If you accept EU players or plan to expand into European markets, the next wave of payment rules will reshape your cashier, authentication, bank-transfer flows, and dispute handling. Here is a practical, plain‑English brief on what PSD3 and the new Payment Services Regulation (PSR) change, why it matters for iGaming payments, and what to implement before the rules start to bite.

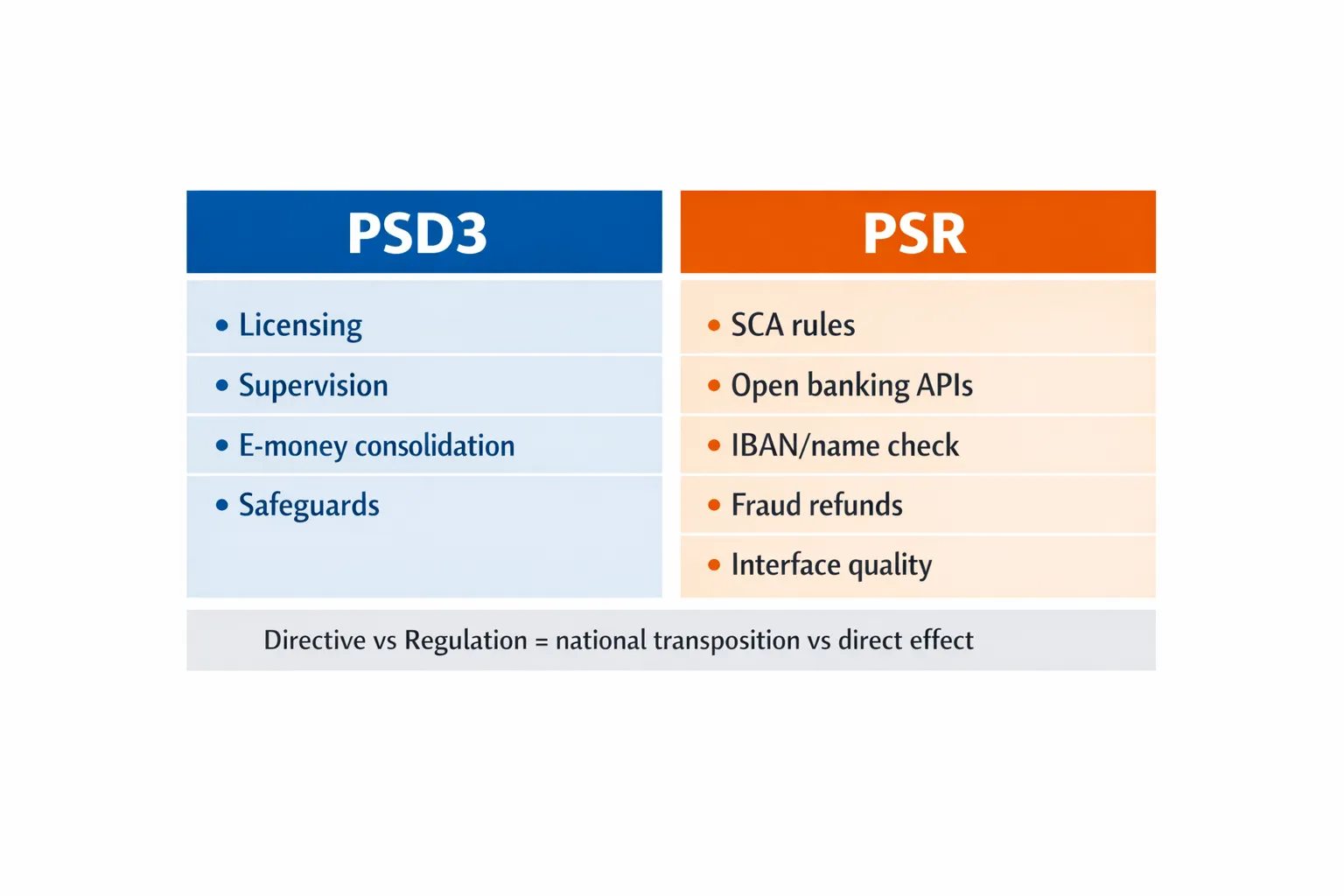

PSD3 vs PSR at a glance

- PSD3 is a Directive. It primarily updates licensing, supervision, and market entry rules for payment institutions and e‑money. Directives require each EU country to transpose them into national law.

