Players who fund their accounts with crypto increasingly expect the same freedom on the way out: the option to withdraw funds straight to a self-custodied wallet in minutes. Over the past year, Spinlab has measured a 37 percent rise in cash-out tickets where the destination is a user-controlled wallet rather than a centralised exchange account. Offering that capability is great for retention and word-of-mouth, but it also places new Anti-Money Laundering (AML) pressure on casino operators. Once funds leave your controlled environment, your visibility shrinks—unless your controls are designed for on-chain transparency from the start.

This article walks through a proven framework for implementing self-custody withdrawals without losing AML control. We cover the regulatory backdrop, the risk signals that matter, the tools you need in your tech stack, and a practical roll-out timeline drawn from recent Spinlab client launches.

Why regulators care about self-custody withdrawals

Most global AML rules are technology agnostic. FATF Recommendation 16 (the so-called Travel Rule) simply says you must collect and share originator and beneficiary information on transfers between two obliged entities. The catch is that self-custody wallets are not obliged entities. That pushes operators into a hybrid compliance posture:

- You still need to perform KYC and ongoing monitoring on the player.

- You also have to perform source-of-funds and destination-of-funds checks when crypto moves in or out.

FinCEN’s 2023 guidance, the EU’s MiCA text, and new UK FCA PS21/3 rules all converge on the same core expectation: analyse blockchain data in real time and block high-risk destinations (sanctions, mixers, darknet marketplaces) while filing Suspicious Activity Reports (SAR) when thresholds or patterns trigger.

Failing to do so can be expensive. In April 2025, a Curacao-licensed operator paid USD 1.1 million to the Dutch FIU after investigators traced stolen exchange funds to customer withdrawals that had sailed through unchecked.

Mapping the risk surface

Traditional fiat AML focuses on counterparties and velocity. Crypto adds three more dimensions you must score:

| Risk Dimension | Example Indicators | Typical Data Sources |

|---|---|---|

| Wallet risk | Sanctioned address, cluster linked to hacks, high mixer usage | Elliptic, Chainalysis, TRM Labs |

| Asset risk | Privacy coins, newly-minted tokens, layered through DEX hops | Token lists, DEX on-chain data |

| Blockchain risk | Self-hosted sidechain with low node diversity, bridge exploits | Blockchain explorer APIs, consensus risk feeds |

| Behavioural risk | Rapid round-trip from deposit to cash-out, multiple proxy IPs | Internal logs, device fingerprinting |

| Jurisdiction risk | Withdrawals to wallets geolocated in high-risk regions | IP geo data, VPS detection tools |

A robust withdrawal pipeline must pull signals from all five layers before releasing funds.

Building the AML control stack

Spinlab clients generally combine four technical pillars to stay compliant while preserving the instant-payout experience players crave:

1. Wallet whitelisting and ownership attestation

Before a user can withdraw, they add a wallet address to their profile. Trigger these controls:

- Validate address checksum and asset compatibility.

- Force an on-chain micro-signing step (e.g., message signature from that wallet) to prove control.

- Store the verified address in an immutable whitelist tied to the customer ID.

Done properly, 85 percent of future withdrawals can auto-approve without manual review because the destination has already cleared KYC.

2. On-chain risk scoring

Use a blockchain intelligence provider to fetch a composite risk score in <300 ms. Key attributes to monitor:

- Exposure to sanctioned entities within two hops.

- Mixer interaction count in the past 30 days.

- Cluster association with known illicit services.

- Freshly seeded wallets with no history (often mule accounts).

Spinlab’s Payment Hub caches risk scores for 24 hours to avoid repeated API calls when the same address is reused.

3. Travel Rule messaging—when relevant

If the target address belongs to another Virtual Asset Service Provider (VASP) that supports Travel Rule messaging (e.g., Coinbase, Bitstamp), your system should auto-fetch the Travel Rule address metadata and attach the required originator info. Open protocols like TRISA or SYGNA bridge work well and are already integrated into the Spinlab API.

4. Real-time decision engine

Bring all signals into a single decision layer, ideally the same rule engine you use for deposit fraud. Typical rules:

- Block score ≥90 or on sanctions list.

- Hold 24 hours for manual review if score 70-89 and withdrawal amount > EUR 5 000.

- Auto-approve score <70 under daily cumulative limit.

