Chargebacks are not just a payments problem in iGaming. They are a product problem that hits your approval rates (PSPs tighten rules), your unit economics (fees plus operational labor), and your licensing posture (complaints and dispute ratios are closely watched in many jurisdictions).

This prevention playbook is written for casino product teams who want fewer disputes without “solving” it by adding friction everywhere. The goal is to redesign the deposit to withdrawal journey so that (1) real fraud is blocked, (2) friendly fraud becomes harder to rationalize, and (3) genuine customer dissatisfaction is handled before it becomes a chargeback.

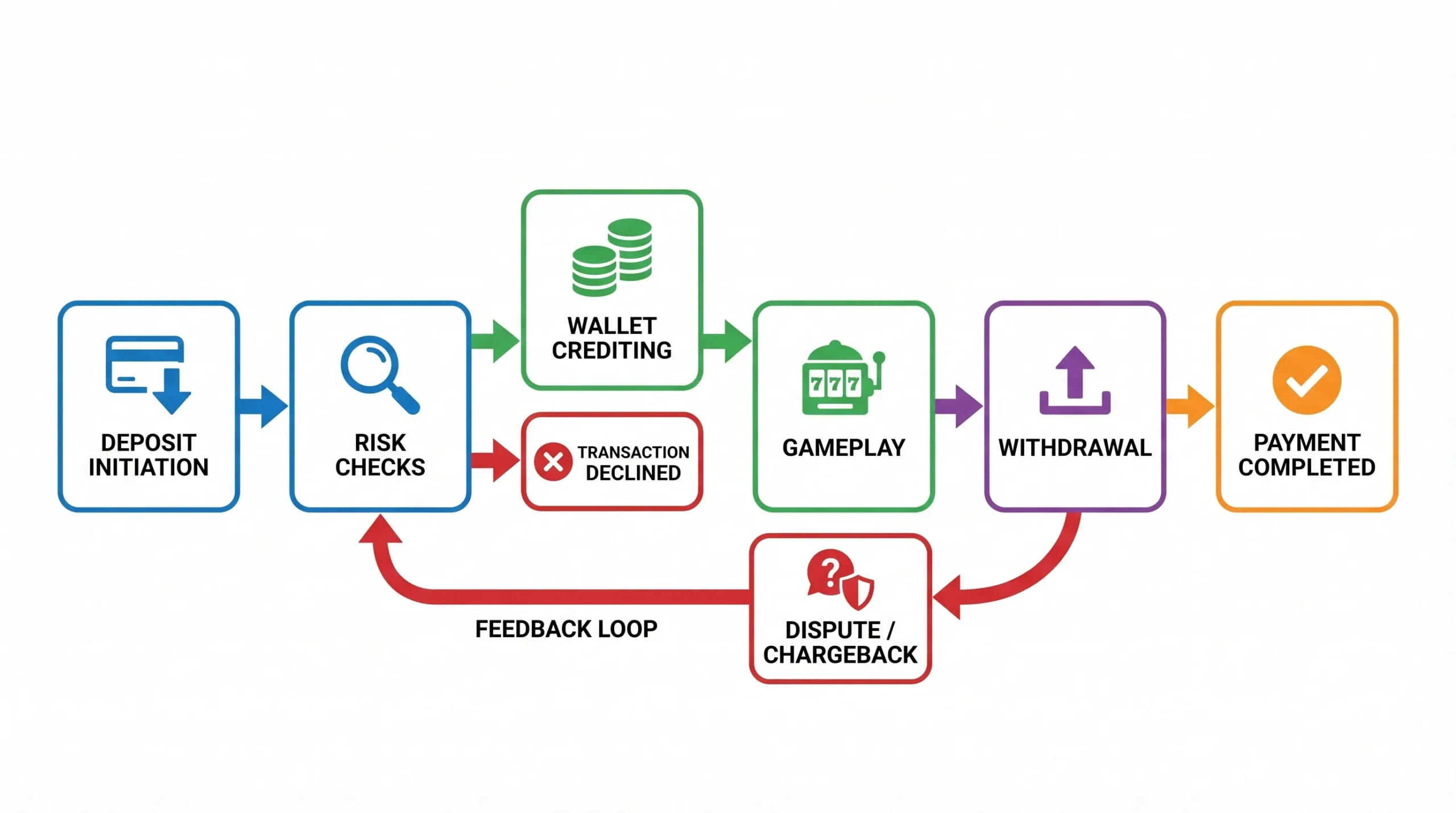

Chargebacks 101 (what product teams need to internalize)

