SEPA Instant is becoming a “default expectation” for European players: money moves in seconds, funds are final (push payments), and the deposit experience feels closer to one-click than a traditional bank transfer. For casino operators, that translates into a cleaner fraud profile than cards, faster time-to-play, and fewer “where is my money?” tickets.

But SEPA Instant is also unforgiving operationally. If your reference fields are wrong, your ledger mapping is sloppy, or your limits are naïve, you will feel it immediately in reconciliation breaks, manual reviews, and regulatory questions.

This guide covers what casino teams actually need to ship SEPA Instant successfully: setup decisions, practical limits, and reconciliation patterns that stand up to audit.

What SEPA Instant is (and what it is not)

SEPA Instant (SCT Inst) is a euro credit transfer scheme designed for near real-time account-to-account payments across participating European banks. A few points matter specifically for iGaming:

- It is a push payment: the player authorizes the transfer from their bank, and you receive funds. That generally means no card-style chargebacks, but it also means you cannot “pull” funds or rely on scheme dispute flows like cards.

- Speed changes player behavior: a deposit that credits in seconds lifts conversion, but it also compresses your risk window. Your fraud and AML controls must work in near real time.

- Instant settlement does not eliminate operational complexity: rejects, returns, and investigations still exist, just on different rails and with different message types and timelines.

If you want the scheme-level reference point, the European Payments Council maintains the SCT Inst documentation and rulebooks on its site.

Why casinos adopt SEPA Instant (2026 operator view)

Most operators add SEPA Instant for three business reasons:

1) Higher cashier conversion in euro markets

Players who do not want to use cards (or who repeatedly hit issuer declines) often trust bank rails more. “Pay by bank” options are now table stakes in many European funnels.

2) Lower fraud and dispute exposure than cards

Cards tend to concentrate chargeback and friendly-fraud risk. Push bank transfers shift the risk profile, but you must replace chargeback tooling with stronger identity, beneficiary controls for withdrawals, and better reconciliation evidence.

3) Better withdrawal experience (when supported)

Instant payouts reduce support volume and improve trust. The catch is that instant rails amplify errors: a wrong IBAN or weak beneficiary verification creates immediate player pain.

Setup: how to enable SEPA Instant for an online casino

There are two common paths: integrate via a PSP/payment gateway that offers SEPA Instant, or connect more directly to banking infrastructure. Most casinos choose the first path because it reduces certification, banking relationship complexity, and reporting variance across markets.

Step 1: Decide the integration model (gateway vs direct)

A practical decision framework:

- Gateway/PSP model: faster onboarding, normalized APIs, consolidated reporting, and usually built-in handling for rejects and returns. Trade-off is less control and provider dependency.

- Direct bank connectivity (for mature operators): more control over message flows (ISO 20022), potentially lower unit costs at scale, but higher integration and operational burden.

For many multi-rail casinos, the long-term “clean” architecture is a payment orchestration layer that can route between cards, SEPA Instant, open banking initiation, and crypto, while keeping a single internal ledger.

Step 2: Define your cashier UX (deposit and payout)

SEPA Instant UX wins or loses in the last 20 seconds. The key is to treat it as an intent-based flow with a clear state machine.

In practice:

- Deposit flow: player selects SEPA Instant, sees the exact amount and beneficiary details, then completes authorization in their bank app or bank UI. Your platform listens for confirmation and credits the casino wallet.

- Payout flow: player submits an IBAN, you verify identity and eligibility, then you send an instant credit transfer and show a real-time status.

If your product team already optimized general cashier speed, fold SEPA Instant into the same measurement model: time-to-credit, drop-off at method selection, and failure reason taxonomy.

Step 3: Get the compliance mapping right (KYC, AML, sanctions, RG)

SEPA Instant does not remove compliance obligations, it changes where you enforce them.

Minimum controls most regulators and banking partners expect:

- KYC gating aligned to deposit and withdrawal thresholds, and jurisdiction rules

- AML monitoring on deposit velocity, source-of-funds triggers, and pattern anomalies

- Sanctions screening where required (player identity, and in some models beneficiary data)

- Responsible gambling controls (deposit limits, cooling-off, affordability signals where applicable)

Step 4: Implement bank-grade identifiers and ISO 20022-compatible fields

Reconciliation success is decided before the first payment is sent.