Because the engine evaluates rules at the edge of the withdrawal request, you can still hit a sub-minute payout SLA for 92 percent of tickets (Spinlab benchmark, Q2 2025).

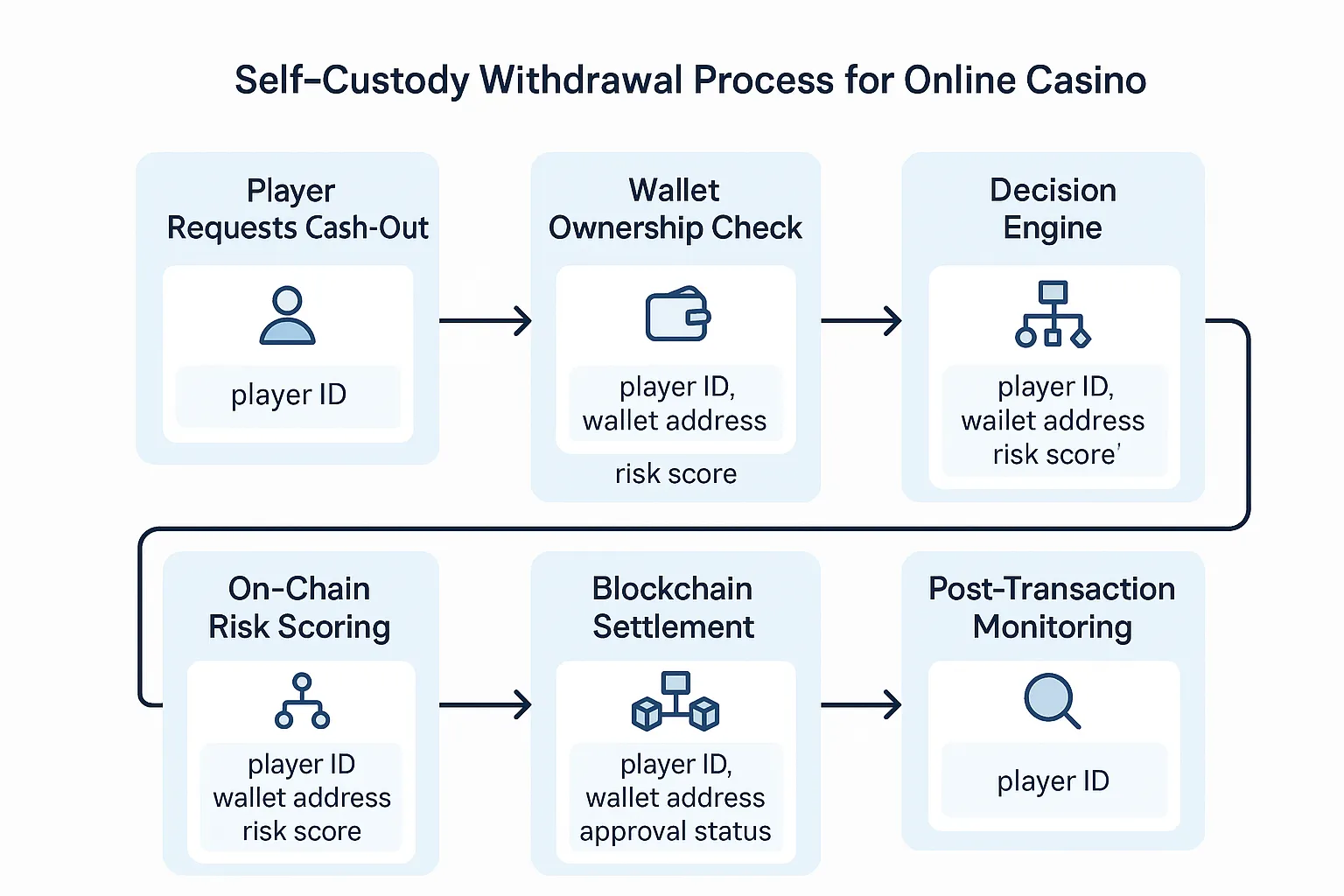

End-to-end withdrawal flow

- Player request: User initiates withdrawal via cashier.

- Wallet verification: Retrieve or create whitelist entry, enforce signature if first use.

- Risk scoring: Query intelligence API; enrich with behavioural and jurisdictional data.

