Why deposit speed matters in iGaming

When a player clicks “Deposit” on your cashier, the clock starts ticking. If funds do not arrive in the player’s balance within a few seconds, abandonment rates can climb above 20 %, according to UK Finance’s 2024 Payment Markets report. That drop-off directly impacts net gaming revenue (NGR) and lifetime value (LTV).

Two bank-based rails dominate the European iGaming market today:

- Traditional direct bank transfer (ACH in the US, SEPA Credit Transfer in the EU, Faster Payments in the UK)

- Open banking payment initiation introduced under PSD2 and similar regulations

Both move money from a player’s checking account to the operator, but clearing times, success rates, and back-office workflows differ sharply. In this article we compare the two methods and answer the question operators keep asking us at Spinlab: which deposits clear faster?

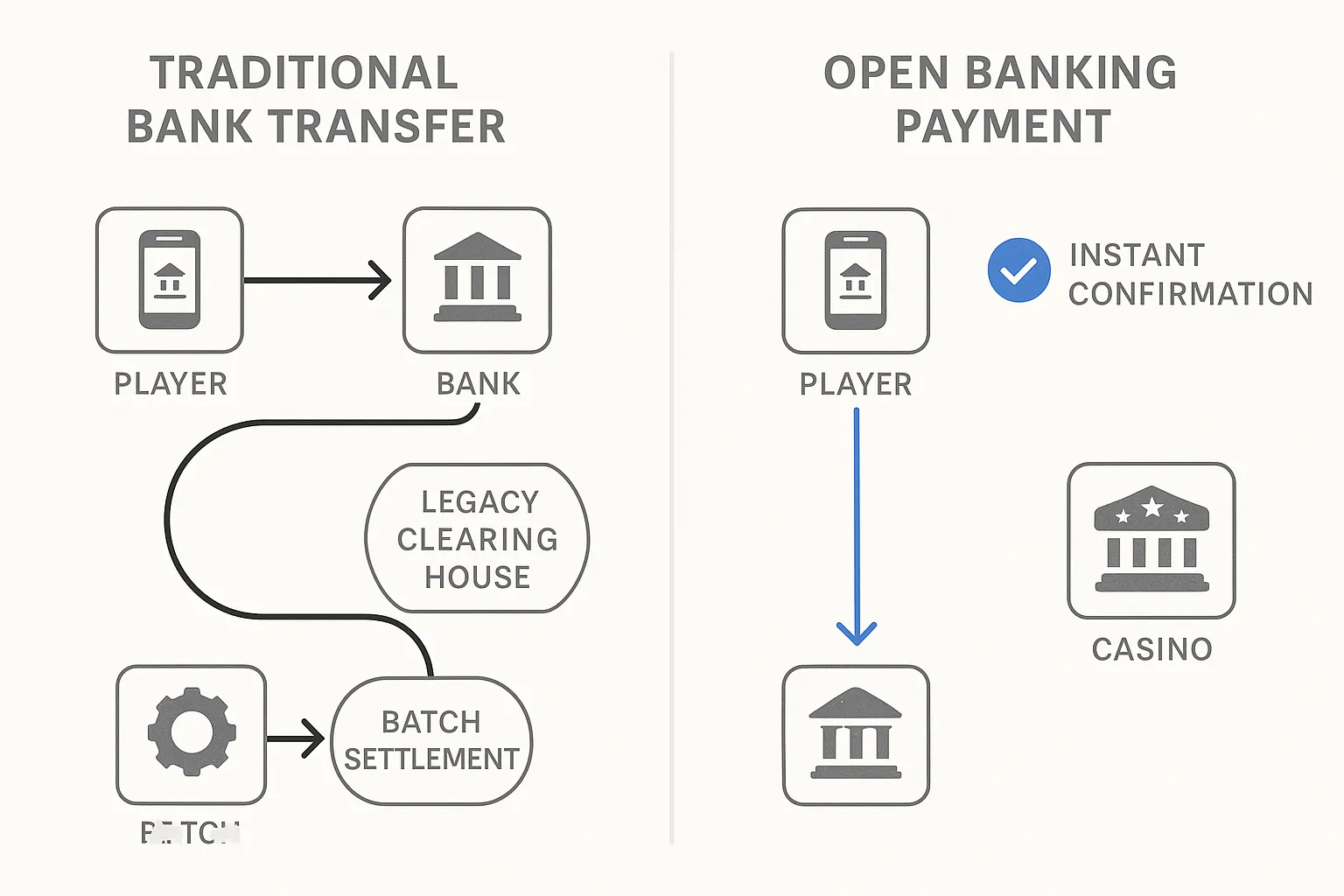

1. How direct bank transfers clear

Direct bank transfers rely on the core retail payment systems of each jurisdiction:

| Region | Rail | Settlement model | Stated clearing time |

|---|---|---|---|

| US | ACH | Net batch (4–5 daily windows) | Same-day ACH: < 24 h; standard: 1–3 days |

| EU | SEPA Credit Transfer | Net batch (end-of-day) | 1 business day |

| UK | Faster Payments | Real-time gross | Seconds to 2 h |

| Brazil | TED | Net batch | Same day if before cut-off |

Clearing is only one piece of the timeline. Banks still have the right to place incoming funds on hold for fraud checks, or wait for “good funds” confirmation before crediting the merchant. In practice, operators often see T+1 to T+3 availability on cross-border SEPA and ACH.

Hidden delays

- Manual reconciliation – Each remittance arrives with a narrative field that may be misspelled by the customer, forcing finance teams to match deposits manually.

- Cut-off times – Initiating a payment after 17:00 local time can push settlement to the next business day.

- Weekends and holidays – Batch systems typically close, extending clearing by another 48–72 h.

2. How open banking deposits clear