You want a stable internal payment ID that maps to:

- Your cashier “payment_intent_id” (internal)

- The EndToEndId (or equivalent unique reference) you place in the transfer

- The PSP/bank transaction identifiers returned in reporting

If you cannot reliably round-trip a unique reference into bank reporting, your finance team will end up matching on amount plus timestamp, which breaks quickly at scale.

Step 5: Use a go-live checklist that includes finance and support

SEPA Instant launches fail most often because reconciliation and support are treated as “post-launch cleanup.” Make them acceptance criteria.

| Go-live area | What “done” looks like | Owner |

|---|---|---|

| Payment intent state machine | Created, pending, confirmed, rejected, returned, refunded (as applicable) | Engineering |

| Reference fields | End-to-end reference always populated and unique | Engineering |

| Ledger postings | Exactly-once crediting, idempotent webhooks | Engineering |

| Limits | Bank limits, scheme limits, and player limits implemented with clear error messages | Product + Risk |

| Reconciliation | Daily automated match rate target defined, exception queue in place | Finance + Ops |

| Support macros | “Pending/Confirmed/Rejected” explanations and SLAs updated | Support |

Limits: scheme limits, bank limits, and casino limits (and how to layer them)

“Limits” is where casino operators either protect margins or create constant friction. The right approach is layered.

1) Scheme-level limits (ceiling)

The SCT Inst scheme has historically defined a maximum amount per instant transfer (often referenced as EUR 100,000), while allowing participants to apply lower caps. Treat the scheme max as a ceiling, not as what you will actually get per bank.

Because rules and participant behavior evolve, avoid hard-coding assumptions. Make the ceiling configurable.

2) Bank and PSP limits (the real constraint)

In production, the binding constraints are usually:

- Per-transaction caps set by the payer’s bank

- Daily caps and “first-time beneficiary” step-up rules

- PSP risk limits for your merchant account

Your cashier should handle this gracefully. If a player tries a deposit above their bank’s instant cap, show a clear fallback path (smaller amount, different rail, or open banking initiation if available).

3) Operator limits (your risk and RG controls)

Casinos need limits that are not just “max deposit,” but risk-shaped.

Common patterns that work well:

- New player caps for the first 24 to 72 hours

- Progressive trust tiers (higher limits after successful KYC, consistent behavior, and clean payment history)

- Velocity limits (X deposits per hour/day) to catch mule behavior

- Cooling-off triggers when unusual spikes occur (especially if gameplay behavior does not match deposit behavior)

A clean way to implement this is a single “limits service” that returns an allow/deny decision plus a reason code that the cashier can display.

| Limit layer | Example control | Why it matters |

|---|---|---|

| Scheme | Scheme max transfer amount | Prevents impossible requests |

| Bank/PSP | Participant cap, beneficiary step-up | Most common real-world failure |

| Casino (RG) | Player-set deposit limits | Regulatory and player protection |

| Casino (Risk/AML) | Velocity and anomaly limits | Stops fast laundering patterns |

4) Withdrawal limits are different (beneficiary and name checks)

Instant payouts are powerful, but they amplify two failure modes:

- Wrong beneficiary details: money can be misdirected quickly.

- Third-party payouts: payouts to accounts not controlled by the player raise AML risk.

Operationally, withdrawals typically need stricter rules than deposits:

- Verified identity before payout

- Beneficiary ownership checks where required or risk-justified

- Clear rules for “beneficiary change” events (step-up verification, cooling-off)

If you are preparing for evolving EU requirements around payee verification and instant payments, see Spinlab’s overview of PSD3 and PSR and how it impacts iGaming payment flows.