A chargeback is the cardholder’s bank reversing a card transaction after a dispute. In practice, disputes fall into four buckets that require different product fixes:

- Fraud disputes (“I didn’t authorize this”) often correlate with account takeover, card testing, synthetic identities, or weak step-up authentication.

- Service / experience disputes (“I didn’t get what I paid for”) in iGaming often map to confusing terms, unexpected KYC, withdrawal delays, or “I didn’t realize this merchant was the casino.”

- Processing disputes (“duplicate charge,” “wrong amount,” “credit not processed”) are frequently engineering and reconciliation issues.

- Compliance-adjacent disputes (underage play claims, self-exclusion violations, jurisdiction access) can become chargebacks, complaints, and regulator conversations.

The most important mindset shift is this: representment (fighting disputes) is downstream. Prevention is upstream design plus instrumentation. You still want a strong representment process, but you will never scale out of chargebacks if the product keeps generating dispute triggers.

Step 1: Map your casino’s “dispute surface area”

Before you add rules, map where disputes are created. Most casinos discover that 70 to 80 percent of their disputes trace back to a small set of moments.

Here is a practical mapping template you can use in a workshop with Payments, Fraud/Risk, Support, and Compliance:

| Journey moment | What players experience | Common chargeback trigger | Best owner | Prevention lever |

|---|---|---|---|---|

| Registration | Quick signup, weak proof | ATO + stored card abuse | Risk + Identity | Device and bot controls, progressive verification |

| Deposit | “Instant” but with declines | Confusing failure states, retries | Payments + UX | Clear states, idempotency, smart routing |

| First gameplay | Player tests small deposits | Friendly fraud after losses | Product + Risk | Friction calibrated to risk, clear receipts |

| Bonus activation | “Free money” perception | Bonus abuse then dispute | CRM + Risk | Bonus guardrails + enforceable terms |

| Withdrawal | Waiting, silent holds | “Casino won’t pay” complaints | Withdrawals + Support | Withdrawal tracker, proactive comms, clear SLAs |

| KYC moment | Surprise requests | “They asked after I won” | Compliance + UX | Upfront disclosure + progressive KYC |

| Support | Slow, inconsistent outcomes | Player escalates to bank | Support + Product | Faster resolution paths, refund tooling |

If you do nothing else, do this mapping and attach last-90-day dispute examples to each moment. It will stop “generic fraud advice” and focus your team on the specific triggers your product is generating.

Step 2: Build your prevention stack around 4 pillars

Pillar A: Stop real fraud without turning your cashier into a maze

You need layered controls, not one big gate.

Start with the attacks that create chargebacks at scale:

- Card testing and bot deposits: Your first defense is to prevent automated traffic from reaching the deposit form. Spinlab has covered a full containment approach in Preventing Card Testing Attacks on Your Cashier.

- Account takeover (ATO): Treat login as part of payments risk. Step-up at login can prevent downstream disputes.

- High-risk first deposits: Friendly fraud risk is often highest on early deposits, especially when the player loses quickly.

Product patterns that work well in iGaming:

- Risk-based step-up authentication: Use strong customer authentication options (for example, 3DS step-up on risky attempts) while letting low-risk cohorts flow.

- Velocity limits that are human-friendly: Limit deposit attempts per card, per account, per device fingerprint, and per IP range, but communicate it clearly.

- Decline recovery that is not “try again forever”: When retries are unlimited, you create duplicates, player confusion, and bank suspicion.

If you are running payment orchestration, make sure risk controls and routing talk to each other. A common anti-pattern is routing that increases approval rates but quietly increases chargebacks because risk is not gating escalations.