- PSR is a Regulation. It sets harmonized conduct‑of‑business rules that apply directly across the EU without national transposition, which means less fragmentation and more consistent enforcement.

- Together, they modernize PSD2, tighten anti‑fraud protections, and improve open banking rails that power pay‑by‑bank deposits and instant payouts.

Current status and timing: the European Commission tabled the proposals in 2023. Final texts and application dates will follow the EU legislative process. Operators should plan for staged application windows after entry into force, typically on the order of 18 to 24 months for major changes. See the Commission’s overview for background and updates: European Commission: Payment services framework (PSD2, PSD3 and PSR).

Note on terminology: PSR in this article means the EU Payment Services Regulation. It is unrelated to the UK’s Payment Systems Regulator, which uses the same acronym.

The changes likely to affect iGaming cashiers most

1) Strong Customer Authentication, modernized for today’s devices

PSR refreshes Strong Customer Authentication (SCA) and clarifies acceptable factors and journeys. Expect continued emphasis on phishing‑resistant methods that bind authentication to the device and transaction context. Passkeys and on‑device biometrics will sit on stronger footing than SMS OTP, and dynamic linking remains central for remote payments. The EBA’s existing SCA guidance stays relevant as a baseline while PSR updates details for newer tech. Reference: EBA Guidelines on SCA and secure communication.