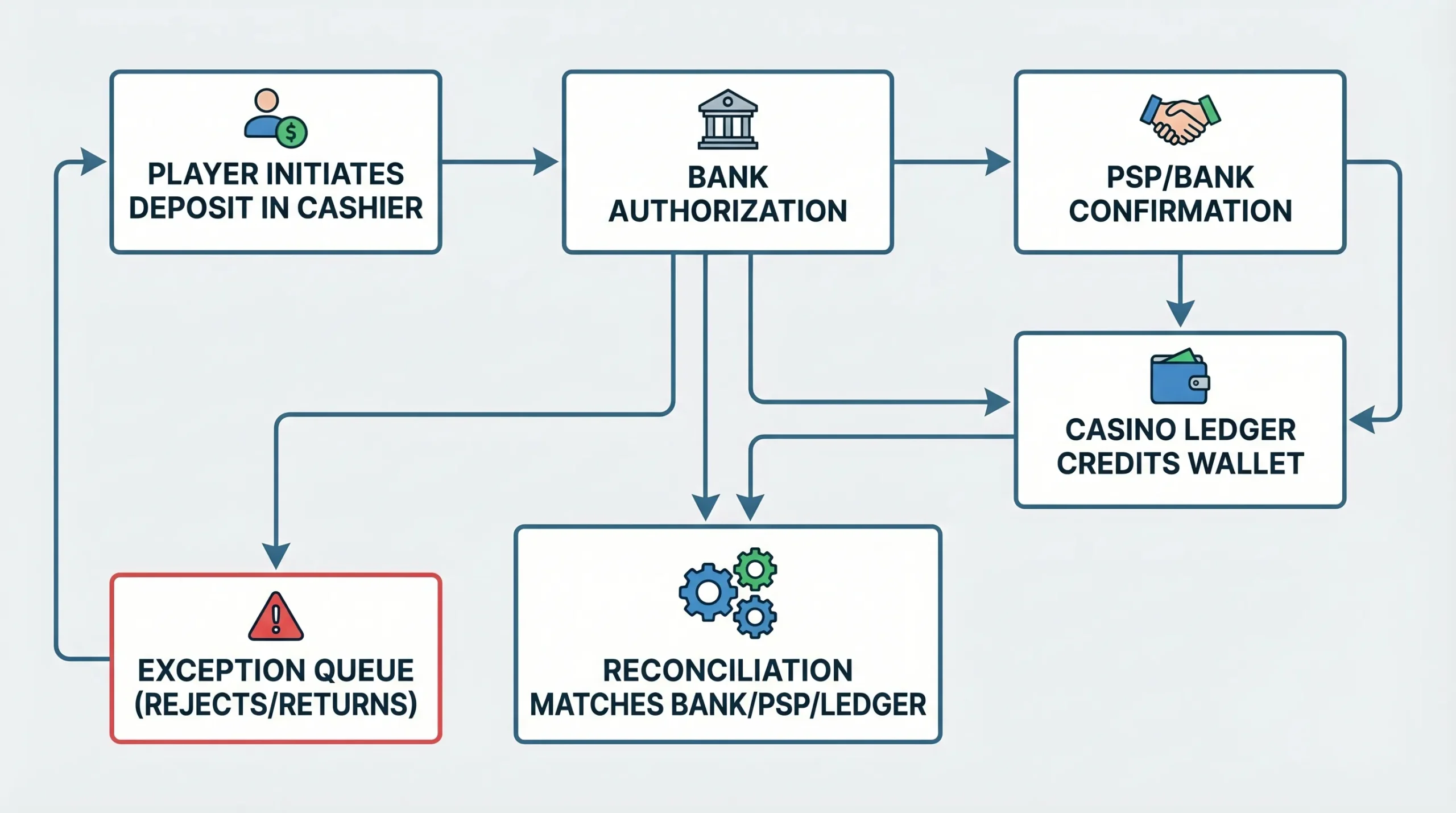

Reconciliation: how to keep SEPA Instant audit-grade

Instant payments increase the speed of money movement, but they also increase the speed at which reconciliation problems become customer problems.

The minimum reconciliation standard: three-way match

For casinos, reconciliation should be designed as a three-way match:

- Casino ledger: your source of truth for player balance movements

- PSP/gateway reports: processor-side transaction outcomes

- Bank statements: actual money movement and settlement

If you want a deeper dive on the operational model and matching rules, Spinlab has a dedicated guide on casino payments reconciliation.

Build an event-driven reconciliation pipeline (not a weekly spreadsheet)

At scale, reconciliation becomes a queueing and exception-management problem.