Pillar B: Reduce friendly fraud by removing ambiguity

A surprising amount of “I don’t recognize this” is self-inflicted.

Your product should reduce ambiguity at three points:

- At deposit confirmation: Show a clear receipt (amount, currency, time, payment rail, and casino brand name). If your legal entity and brand differ, explain it.

- In transaction descriptors and support emails: Ensure your descriptor is consistent with your brand and support contact. Mismatches drive bank calls.

- In wallet crediting: If a payment is pending (common for some APMs), do not display it as “taken” without a clear pending state.

A useful mental model is to adopt “inspection-grade” documentation and transparency, similar to industries that reduce disputes by making condition and terms explicit upfront. For example, the premium shipping containers with transparent pricing and inspection steps approach is a good analogy: fewer surprises, fewer arguments later.

Pillar C: Prevent “service disputes” by productizing withdrawals and KYC timing

In iGaming, many disputes are not about the deposit at all. They are about the player’s perception that they cannot get their money out.

Two high-leverage product moves:

- A player-facing withdrawal tracker: Show states (submitted, in review, approved, paid) with timestamps and next steps. This reduces “silent anxiety,” which becomes chargebacks.

- Progressive KYC with upfront disclosure: If you only request KYC after a win, you maximize chargeback probability. You do not need to KYC everyone at registration, but you must be honest about when and why verification will happen.

If you want a deeper withdrawal UX blueprint, see How to Reduce Withdrawals Support Tickets by 40%. Fewer tickets generally means fewer disputes, because players stop escalating to banks.

Pillar D: Eliminate processing errors with “money-safe” engineering

Processing disputes are the most avoidable category, and they are often embarrassing because they are fully within your control.

Focus on:

- Idempotency across payment APIs: One click should never become two charges due to retries or timeouts.

- A ledger-first architecture: Your platform should treat the ledger as the source of truth, not the PSP webhook.

- Three-way reconciliation: Ledger vs PSP vs bank settlement. Small reconciliation gaps turn into “you took my money” disputes.

Even if your ops team “can fix it later,” the player experience happens now. Prevention means fewer exceptions in the first place.

Step 3: Shift volume toward lower-chargeback rails (without killing conversion)

Card chargebacks are structurally part of card payments. The best prevention lever is often a product decision: offer (and intelligently default to) rails that fit your audience and reduce dispute rights.

This does not mean “push everyone to crypto.” It means building a hybrid cashier and routing based on player and payment signals.

| Rail | Chargeback exposure | UX strengths | Key risks to manage | Where it fits best |

|---|---|---|---|---|

| Cards | High | Familiar, fast | Chargebacks, card testing, issuer declines | Broad coverage, established markets |

| Open banking / pay-by-bank | Low | Strong authorization, fewer disputes | Bank coverage variance, UX education | Regions with mature open banking |

| APMs (local wallets, bank transfers) | Medium to low | Local trust, good approval | Asynchronous states, reconciliation | Emerging markets, local-first deposit UX |

| Crypto deposits | Very low (no card chargebacks) | Speed, global reach | AML/KYT, irreversible mistakes, custody | Crypto-native audiences, cross-border |

For orchestration and routing patterns (BIN signals, geo, risk score, provider health), see Casino Payment Orchestration 101.

Step 4: Make chargeback prevention measurable (a product KPI set)

Chargeback work fails when it lives only in Finance or Risk spreadsheets. Product needs a dashboard that connects disputes to funnel events.

Here is a KPI set that is actionable for product teams:

| Metric | What it tells you | Why product should care |

|---|---|---|

| Chargeback rate (count and amount) by deposit cohort | Which cohorts are generating disputes | Lets you target fixes without blanket friction |

| Time from deposit to dispute | Whether issues are “fraud now” or “experience later” | Helps prioritize login/KYC/withdrawal work |

| Refund-before-dispute rate | How often you defuse problems early | Indicates support tooling and policy health |

| Deposit duplicate rate | Retry/idempotency failures | Direct driver of processing disputes |

| Withdrawal “time-to-status” and “time-to-paid” | Whether you create escalation pressure | Correlates with complaints and disputes |

| Step-up auth rate and conversion impact | Cost of friction | Lets you tune risk-based step-ups |

Do not stop at averages. Instrument percentiles (P95 withdrawal time-to-status, P95 support first response) because chargebacks are driven by the worst experiences, not the mean.

