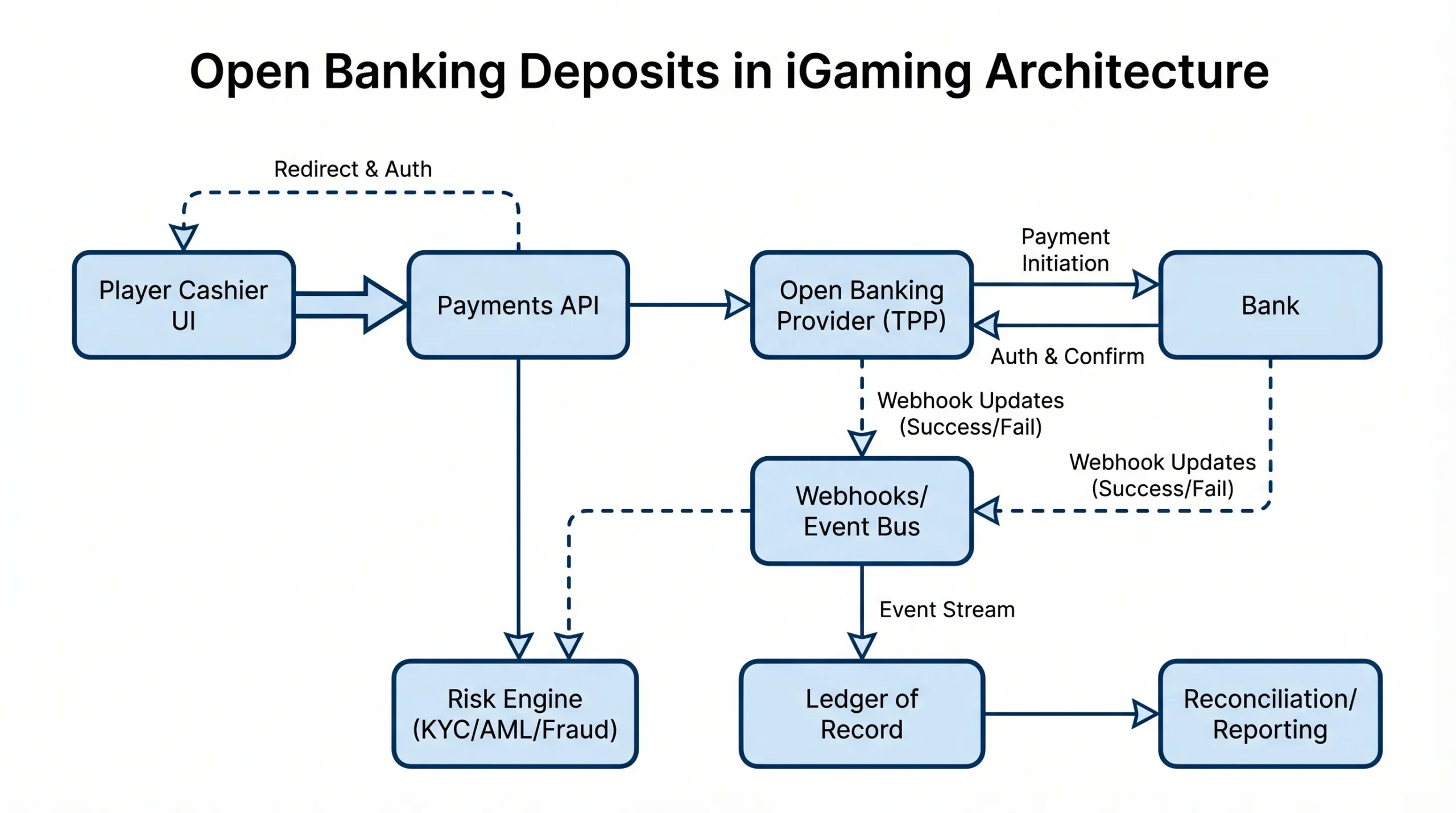

Reference architecture: treat Pay-by-Bank like a real rail

At minimum, you need six components to avoid brittle integrations:

- Cashier UI (web and mobile) that can handle redirects, deep links, pending states, and retries.

- Payments API that creates intents, stores state, and exposes idempotent endpoints.

- Provider connector (TPP/aggregator) handling OAuth, bank selection, and callbacks.

