Players decide whether to hit the “Deposit” button in fractions of a second. Yet the moment funds leave their wallet, cognitive alarms go off—especially if they spot an extra 2 % “processing fee.” The way you frame that cost can raise or sink conversion, average deposit size, even lifetime value. Below we unpack the psychology behind surcharges vs no-fee deposits, share live A/B data from iGaming operators, and show how to run your own experiments on Spinlab’s platform.

Why Deposit Pricing Frames Matter

A 2024 meta-analysis in the Journal of Consumer Behaviour found that price framing can shift purchase intent by up to 34 % across digital products. In gambling, that impact is magnified because:

- Deposits happen frequently, so small frictions compound.

- Players often use discretionary income, making them hyper-sensitive to “wasted” spend.

- Competitive switching costs are near zero—another casino is two clicks away.

Most operators silently absorb payment gateway fees. Others pass some or all of the cost to players via a line-item surcharge. Both approaches have merit; what matters is how, when, and to whom you present the fee.

Key Psychological Biases at Play

| Bias | What It Means | Deposit Example | Expected Effect |

|---|---|---|---|

| Pain of Paying | Customers feel real discomfort when parting with money. | Explicit “$1.20 fee” line item. | Lower conversion, higher abandonment. |

| Surcharge Aversion | People dislike extra charges more than higher base prices. | 2 % fee vs 2 % lower bonus. | Up to 20 % drop in intent (Nova & Urban, 2023). |

| Zero-Price Effect | Items framed as “free” create disproportionate joy. | “0 % fee—casino covers all costs.” | Deposit rate spike, larger first deposits. |

| Decoy Effect | Adding a less attractive option nudges users toward the target choice. | Offer $10 fee-free crypto vs $5 card with $0.40 fee. | Increases share of lower-cost rails. |

| Reciprocity | Players respond positively when the house absorbs a cost. | “We pay your gas fees today.” | Boosts loyalty and NPS. |

Understanding these biases lets you design cashier experiences that maximize net gaming revenue (NGR) even when you opt to surcharge.

