Most AML programs fail in iGaming for the same reason product teams fail when traffic spikes: they were designed for low volume and “reasonable manual review”, then deposits, withdrawals, promos, and payment rails multiply.

Risk-based monitoring solves that by turning AML from a static checklist into a live system that continuously answers two questions:

- Who is riskier right now?

- What action is proportionate, and defensible to an auditor?

Below is a practical blueprint for building AML monitoring that scales with your player base, supports crypto and fiat flows, and stays audit-ready without turning your operations team into a case-management factory.

What “risk-based monitoring” means in iGaming

A risk-based approach is not “do less AML”. It is “do more AML where it matters”.

In practice, risk-based monitoring means you:

- Assign baseline risk based on what you know at onboarding (jurisdiction, product, payment methods, expected activity).

- Continuously adjust risk based on behavior (transaction patterns, withdrawal behavior, bonus abuse indicators, device and account linkages).

- Apply proportionate controls (step-up verification, friction, limits, holds, enhanced due diligence, or reporting) based on that risk.

This aligns with long-standing expectations from global standard setters like the Financial Action Task Force (FATF), and it maps cleanly to modern regulatory trends pushing for continuous, evidence-grade compliance (including tighter expectations in common licensing jurisdictions).

For iGaming, “risk-based” also matters because the risk surface is unusually wide:

- You have high-frequency micro-transactions (deposits, wagers, withdrawals).

- You support multiple rails (cards, APMs, bank transfer, crypto onramps, self-custody withdrawals).

- You operate across borders and often across brands, skins, and domains.

The only sustainable answer is to treat AML monitoring as a real-time decision system, not a weekly report.

The AML data you need (and what many operators miss)

If you want monitoring that scales, start by being explicit about your minimum viable data model. Most teams have KYC and payments, but they underuse gameplay and bonus mechanics, even though those can be decisive for typology detection.

1) Identity and account graph

This is not just “KYC passed/failed”. It’s the graph that links:

- Player identifiers (account, email, phone)

- Document verification outcomes

- Device fingerprints and session attributes

- Shared payment instruments or wallets

If you are not building an identity graph, you will miss multi-account patterns that often sit at the intersection of fraud and AML.

2) Payments and custody events

For fiat, you need deposit and payout events with enough detail to support:

- Velocity and threshold logic

- Source and destination consistency

- Chargeback and dispute linkage

For crypto, you also need the “edges” around the transfer:

- Onramp origin type (custodial exchange vs unhosted wallet)

- Asset type (stablecoins vs volatile assets)

- Address reuse patterns and wallet allowlisting (where applicable)

If you support self-custody withdrawals, monitoring must extend beyond your internal ledger to the withdrawal destination risk model. Spinlab has covered the operational constraints in detail in Implementing Self-Custody Withdrawals Without Losing AML Control.

3) Gameplay, bonus, and promotion mechanics

AML monitoring is stronger when it understands how money actually moves through your product:

- Wagering patterns relative to deposits

- Bonus-triggered activity and clearing behavior

- Low-variance play patterns that look like “throughput” rather than entertainment

This is also where fraud prevention overlaps heavily with AML. Bonus abuse signals can become AML red flags when they indicate structured movement of funds across accounts.

