Most compliance failures in iGaming do not happen because a team ignores regulation. They happen because teams treat KYC and AML as the same thing, bolt them on late, then drown in manual reviews when volume spikes or crypto rails get added.

KYC and AML are tightly connected, but they solve different problems. Understanding the difference is the fastest way to design workflows that (1) pass audits, (2) reduce fraud and chargebacks, and (3) keep your onboarding and cashier conversion healthy.

KYC vs AML in iGaming: the simplest (accurate) distinction

KYC (Know Your Customer) answers: “Who is this player, and are they allowed to play here?”

It is primarily an identity and eligibility process. In iGaming it typically covers identity verification, age checks, jurisdiction checks, and in many markets, source-of-funds or affordability-related evidence when risk triggers.

AML (Anti-Money Laundering) answers: “Given what this player is doing, does it look like illicit finance, sanctions evasion, or laundering?”

It is primarily a behavior and funds-flow process. AML is ongoing, even after a player is verified.

Why the confusion is so common:

- KYC is often a gating step that operators feel immediately (conversion impact).

- AML is often a monitoring and casework step that operators feel later (ops load, audits, fines).

- Both reuse overlapping tooling (screening, risk scoring, case management, audit trails).

If you want a north star, follow the risk-based logic advocated by global standard setters like the FATF Recommendations: apply controls proportional to risk, and be able to evidence your decisions.

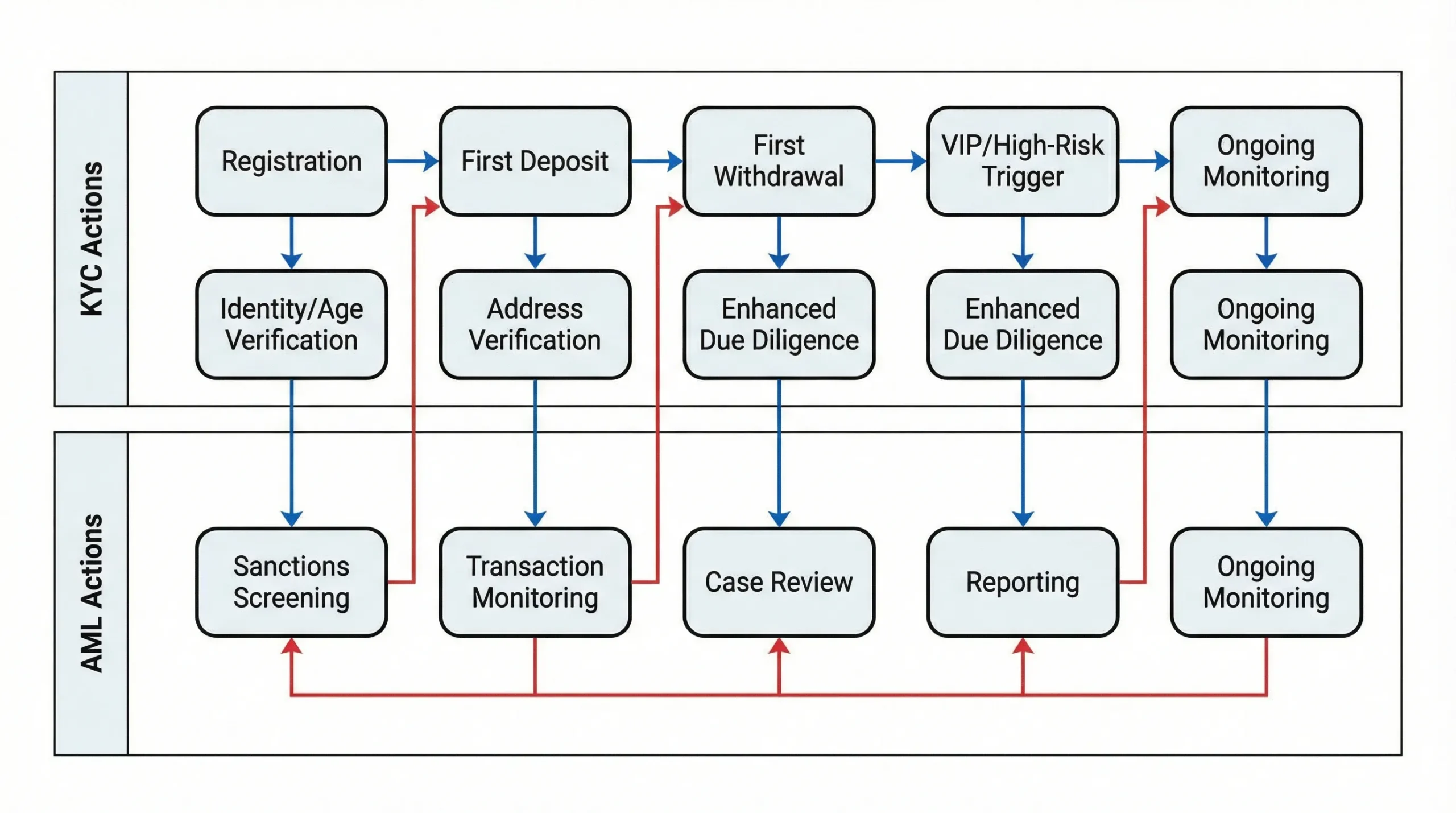

Where KYC ends and AML begins (in the player lifecycle)

In a modern online casino, KYC and AML show up at multiple checkpoints, not just “verify ID at registration.”