A practical architecture:

- Ingest bank reporting files/streams (often ISO 20022 camt formats) into a reconciliation store

- Normalize PSP webhooks and reports into the same model

- Match on deterministic keys first (end-to-end reference, internal payment intent ID)

- Fall back to secondary matching only for exceptions (amount, timestamp window, payer IBAN when permissible)

Match keys you should capture from day one

Your match rate depends on whether you capture stable identifiers consistently.

| Data element | Capture from | Used for |

|---|---|---|

| payment_intent_id | Casino cashier | Primary internal join key |

| EndToEndId (or equivalent reference) | Outgoing/incoming transfer | Primary deterministic match |

| PSP transaction ID | PSP | Join to PSP reports |

| Booking date-time | Bank statement | Tie-outs and windowed matching |

| Amount and currency (EUR) | All sources | Validation and secondary matching |

Handle rejects and returns explicitly

Finance teams hate “mystery negatives.” Engineering teams hate “why is the balance wrong?” Solve both by treating negative outcomes as first-class states.

| Outcome type | What it means | Required action |

|---|---|---|

| Reject | Payment never completed | Do not credit wallet, store reason code |

| Return | Funds moved then reversed | Reverse ledger posting, notify player, investigate cause |

| Pending | Authorization in progress | Show pending state, set SLA timer, auto-refresh |

Do not rely on manual interventions as your default. Manual should be the exception queue.

Customer support is part of reconciliation

A noticeable share of SEPA Instant tickets are really “status ambiguity.” You can reduce them by making status legible:

- Show a deposit tracker with timestamps and current state

- Provide “what to do next” guidance for pending states

- Clearly explain when a player should contact their bank vs your support

This is the same productization principle that reduces withdrawal tickets across other rails.

Where SEPA Instant fits in a modern iGaming payments mix

SEPA Instant is rarely the only “bank rail” you will offer. In many EU funnels, operators run:

- Cards for convenience and broad coverage

- SEPA Instant for fast bank transfers where supported

- Open banking initiation for a guided “pay by bank” experience (often riding instant rails in the background)

- Crypto rails for global reach and crypto-native players

The operational challenge is keeping one ledger, one reconciliation model, and one risk layer across all rails.

How Spinlab approaches SEPA Instant-ready operations

Spinlab Studio is an all-in-one, modular iGaming platform designed to help operators build, launch, and scale online casinos with integrated payments, compliance, fraud prevention, and analytics. In practice, SEPA Instant is easiest to operate when it is treated as one rail inside a unified cashier and ledger, not as a bolt-on.

If you are evaluating platforms, prioritize:

- Configurable limits (RG + AML + bank constraints) with clear reason codes

- Idempotent payment processing and ledger postings

- Reconciliation tooling that can do ledger-PSP-bank matching with an exception workflow

- A backoffice that ops teams can actually run daily (Spinlab emphasizes a Shopify-like admin experience)

Spinlab also positions itself as a low-cost option in the white label casino software market. If you are comparing providers, validate total cost of ownership across payments reporting, reconciliation effort, and support load, not just the platform fee.

Frequently Asked Questions

Is SEPA Instant available at every bank in Europe? Not universally. Coverage depends on whether a bank participates in SCT Inst and on local implementation choices (including limits and beneficiary rules).

What is the typical SEPA Instant limit for casino deposits? There is no single universal number. The scheme ceiling has historically been referenced around EUR 100,000, but payer banks and PSPs often apply lower caps. Design your cashier to handle variable limits gracefully.

Do SEPA Instant deposits eliminate chargebacks? They typically avoid card-style chargebacks because they are push credit transfers, but you still need processes for returns, misdirected transfers, and investigations. Your fraud and AML controls remain critical.

What is the biggest reconciliation mistake casinos make with SEPA Instant? Failing to enforce a unique end-to-end reference and failing to map it deterministically to an internal payment intent and ledger posting. That leads to manual matching and balance disputes.

Should SEPA Instant be used for withdrawals too? If your banking and PSP setup supports it, instant payouts can be a major trust and retention lever. Just apply stricter beneficiary controls and step-up checks than you do for deposits.

Next step: make instant payments operationally boring

If you want SEPA Instant to feel magical for players, it has to be boring for ops: clear states, strong identifiers, layered limits, and reconciliation that closes daily.

To see what an integrated approach looks like (payments, KYC/AML, fraud prevention, analytics, and a customizable backoffice), explore the Spinlab platform at spinlab.studio.

If you are relocating an operations or compliance team during an EU market expansion, it can also help to use a dedicated relocation service for housing and home setup. A practical option is stress-free long-term rentals and home services via Movely.