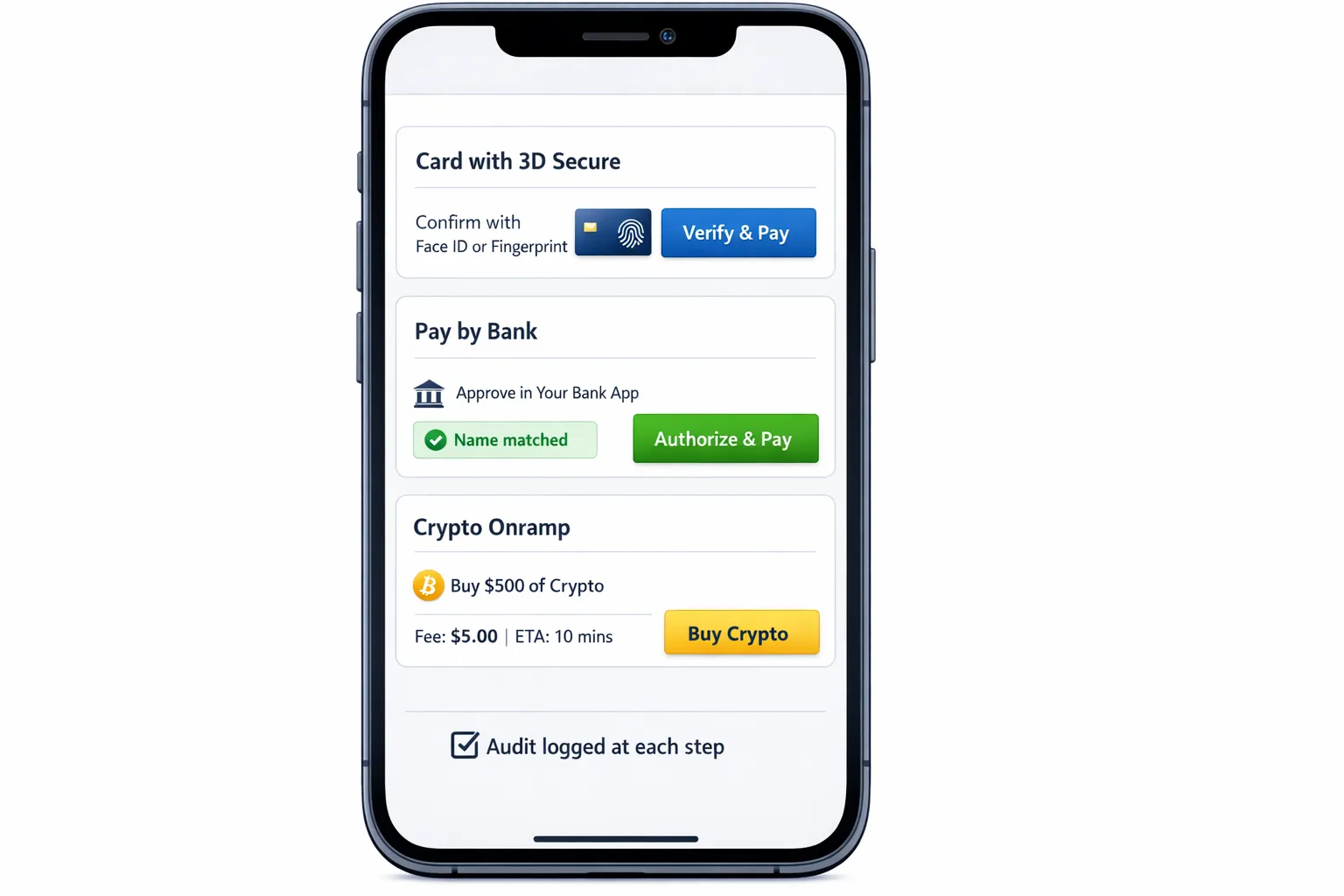

What it means for casinos: 3‑D Secure will not disappear for cards, but risk‑based and possession‑bound flows will be favored. If you still lean on SMS for step‑up, plan to adopt passkeys or app‑based approvals to reduce abandonment and fraud. For account‑to‑account (A2A) pay‑by‑bank flows, authentication should increasingly feel like one‑tap biometric approvals inside banking apps.

Related deep‑dive: SMS 2FA vs Passkeys: Security Trade‑Offs for Casino Logins.

2) Open banking gets more reliable and less frictiony

Under PSR, dedicated bank APIs remain mandatory and obstacle‑free access is reinforced. Expect tighter uptime and performance expectations, better conformance testing, and standard permission dashboards so customers can see and revoke third‑party access without the clunky 90‑day re‑authentication loops that caused churn under PSD2. Payment initiation service providers should see fewer broken journeys and a more uniform experience across banks.

What it means for casinos: A2A deposits should become more consistent in approval rates and time‑to‑credit. This strengthens the business case to promote pay‑by‑bank as a primary rail alongside cards. If you currently depend on manual reference transfers or batch reconciliation, you will be competing with operators offering near‑instant, app‑approved deposits tied into a unified ledger.

Recommended primers:

- Direct Bank Transfer vs Open Banking: Which Deposits Clear Faster?

- 7 Ways Open Banking Will Transform Casino Deposits

3) IBAN/name check and tougher action on impersonation fraud

PSR proposes an EU‑wide IBAN and payee‑name matching service for credit transfers, similar in spirit to Confirmation of Payee. Payers will be warned when the name does not match the IBAN, and PSPs must have stronger controls against impersonation and authorized push payment scams. Consumer refund rights are strengthened in specific impersonation scenarios, which pushes more liability onto the payment chain if warnings or controls are missing.

What it means for casinos: You will need to ensure your beneficiary naming is consistent with what players see at payment initiation. Using PSP pooled accounts with a generic beneficiary name can drive drop‑offs when the name check flags a mismatch. Work with your PSP or open banking aggregator to present the correct descriptor and to log warnings. Build server‑side evidence for dispute handling and refunds. For a policy perspective on IBAN issues, see the European Payments Council’s note: IBAN discrimination remains prohibited.

4) Instant payouts will be the default expectation

Separate from PSD3/PSR but highly related, the EU’s Instant Payments Regulation requires euro‑area banks to send and receive SEPA Instant Credit Transfers with pricing no higher than standard transfers and with extra checks in place. As banks finish their rollouts, same‑day or sub‑minute withdrawals become a baseline. See: Council of the EU adopts instant payments rules.