Here is a practical mapping that compliance, product, and risk teams can align on:

| Journey point | KYC objective | AML objective | Typical decision outcome |

|---|---|---|---|

| Account creation | Establish baseline identity and eligibility (age, geo, uniqueness) | Initial sanctions/PEP screening and risk seeding | Allow, block, or step-up verification |

| First deposit | Confirm identity if required by jurisdiction or risk | Detect stolen payment instruments, mule behavior, structuring | Allow, hold, require more info, route to review |

| Gameplay and bonuses | Maintain a consistent identity across sessions/devices | Detect bonus abuse linked to laundering patterns (high turnover, low entertainment) | Continue, limit, freeze bonus, investigate |

| First withdrawal | Confirm “rightful owner” before funds exit | Detect layering, rapid in-out, third-party funding | Approve, hold pending EDD, file report if needed |

| Scaling to VIP | Enhanced checks for high-risk/value players | Ongoing monitoring, source-of-funds triggers, velocity thresholds | EDD, limits, enhanced monitoring, offboarding |

The key takeaway: KYC is not one moment, and AML is not just a rules engine. Both are workflows.

A modern KYC workflow for iGaming (designed to protect UX)

A high-performing KYC flow is progressive: you collect the minimum information needed early, then step up verification only when regulation or risk requires it.

KYC workflow stages (what “good” looks like)

Stage 1: Capture and normalize identity data

This is about data quality and future matching. Even before document checks, you want consistent fields, validation, and deduplication.

Stage 2: Verify identity (IDV) and liveness

Most operators use a vendor for document authenticity checks and selfie/liveness. In iGaming, mobile capture quality and retry UX often matter as much as raw verification accuracy.

Stage 3: Eligibility checks

This is where you enforce age and jurisdictional availability, and align with your geo-blocking and payment acceptance policies.

Stage 4: Enhanced due diligence (EDD) when triggered

EDD is not for everyone. Common triggers include high velocity deposits, unusually large withdrawals, certain geos, payment-method risk, or adverse media signals.

KYC tools you typically need (category-level)

- ID verification (document + selfie): authenticity, liveness, anti-spoofing.

- Sanctions/PEP screening (often shared with AML): name and date-of-birth matching with tuning for false positives.

- Device and account integrity signals: device fingerprinting, bot checks, credential stuffing defense.

- Address verification (market-dependent): document proof, data sources, or bank data.

- Case management and audit log: every decision, reviewer action, and evidence artifact must be replayable.

If you are comparing vendors specifically, Spinlab has a separate, deeper guide worth reading: KYC Vendor Comparison: How to Choose Without Killing UX.

A modern AML workflow for iGaming (built for volume)

AML in iGaming is fundamentally an operations system. The workload is continuous, and if you design it like an occasional compliance task, it will break the first time your player base doubles or you add new rails (APMs, instant bank payments, stablecoins).

AML workflow stages (end to end)

Stage 1: Risk profiling (baseline + ongoing updates)

Your AML program should maintain a dynamic risk profile per player. The profile is influenced by identity confidence, geography, payment rails, deposit and withdrawal behavior, and in some models, gameplay patterns.

Stage 2: Screening (sanctions, PEPs, watchlists)

Screening is not a one-time checkbox. Players should be rescreened periodically and on key events (profile changes, large withdrawals, new payment method).

Stage 3: Transaction monitoring and alerting

Alert quality matters more than alert quantity. A scalable system combines:

- Deterministic rules (clear, auditable thresholds)

- Risk scoring (prioritization and queue ordering)