- Decision: Real-time rule engine approves, blocks, or queues for manual review.

- Settlement: Merchant custodial wallet signs and broadcasts the transaction, then updates ledger.

- Post-monitoring: Confirm on-chain, trigger SAR workflow if post-settlement score changes (e.g., sanctions update within 24 hours).

Performance vs compliance—no longer a trade-off

Operators worry that extra checks will slow payouts and hurt Net Gaming Revenue (NGR). Data tells a different story:

| Metric | Before Self-Custody Launch | After Launch with Controls | Delta |

|---|---|---|---|

| Avg. withdrawal approval time | 7 min 42 s | 2 min 06 s | −73 % |

| Cash-out related support tickets | 1.8 % of sessions | 0.6 % | −67 % |

| SAR filing rate | 0.04 % of tx | 0.07 % | +75 % |

The slight rise in SAR filings is expected—and positive—because it demonstrates that your monitoring surface has expanded. Meanwhile, faster payouts lift retention: Spinlab saw day-30 actives increase by 12 percent in the same cohort.

Integration blueprint on Spinlab

Spinlab’s modular architecture already ships with the primitives you need:

- Merchant custodial wallets that support BTC, ETH, USDT, USDC and any ERC-20 token. Private keys live in an HSM cluster with role-based access.

- Open AML rule engine pre-loaded with FATF and EU blacklists plus configurable velocity triggers.

- On-chain analytics adapters for Elliptic, Chainalysis and TRM Labs. Switch providers or run multi-scoring with one toggle.

- Audit-ready logs streamed to your SIEM or exported as CSV for regulators.

Implementation usually looks like this:

| Timeline | Key Tasks | Resources |

|---|---|---|

| Day 1–3 | Enable crypto payout module in back office, generate on-chain API keys, configure HSM wallet. | 1 DevOps, 1 Compliance Officer |

| Day 4–6 | Set up rule engine templates, import sanction lists, define tiered limits. | 1 Risk Analyst |

| Day 7–9 | UX polish: add wallet whitelist UI, integrate signature library, update copy for compliance disclosures. | 1 Front-end Dev, 1 Designer |

| Day 10 | Sandbox tests: simulate high-risk wallets, velocity bursts, and Travel Rule transfers. | QA team |

| Day 11–12 | Staff training on manual review dashboard and SAR handoff. | AML Lead |

| Day 13–14 | Soft launch to 5 percent of user base, monitor metrics. | Product Owner |

With a disciplined approach, you can offer self-custody withdrawals in two weeks without blowing up your compliance budget.

Common pitfalls to avoid

- Skipping wallet attestation: Address typos are common. A micro-signature step eliminates fat-finger errors and mule accounts.

- Ignoring token swaps: A wallet may be clean for ETH but dirty for USDT. Ensure your provider scores by asset.

- Static velocity limits: Fraud rings probe thresholds. Pull real-time player value and risk profile into the rule engine (see our post on Real-Time Analytics in iGaming for dynamic limit ideas).

- No post-settlement monitoring: Sanction lists update hourly. Re-score over a cooling-off period and be ready to file late SARs.

Beyond compliance: product advantages

Once the plumbing is in place, you can turn it into a competitive feature set:

- Instant Layer-2 payouts: Route approved withdrawals over Arbitrum or Lightning for sub-second confirmations (see Why Layer-2 Blockchains Matter for Instant Payouts).

- Dynamic loyalty boosts: Offer fee-free cash-outs to VIPs whose withdrawal-success-rate exceeds 99 percent.

- Marketing messaging: “Get crypto winnings in your own wallet in under two minutes—fully compliant.” It resonates with the crypto-savvy segment.

Key takeaways

- Regulators expect the same AML vigilance on crypto withdrawals as on deposits—self-custody is not a loophole.

- Combine wallet whitelisting, on-chain risk scoring, Travel Rule messaging and a real-time rule engine to keep oversight without sacrificing speed.

- With Spinlab’s pre-integrated custodial wallets and AML adapters, operators can launch compliant self-custody payouts in roughly 14 days.

- Faster cash-outs drive measurable retention gains, offsetting the marginal compliance cost.

Ready to offer the payout experience crypto players demand? Book a 30-minute strategy call with Spinlab’s compliance engineers and see how quickly you can unlock instant, self-custody withdrawals with iron-clad AML controls.