Step 5: A prevention playbook you can ship in 30 days

This is a realistic sequence that avoids “big bang” rewrites.

Week 1: Instrumentation and taxonomy

Define a dispute taxonomy you can join back to product events. At minimum, ensure you can link a dispute to:

- Player account and device fingerprint

- Payment attempt ID and idempotency key

- Auth outcome (including any step-up)

- KYC state at time of deposit and at time of withdrawal

- Withdrawal timeline events

- Support interactions and timestamps

If you cannot join disputes to product events, you will argue opinions instead of fixing causes.

Week 2: Fix the biggest self-inflicted errors

Typical high-ROI fixes:

- Eliminate duplicate charges via idempotency and better retry handling

- Replace vague “failed” states with reasoned states (and safe next actions)

- Improve descriptor clarity and receipt messaging

These reduce both chargebacks and support tickets.

Week 3: Add risk-based step-up and bot controls

Add friction only where the risk justifies it. You can start with a simple policy:

- Step-up on first deposits above a threshold

- Step-up when device or IP reputation is poor

- Step-up when the card BIN region mismatches player geo

Then iterate using your fraud-adjusted approval and chargeback cohorts.

Week 4: Productize withdrawals and preempt escalations

Ship:

- Withdrawal tracker

- Proactive messaging on holds, with clear next steps

- Self-serve resolution actions (for example, upload docs, update method, cancel and re-request)

This is where many casinos see the fastest drop in “service disputes” because players stop going straight to their bank.

Where Spinlab fits (without rebuilding your stack)

Spinlab is built as a modular, all-in-one iGaming platform with the components chargeback prevention needs to be a product capability rather than a weekly fire drill:

- Crypto and fiat payment support, plus crypto onramp options, so you can design a hybrid cashier and shift volume toward lower-dispute rails.

- Advanced fraud prevention and KYC/AML compliance primitives to run risk-based step-ups that are measurable and auditable.

- Real-time analytics to connect disputes back to journey events and cohorts.

- Affiliate and bonus engine controls to reduce bonus-driven abuse patterns that often end in disputes.

- A customizable backoffice admin panel and open APIs so ops teams can act fast without engineering bottlenecks.

If your current platform forces you to bolt these together across vendors, prevention becomes slow and inconsistent. With a more unified stack, you can ship the prevention playbook above as product work in sprints.

Frequently Asked Questions

What is the number one cause of casino chargebacks? It depends on your mix, but most casinos see disputes cluster around fraud (ATO/card testing) and withdrawal or KYC frustration. Map your dispute surface area first.

Does adding 3DS eliminate chargebacks? No. It can reduce certain fraud disputes, but it also adds friction. Use risk-based step-up so you do not tax every good player.

How can we reduce chargebacks without lowering deposit conversion? Focus on “clarity fixes” first (receipts, descriptors, better failure states, withdrawal status visibility), then add targeted step-ups only on high-risk cohorts.

Do crypto deposits remove chargeback risk? Crypto transactions are generally irreversible, so classic card chargebacks do not apply. However, you must manage AML/KYT, wallet mistakes, custody controls, and player support expectations.

Should product teams own chargeback prevention, or should Risk own it? Risk should own policy and loss outcomes, but product should own the journey design and instrumentation. Prevention fails when those are separated.

Want a chargeback prevention audit of your cashier and withdrawal flow?

If you want to reduce casino chargebacks without blanket friction, the fastest next step is an audit that links your disputes to specific journey moments and fixes you can ship in 2 to 4 sprints.

Explore Spinlab’s modular iGaming platform at spinlab.studio and book a walkthrough to see how hybrid payments, real-time analytics, fraud prevention, and KYC/AML tools can work together in one stack.