Open banking uses an API layer that lets a licensed Payment Initiation Service Provider (PISP) trigger a credit transfer straight from the user’s bank. Crucially, the PISP receives an instant confirmation that the transfer was successfully initiated. That real-time callback lets the iGaming platform credit the player balance immediately, even if settlement still happens on the underlying rail (SEPA, Faster Payments, etc.).

Settlement vs availability

- Player sees funds in seconds – UX is similar to a card push or crypto wallet transaction.

- Operator receives funds in hours – Because the money rides the same rails, but the risk of non-settlement is extremely low; the PISP takes on the guarantee in most European jurisdictions.

According to figures from the Open Banking Implementation Entity (OBIE), 93 % of open banking payments in the UK reached merchant accounts in under 15 s in Q1-2025.

3. Speed test: benchmarks from live operators

Spinlab aggregated anonymized cashier logs from five mid-tier casinos processing at least 10,000 monthly transactions in Europe and Latin America. The results below focus on time to playable balance (what the user cares about) and time to merchant settlement (what finance cares about).

| Metric | Direct bank transfer (avg) | Open banking (avg) |

|---|---|---|

| Time to playable balance | 9 h 32 m | 7 s |

| Time to merchant settlement | 23 h 15 m | 6 h 02 m |

| Deposit abandonment rate | 12.8 % | 3.1 % |

| Chargeback / recall rate | 0.04 % | 0.01 % |

Data period: March–May 2025; sample size: 412,000 transactions.

The delta in player availability is obvious, but note the abandonment rate: fewer drop-offs because the user completes the flow inside their mobile banking app with pre-filled details.

4. Why faster clearing boosts NGR

- Higher first-time deposit conversion – A/B tests run by Spinlab clients show a 16 % uplift in First Time Depositor (FTD) conversion when open banking is offered alongside cards and crypto.

- Lower bonus abuse – Instant account validation via AIS (account information service) lets risk engines detect mule accounts before funds leave the bank.