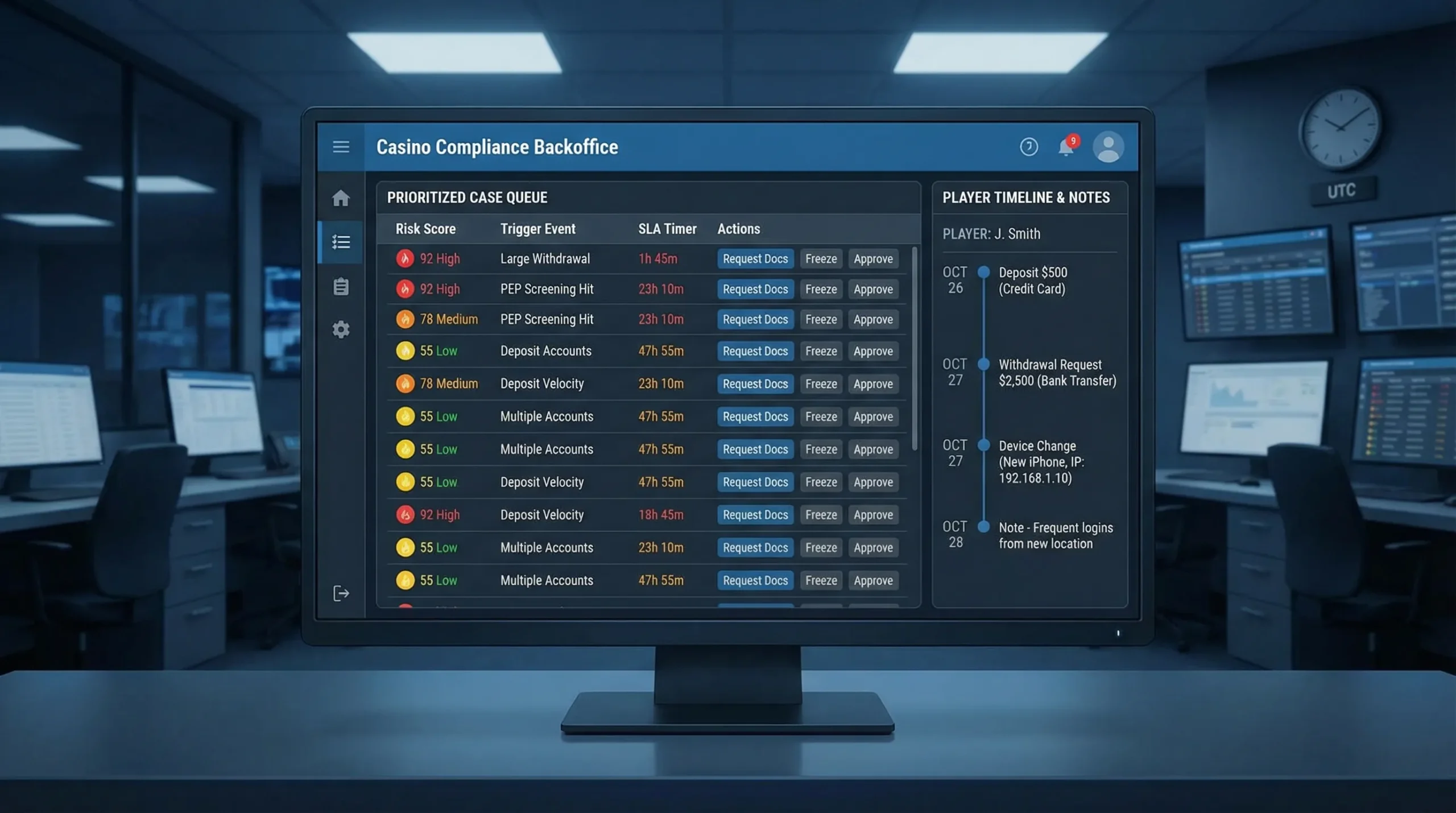

Stage 4: Case investigation and disposition

This is where you need a clean evidence timeline: deposits, withdrawals, game sessions, bonus usage, device history, account changes, support contacts, and any requests for documents.

Stage 5: Reporting and program evidence

Depending on jurisdiction, you may need to file suspicious activity reports and demonstrate that your program has governance, training, tuning, and QA.

Spinlab’s longer operator-focused blueprint on this topic is here: AML for iGaming: Risk-Based Monitoring That Scales.

AML gets harder with crypto (KYT and Travel Rule readiness)

If you accept crypto deposits or process crypto withdrawals, AML needs additional layers:

- KYT (Know Your Transaction) style controls (wallet risk, exposure categories, on-chain patterns)

- Address ownership and wallet allowlists in some risk models

- Travel Rule considerations in regulated contexts

A practical starting point is to map where Travel Rule obligations touch your cashier flows and what minimum data you must store and transmit. Spinlab’s guide: Travel Rule Compliance for Crypto Casinos.

Tools stack: what you need (and what you should demand) from vendors

Most compliance tool purchases fail for one of two reasons:

- The operator buys point solutions without a workflow layer (result: swivel-chair ops).

- The operator buys a workflow layer without strong data contracts and event instrumentation (result: blind spots, weak audits).