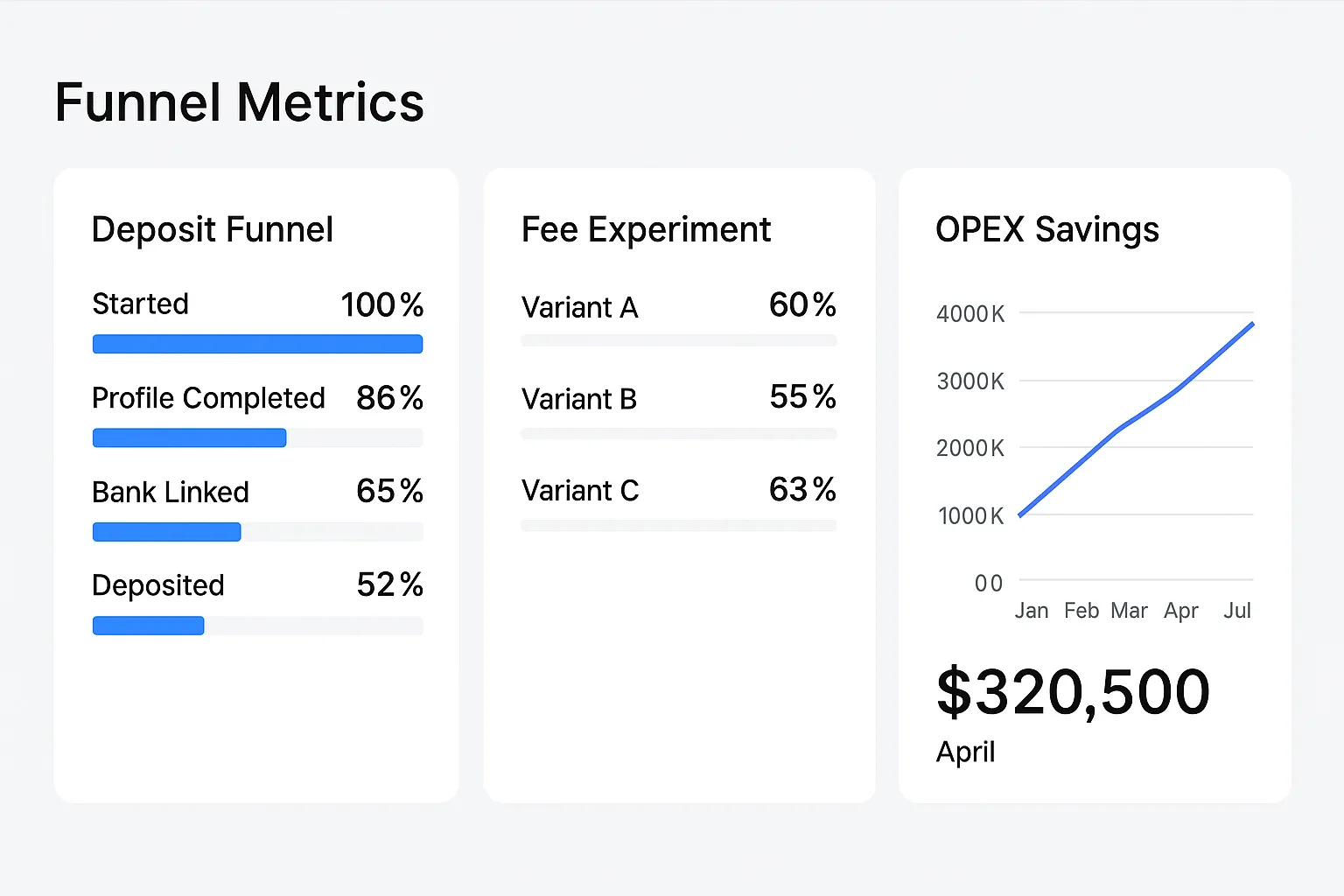

Experiment 1: Flat Surcharge vs No-Fee (Control)

Anonymized data from three mid-tier EU casinos on Spinlab (Q2-2025):

| Metric | No-Fee (Control) | 2 % Surcharge | Δ |

|---|---|---|---|

| Deposit Conversion | 78.4 % | 71.3 % | –7.1 pp |

| Avg. Deposit Size | €46.10 | €50.90 | +10.4 % |

| Gateway Cost / Deposit | €1.02 | €0.32 (player pays) | –68 % |

| NGR/Player/Month | €112.30 | €109.40 | –2.6 % |

Takeaway: surcharging improved gross margin per transaction, but lower conversion shaved nearly all gains. However, deposit size rose, hinting at a self-selection effect: only committed players pushed through.

Experiment 2: Conditional Free Rail

Goal: steer deposits to a cheaper payment method without cutting revenue.

Setup

- Rail A: Card, 2.4 % fee (operator cost).

- Rail B: Open Banking, €0.05 flat cost.