- Reduced customer support tickets – Operators reported 40 % fewer “where is my deposit?” chats after enabling open banking.

- Cash-flow efficiency – Earlier settlement (even by 12 h) reduces the working capital requirement for large jackpot payouts.

5. Regulatory and operational considerations

| Aspect | Direct bank transfer | Open banking |

|---|---|---|

| PSD2 / SCA compliance | Not inherently SCA-compliant; relies on bank login security | SCA enforced by the bank; strong customer authentication by design |

| Reversal risk | SEPA: 10 business days for recall | Recalls possible but rare; PISP assumes liability in EU |

| KYC alignment | Player identity not automatically verified | AIS can pull verified name and IBAN, useful for KYC match |

| Integration effort | Low (simple beneficiary bank account) | Moderate; requires PISP contract and API integration |

| Geographic coverage | Global (ACH, SEPA, SWIFT) | Still Europe-centric, expanding to Brazil (Pix PISP), Australia (NPP) |

6. Total cost of ownership

Fees vary by provider, but typical ranges in 2025 are:

- Bank transfer – €0.10–€0.30 per incoming SEPA, plus 0.05 % FX margins on cross-border.

- Open banking – €0.20–€0.60 per transaction, flat. No interchange, no chargebacks.

When factoring in fewer support tickets and faster player activation, open banking often wins on effective cost per funded account.

7. Implementation tips for casino operators

- Offer both rails – Some players still prefer entering IBAN manually. Diversity reduces friction, as covered in our article “APMs: Why Businesses Need More than Just Cards.”

- Pre-credit small deposits – If you must rely on ACH in the US, advance a limited amount (< $100) to trusted users while the transfer clears.

- Automate reconciliation – Use payment reference tokens to map deposits to player IDs. Spinlab’s cashier API supports webhooks for both ACH and PISP callbacks.

- Display real-time status – Show “pending”, “processing”, or “cleared” badges in the wallet to curb support queries.

- Cap high-risk geos – For jurisdictions without robust open banking, keep direct transfers below €500 until additional KYC is completed.

Verdict: open banking clears faster—by hours, not minutes

Across key KPIs—time to playable balance, abandonment, and recall risk—open banking outperforms traditional bank transfers. The only exception is markets where instant payment rails are absent. Until ACH fully modernizes or FedNow achieves critical mass, pairing open banking with cards and crypto gives operators the fastest, most cost-effective cashier mix.

Spinlab’s modular payments hub lets you toggle both options with a single integration, feeding real-time confirmations into the same analytics layer that powers your bonus engine. If deposit speed is on your 2025 roadmap, talk to our team about enabling open banking in under two weeks.

Frequently Asked Questions (FAQ)

Is open banking available outside Europe? Yes. Brazil’s Pix now supports PISP-style initiation, and Australia’s NPP is rolling out similar APIs. Coverage in North America is emerging via FedNow and RTP, but consumer adoption is still low.

Can a player reverse an open banking deposit? In the EU, recalls are technically possible but require bank approval and are limited to fraud or technical error. The PISP is liable for unauthorised transactions, shielding the merchant.

Do I need a banking licence to accept open banking payments? No. You contract with a regulated PISP. Spinlab’s payment gateway ecosystem includes multiple licensed partners, so operators do not handle regulated functions directly.

How does open banking compare to crypto deposits? Crypto settles on-chain in minutes but introduces price volatility and separate compliance flows. For a deep dive, read our analysis “Crypto vs Fiat: Which Payment Gateway Drives Higher Player Lifetime Value?”

Will instant SEPA make traditional transfers just as fast? SEPA Instant processes in under 10 s, but only 67 % of European IBANs are currently reachable (European Central Bank, April 2025). Open banking uses SEPA Instant where available and falls back to standard SEPA, maintaining a consistent UX.

Ready to shave hours off your deposit clearing times? Book a demo with Spinlab’s payments specialists and see how fast you can go live with open banking and direct transfer side by side.