- Webhook listener + event bus to process asynchronous outcomes reliably.

- Ledger of record (double-entry) that posts credits only when conditions are met.

- Reconciliation pipeline that matches ledger vs provider reports vs bank settlement.

Why the ledger and state machine matter more than the API call

Open Banking deposits often “feel” instant, but operationally they are asynchronous. You will see combinations of:

- player-approved but pending execution

- executed but not yet confirmed by your provider

- confirmed but later returned (less common than card chargebacks, but not zero)

If you do not model this explicitly, you end up with either:

- false negatives (money arrived, player not credited, support tickets spike)

- false positives (player credited, payment later fails, negative balances)

Step-by-step integration blueprint

1) Define your “Deposit Intent” contract

Start by designing a single internal abstraction that works across rails:

payment_intent_idplayer_idamountandcurrencymethod(open_banking)country/jurisdictionproviderandbank_id(optional)return_urlanddevice_contextstatus

Make sure the create intent endpoint is idempotent (same key, same intent) so retries do not create duplicates.

2) Implement an explicit Pay-by-Bank state machine

A practical starting state machine for deposits looks like this:

| State | Meaning | What your system should do |

|---|---|---|

CREATED |

Intent created, no bank session | Show bank selection and “Continue” |

REDIRECTED |

Player sent to bank auth | Start a timer, persist session IDs |

AUTHORIZED |

Bank auth succeeded, payment approved | Move to pending credit checks |

PENDING |

Awaiting provider confirmation or execution | Show deposit tracker, allow support-safe retries |

COMPLETED |

Provider confirms success | Post ledger entries, credit player |

FAILED |

Definitive failure | Show reason category, offer alternative rails |

EXPIRED/CANCELLED |

Player abandons or session expires | Close intent, keep audit trail |

Do not compress this into “success/fail.” The intermediate states are where most conversion and support wins live.

3) Secure the redirect flow (this is where real money leaks)

Most Open Banking flows involve redirects and callback URLs. Your checklist:

- Use OAuth best practices like

stateand (where applicable) PKCE. - Tie callbacks to the original intent using immutable correlation IDs.

- Validate return URLs (no open redirects).

- Require signed webhooks from the provider and verify signatures.

- Store only what you need (data minimization).

If you already run a modern auth stack, align this with your platform’s existing session security patterns.

4) Decide when you credit the player

Operators typically choose one of two policies:

- Credit on provider-confirmed success: simplest and safest.

- Credit optimistically for small amounts: improves time-to-play, but requires tight risk limits and rollback controls.

If you consider optimistic crediting, build it as a policy layer, not a one-off hack. You need:

- max amount thresholds by risk segment

- device/account history gates

- automated clawback handling (and clear player comms)

5) Wire risk controls that fit A2A, not cards

Open Banking can reduce classic card chargebacks, but it introduces other realities (for example, authorized push payment scams, mule accounts, and first-party fraud patterns). A practical, non-theoretical control set includes:

- Name and account-owner checks where available (and permitted)

- Velocity limits (per player, per bank account, per device)

- Device intelligence (new device plus first deposit is higher risk)

- KYC status-aware routing (for example, require KYC completion above thresholds)

- AML monitoring hooks that join deposits with gameplay and withdrawal behavior

Your goal is to reduce fraud without destroying the core benefit of Pay-by-Bank, which is lower friction.

6) Build webhook-first processing (and make it replayable)

Do not rely on the player returning to your site for confirmation. Players close tabs, banks time out, mobile apps kill sessions.

Webhook handling rules:

- Accept and persist every webhook event.

- Make processing idempotent (same event can arrive twice).

- Allow replay from raw events into your ledger posting pipeline.

- Expose an internal “payment timeline” view for ops and support.

This reduces the most expensive failure mode: “Player paid, but we did not credit.”

7) Reconciliation: design it on day 1, not after your first audit

Even if Pay-by-Bank improves approval and reduces disputes, finance still needs a clean daily close.

Implement a three-way match:

- Ledger of record (what you say happened)

- Provider report (what your Open Banking provider says happened)

- Bank settlement (what actually landed)

If you want the operational template for this approach, align your process with the same principles used in modern casino payments reconciliation.

Cashier UX patterns that lift conversion (without creating compliance risk)

Most Pay-by-Bank UX underperforms because it is treated as a tiny button near the bottom of the cashier.