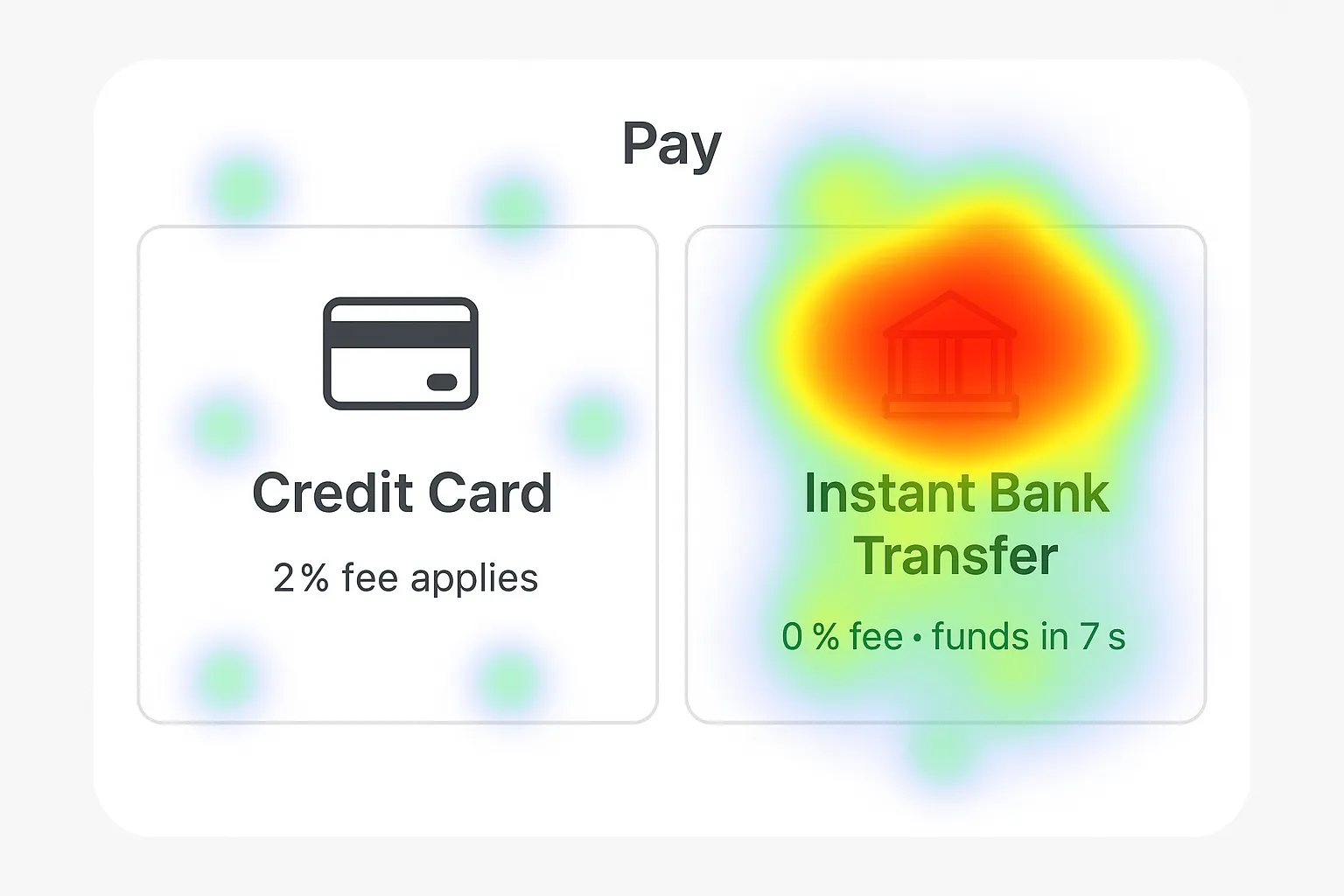

- UI: “Instant Bank Transfer — 0 % fee” badge, card displayed second.

Results (4-week test, 42k sessions):

| Metric | Pre-Test | Post-Test |

|---|---|---|

| Share of Open-Banking Deposits | 19 % | 47 % |

| Overall Deposit Conversion | +3.2 pp | |

| Average Time-to-Balance | –12 s | |

| Payment OPEX | –41 % |

Framing the cheaper rail as free and faster moved nearly half of deposits to a cost-efficient channel—mirroring findings in our article on open banking (https://spinlab.studio/direct-bank-transfer-vs-open-banking-which-deposits-clear-faster/).

Four Tested Messaging Variations That Shift Behavior

-

Bundled Bonus Offset

“Deposit €50, get €50 + we cover all fees.” Players anchor on the headline bonus; fee coverage feels like extra generosity. -

Time Savings First, Fee Second

“Play in 10 seconds • 0 % fee” proved more persuasive than fee-first phrasing. -

Gamified Fee Rebate

Refund the surcharge as loyalty points unlockable after wagering €X. Converts cost into an engagement driver. -

Limited-Time “House Pays Fees” Banner

Scarcity bias (24-hour window) triggered a 14 % lift in first-time deposits in LATAM markets.

When Surcharging Makes Economic Sense

- Micro-Deposits (<$10): Fees eat a larger share of GGR; passing on cost preserves margin.

- High-Risk Markets: Chargebacks drive payment OPEX; shifting to surcharge deters fraud rings.

- Premium Payment Features: Same-day card payouts or fiat-to-crypto swaps justify a usage fee.

Spinlab clients often apply rule-based surcharging—e.g., only on card transactions under €20 or on weekend withdrawals—using our fee engine.

Regulatory Watch-Outs

- EU PSD2 Anti-Surcharging Clause: Bans fees on consumer card payments within EEA. Crypto and A2A payments are unaffected.

- US State Variance: Some states cap card surcharges at 3 %, others mandate disclosure font size.

- LATAM: Brazil allows surcharges but requires clear, upfront disclosure (Art. 39, Consumer Code).

- Responsible Gambling: Advertising “free deposits” must exclude wagering requirements in the same visual field to avoid misleading claims.

Always run fee strategies past legal counsel and ensure cashier copy meets local rules. Our compliance module can geo-target fee disclosure text.

How to Run Your Own Pricing Tests on Spinlab

-

Define Segments

Use Spinlab’s real-time segmentation to target new vs VIP cohorts or specific jurisdictions. -

Configure Dynamic Fees

In Backoffice › Payments › Fee Rules, set conditions (rail, currency, amount range). No code needed. -

A/B or Multi-Armed Bandit

Toggle “Send to Experiments API” and allocate traffic split. Results stream live into the analytics dashboard (https://spinlab.studio/real-time-analytics-in-igaming-turning-live-data-into-bigger-profits/). -

Monitor Key KPIs

- Deposit Conversion

- Average Deposit Value

- Payment OPEX / GGR

- Player LTV (see crypto vs fiat study: https://spinlab.studio/crypto-vs-fiat-which-payment-gateway-drives-higher-player-lifetime-value/)

-

Iterate Weekly

Most fee-framing effects surface within 5,000-10,000 cashier sessions. Kill losers fast; scale winners.

Bottom Line

Whether you absorb gateway costs or pass them on, presentation is everything. Smart framing can nudge players toward cheaper rails, protect margins, and even boost loyalty. The only way to know what works for your audience is disciplined experimentation.

Spinlab’s modular cashier, fee engine, and streaming analytics let you launch pricing psychology tests in hours—not weeks—while staying compliant across markets.

Ready to see how fee framing could lift your NGR? Book a 20-minute demo today and run your first surcharge vs no-fee experiment this week.