What it means for casinos: Combine PSR’s API reliability with instant rails and you can offer card, A2A, and wallet payouts that clear quickly and predictably. This improves trust, reduces support tickets, and lifts re‑deposit velocity when handled responsibly.

5) Licensing consolidation and vendor due diligence

PSD3 merges parts of the e‑money rulebook into the payment‑services perimeter and tightens authorization and safeguarding requirements. If your EU PSP relies on an e‑money license or passporting strategy, expect paperwork and supervisory changes. Merchants are not directly licensed under PSD3, but your risk and compliance teams should refresh vendor oversight playbooks and contractual warranties.

What it means for casinos: Strengthen third‑party risk management (licensing status, safeguarding, operational resilience, data protection, fraud sharing). Your cashier depends on their compliance.

How these rules change deposits, withdrawals, and disputes

- Deposits via card: Expect more banks to support friction‑light possession factors and merchant whitelisting for returning players within SCA rules. Your job is to reduce false step‑ups, pre‑warm 3‑DS data, and route intelligently.

- Deposits via A2A: With stronger APIs and IBAN/name checks, players will see clearer payee names and faster approvals. Present total costs up front and keep descriptor consistency to avoid “mismatch” warnings.

- Withdrawals: Instant SEPA and improved push‑to‑card rails enable near‑real‑time payouts. You still need AML velocity checks, transaction risk analysis, and audit trails.

- Disputes and fraud: Impersonation and social‑engineering scams are a priority. You must demonstrate proper warnings, controls, and logs. Build playbooks for refund handling and reconciliation.

Operator checklist mapped to PSD3/PSR changes

| Area | What changes under PSD3/PSR | Operator actions and owner |

|---|---|---|

| SCA rules and UX | Clearer acceptance of device‑bound, phishing‑resistant SCA, dynamic linking reinforced | Replace SMS OTP with passkeys or app approvals (Payments + Engineering). Tune 3‑DS data enrichment. A/B test abandonment and approval lift. |

| Open banking APIs | Dedicated APIs with fewer obstacles and better permission UX | Integrate at least one EU open banking aggregator into a unified payment hub (Engineering). Add health checks, failover, and reconciliation hooks. |

| IBAN/name check | Mandatory name matching with payer warnings | Align beneficiary naming with what the player sees (Payments). Update descriptors, QA test across top EU banks, log warnings server‑side. |

| Impersonation fraud and refunds | Stronger controls and refund rights in specific scenarios | Add scam warnings, ML signals for mule risk, cool‑down windows (Risk). Update T&Cs and dispute runbooks (Legal). |

| Vendor licensing | E‑money and PI perimeter updated, stricter supervision | Refresh vendor due diligence and SLAs, request updated licenses and safeguarding attestations (Compliance). |

| Instant payments | Faster euro payouts at a capped fee versus standard transfers | Offer instant withdrawals with risk‑based limits and messaging, measure CSAT and re‑deposit velocity (Payments). |

A 90‑day implementation blueprint

Phase 1, weeks 1 to 3, assess and prioritize

- Map your EU traffic and payment mix. Identify top issuing banks and countries.

- Baseline key KPIs: SCA failure rate by issuer, time‑to‑credit by rail, A2A abandonment, dispute ratios, refund cycle time.

- Run a cashier copy and descriptor audit. Ensure beneficiary names match brand expectations and legal entities.

- Vendor review: licenses, incident history, uptime SLAs, fallback processes, fraud data sharing.

Phase 2, weeks 4 to 8, build and test

- Add a passkey sign‑in and step‑up path, then gradually reduce SMS OTP exposure for low‑risk segments.

- Integrate an EU open banking aggregator into a unified payment hub, including health checks and ledger mapping.

- Implement IBAN/name check telemetry with QA across the top 20 EU issuers for your markets. Fix descriptor mismatches.

- Add contextual scam warnings and cool‑downs for high‑risk payout scenarios. Update in‑app copy and educate support.