Use this tool map to sanity-check your stack.

| Stack layer | What it does | Non-negotiables for iGaming |

|---|---|---|

| Identity verification (KYC) | Document checks, liveness, identity confidence | Mobile-first capture, fast retries, clear failure reasons, low friction pending states |

| Screening | Sanctions/PEP/watchlist matching | Tunable matching, evidence for hits, re-screen triggers, audit logs |

| Fraud and account integrity | Bot, ATO, bonus abuse, mule detection | Low-latency decisioning, device signals, explainable rules, feedback loops from outcomes |

| Transaction monitoring (AML) | Alerts and risk scoring across deposits/withdrawals/gameplay | Real-time or near-real-time, queue prioritization, rule versioning, test harness |

| Case management | Investigations, evidence packs, reviewer actions | Full timeline view, attachments, SLAs, role-based access, immutable logs |

| Reporting and governance | Internal metrics, audit readiness, regulator requests | Exportability, retention controls, permissions, searchable decisions |

Do not ignore third-party risk (KYB) while focusing on KYC

KYC and AML controls can be undermined by weak partners. PSPs, affiliates, game providers, and even support vendors can introduce compliance and settlement risk.

A simple mental model: if you would not buy high-value operational infrastructure from an opaque counterparty, do not integrate a payments or compliance vendor without due diligence. Even outside iGaming, teams apply this instinct when they need trusted logistics and secure checkout, for example when they buy shipping containers online and look for clear inspection standards and payment safety. Apply the same discipline to your casino supply chain.

Workflow design: how to make KYC and AML work together

The fastest route to a broken compliance operation is to treat KYC and AML as two separate queues with separate truth.

A scalable design uses shared primitives:

- A single player identity graph (accounts, devices, payment instruments, wallets)

- A unified event stream (registration, deposit, withdrawal, bonus events, login changes)

- A shared decision log (who decided what, when, based on which version of rules)

A practical operating model (roles and SLAs)

You want clear ownership so cases do not bounce between “compliance” and “risk” indefinitely.

- L1 review (operations): handles straightforward KYC retries, low-risk alerts, obvious false positives.

- L2 review (compliance specialists): handles EDD, complex investigations, source-of-funds requests.

- Financial crime lead (governance): rule tuning approvals, reporting sign-off, regulator communications.

Make the handoffs explicit, and instrument the workflow like any other production system.

Metrics that actually tell you if workflows are healthy

Avoid vanity counts like “number of checks run.” Track metrics that expose friction, quality, and risk:

- KYC completion rate (by device, country, acquisition channel)

- Median and P95 time-to-verified

- False positive rate for screening

- AML alert-to-case rate (too high often signals noisy rules)

- Case aging (SLA breaches)

- Re-review rate (how often L2 overturns L1)

- Loss outcomes (chargebacks, confirmed fraud, confirmed suspicious activity) tied back to signals

Common failure modes (and how to prevent them)

Failure mode 1: “KYC at withdrawal” surprises good players

Many operators delay verification to protect top-of-funnel conversion, then create a trust crisis at first withdrawal.

Fix: design progressive verification with clear UX states, and communicate withdrawal requirements early, especially for higher-risk rails.

Failure mode 2: Static checks in a dynamic, multi-rail world

If your compliance program assumes one geography, one PSP, and card-only deposits, it will collapse when you introduce APMs, instant bank rails, or crypto.

Fix: implement risk scoring that is rail-aware and jurisdiction-aware, with rule versioning and change control.

Failure mode 3: Manual review becomes the product

When automation is low, every spike in traffic becomes a staffing problem, and staffing becomes a compliance risk.

Fix: treat review capacity like a system constraint. Use prioritization, step-up flows, and automation for low-risk decisions.

Where Spinlab fits (platform-level view)

If you are building or re-platforming an online casino, the hardest part is rarely “finding a KYC vendor.” It is wiring KYC and AML into:

- payments (fiat and crypto)

- fraud prevention

- game aggregation events

- backoffice operations

- audit-grade logging

Spinlab is positioned as an all-in-one, modular iGaming platform that supports KYC and AML compliance, advanced fraud prevention, crypto and fiat payments, multi-currency, and an open API for integrations, with a customizable backoffice to run the day-to-day workflows. Spinlab also markets itself as a cost-effective white label option with a Shopify-like operator experience, which matters if you want non-engineering teams to operate compliance without constant developer intervention.

If you are evaluating workflows or planning a new launch, the most useful next step is to map your player journey checkpoints (registration, first deposit, first withdrawal, VIP triggers) and define exactly where you will step up verification, where you will monitor, and what evidence you will retain. Then choose tooling and platform primitives that make those decisions consistent and auditable.

To see how a unified platform can operationalize these flows with integrated payments, compliance, and backoffice tooling, explore Spinlab Studio and request a walkthrough focused on your jurisdictions and rails.