Placement and framing

Good patterns that are still compliant in most contexts:

- Put Pay-by-Bank alongside cards, not hidden under “More methods.”

- Add a short expectation line: “Typically credits in under a minute (bank dependent).”

- Show trust cues: bank logos (approved usage only), security messaging, and clear support paths.

Handle “pending” like a product

“Pending” is not an error. It is a state. Your UI should:

- show a deposit tracker

- avoid encouraging spam retries

- offer a safe fallback method only when you are confident the intent is not going to complete

Make it discoverable for acquisition pages

Pay-by-Bank can be a strong differentiator on landing pages and SEO-focused “deposit methods” pages, especially in markets where players already trust bank payments.

If you are building content funnels around payment options, an external partner like SEO Bridge for affordable SEO support can help structure and optimize those pages so they actually rank and convert.

Testing and rollout: ship it like you would wallet code

A safe rollout looks like:

- Sandbox certification: simulate happy path, timeouts, cancellations, duplicate webhooks.

- Staging with real devices: especially mobile redirects and bank app deep links.

- Internal pilot: staff accounts with strict limits.

- Canary release: small traffic percentage, then ramp.

Track these metrics from the first canary:

| Metric | Why it matters | Segment it by |

|---|---|---|

| Initiation rate | Method attractiveness | country, device, traffic source |

| Completion rate | Real conversion | bank, provider, KYC state |

| Time-to-credit (P50/P95) | Time-to-play and trust | bank, hour of day |

| Support contacts per 1k deposits | Hidden UX failures | reason code |

| Reversal/return rate | Residual risk | bank, player cohort |

Operator checklist: questions to answer before you integrate

Coverage and commercials

- Which countries and banks are actually covered for your target player base?

- What is the pricing model (per transaction, percentage, blended)?

- What are settlement timings and reporting cutoffs?

Technical due diligence

- Is there a sandbox with realistic redirect and webhook behavior?

- Are webhooks signed, versioned, and documented?

- Do you get granular failure reasons (timeout vs rejected vs cancelled)?

Compliance and data

- What data do you receive, store, and for how long?

- How is consent handled and evidenced?

- How do you export audit trails for licensing reviews?

Where Spinlab fits (without rebuilding your stack)

If your current platform makes payments feel like a bolt-on, Open Banking becomes expensive fast.

Spinlab is built as a modular iGaming platform with an API-first approach, integrated payments (crypto and fiat), compliance workflows (KYC/AML), fraud prevention, and real-time analytics. In practice, that architecture is what you want behind Pay-by-Bank: a clean intent model, strong audit trails, and the ability to measure and route deposits like a product.

If you are evaluating how to add Pay-by-Bank alongside cards and crypto in a single cashier, you can explore the platform at spinlab.studio.

Frequently Asked Questions

Is Open Banking only for deposits, or can it be used for withdrawals too? It is primarily used for deposits, but some providers and market setups support bank-based payouts. Whether it is viable depends on jurisdiction, your provider’s capabilities, and how you manage beneficiary validation and reconciliation.

Do Open Banking payments eliminate chargebacks? They typically reduce card-style chargebacks because the flow is bank-authenticated, but you can still see returns, operational disputes, and fraud patterns that require monitoring and controls.

What is the biggest technical mistake casinos make with Pay-by-Bank? Treating it as a synchronous “API payment” instead of an asynchronous rail with webhooks, intermediate states, idempotency, and ledger-safe posting rules.

How long does a solid integration usually take? A minimal integration can be done quickly, but a production-grade implementation (state machine, webhook reliability, reconciliation, dashboards, and canary rollout) usually takes longer. The exact timeline depends on your existing payments architecture and compliance scope.

Do we need account information data for affordability to integrate Pay-by-Bank? Not necessarily. Many operators integrate payment initiation first, then evaluate additional consented data signals later, only where lawful and operationally justified.

Next step: integrate Pay-by-Bank without breaking your ledger or your conversion

If you want Open Banking to perform like a top-tier deposit method, the key is getting the plumbing right: intent lifecycle, webhook reliability, risk gating, and reconciliation.

Spinlab helps operators launch and scale with an all-in-one, modular casino platform (payments, compliance, fraud, analytics, and game aggregation). To see how Pay-by-Bank can fit into a unified cashier alongside fiat and crypto, visit Spinlab and request a walkthrough.