Phase 3, weeks 9 to 12, launch and monitor

- A/B test card vs A2A deposit prominence by market. Track approval, abandonment, and first‑time‑deposit conversion.

- Turn on instant euro payouts for verified segments. Measure CSAT, ticket volume, and re‑deposit behavior.

- Update T&Cs, privacy notices, and dispute playbooks. Train agents on new refund pathways.

- Ship compliance telemetry dashboards that tie every authentication, warning, and decision to immutable logs.

Architecture notes for payments leads

- Use a modular payment hub that abstracts PSPs and open banking aggregators behind one API, ledger, and reconciliation layer. This gives you routing freedom as PSR reshapes reliability and costs.

- Treat SCA as a product. Implement device binding, passkeys, and 3‑DS data enrichment as configurable modules you can A/B test without code freezes.

- Make IBAN/name check a first‑class signal. Store the bank’s returned comparison result and show the exact name players will see before they approve.

- Keep crypto onramps in the same cashier, with clear fee and ETA disclosure, and the same KYC and AML controls. Many EU players prefer stablecoins, while fiat remains dominant in regulated markets. See our perspective on optimizing hybrid cashiers: Crypto vs Fiat: Which Payment Gateway Drives Higher Player Lifetime Value?.

Governance and evidence you will need in audits and disputes

- Immutable audit trails for every authentication step, warning, and approval decision.

- A catalog of supported SCA factors and where you use them, with rationale by segment or market.

- IBAN/name check logs for A2A payments, including the presented payee name and the bank’s similarity result.

- Vendor due‑diligence files with license copies, safeguarding statements, and incident SLAs.

- Fraud and mule‑account controls, including thresholds, cool‑downs, and manual‑review outcomes.

How Spinlab helps operators prepare

Spinlab’s modular iGaming platform was built for hybrid payments at scale, with crypto and fiat rails, KYC and AML compliance, fraud prevention, real‑time analytics, and open API integration. Operators use our Payment Hub to add pay‑by‑bank next to cards, wire in crypto onramps, and route payouts intelligently, while our backoffice and dashboards provide audit‑ready visibility across SCA, fraud, and reconciliation. If you are aiming for a Shopify‑like experience to launch or modernize a white label casino platform, Spinlab is designed for fast onboarding and predictable operations.

We do not replace your counsel. This article is general information, not legal advice. For regulatory interpretations rely on your legal team and official EU sources, including the Commission’s PSD3/PSR page linked above.

Frequently Asked Questions

What is the single biggest change I should plan for first? Prioritize SCA modernization and a bank‑A2A rail with proper IBAN/name presentation. Together they cut abandonment and fraud while aligning with PSR’s direction.

Will PSD3 or PSR force me to accept every EU IBAN for deposits? IBAN discrimination is already prohibited in the SEPA area. You still have AML and responsible‑gaming obligations, but you cannot refuse an otherwise valid EU IBAN for unjustified reasons.

Do I have to pay for refunds in impersonation fraud cases? PSR strengthens consumer protection in specific impersonation scenarios. Liability can depend on whether proper warnings and controls were in place. Keep detailed logs and consult counsel for case handling.

Does this kill SMS OTP? No, but the trend favors device‑bound, phishing‑resistant factors like passkeys and app approvals. Expect better conversion and fewer takeovers when you move away from SMS, especially for high‑value players.

When will these rules apply? The Regulation will have direct effect after it enters into force, usually with transition periods. The Directive must be transposed by Member States. Plan your roadmap now so you are not rushing later.

How do instant payouts fit into all this? Instant euro rails are becoming mandatory across the EU. Combine them with PSR‑grade authentication and fraud controls to deliver faster, safer withdrawals that improve trust and retention.

Next step

Want a PSD3/PSR readiness audit of your cashier and payout stack, with concrete A/B tests and a 90‑day playbook? Book a discovery call at spinlab.studio. We will review your payment gateway mix, open banking coverage, SCA flows, crypto onramp placement, beneficiary naming, and compliance telemetry, then outline the fastest path to an EU‑ready, conversion‑optimized iGaming payments experience.