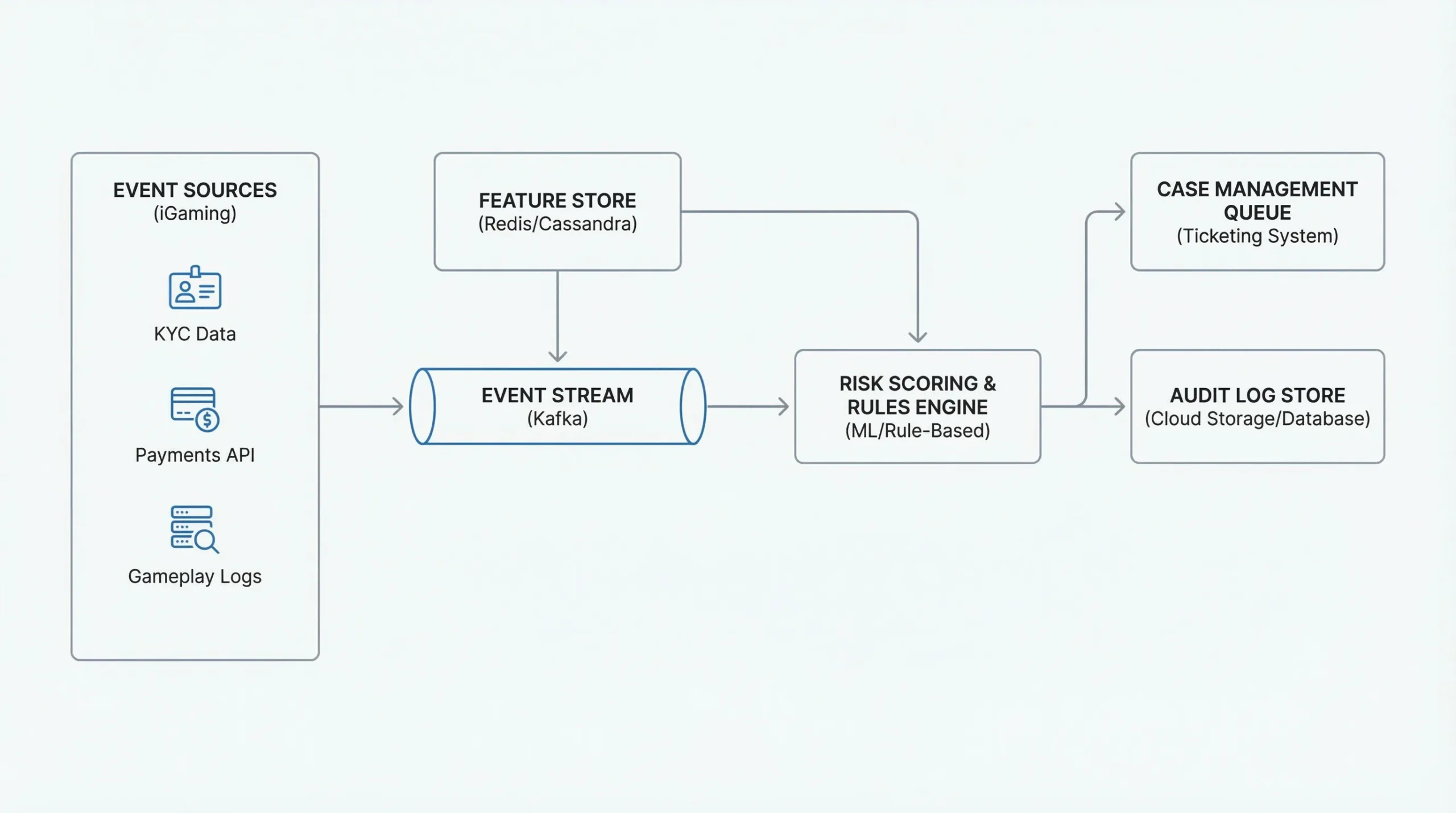

A scalable architecture for AML monitoring

To scale, you need separation of concerns: data capture, decisioning, case management, and audit evidence.

A common anti-pattern is wiring AML logic directly into a backoffice dashboard with manual filters. That feels fast early on, but it becomes unmaintainable as soon as you add new payment methods, new brands, or new jurisdictions.

A scalable reference architecture looks like this:

- Event capture: KYC events, payment events, gameplay events, bonus events.

- Normalization layer: standard schemas, currency normalization, consistent player IDs.

- Feature computation: rolling windows (5 minutes, 24 hours, 30 days), player aggregates, graph features.

- Decision engine: rules plus risk scoring, with explainability.

- Case workflow: queue, SLA, dispositions, attachments.

- Evidence ledger: immutable logs and snapshots for audits.

If you already operate real-time analytics, you have a head start. The key is to ensure monitoring is built on the same event discipline as product analytics, because AML questions are time-sensitive and sequence-sensitive.

For operators using Spinlab’s modular platform, the relevant capability is not “a checkbox called AML”, it’s that compliance, payments, and real-time analytics can live in one system, with an API surface for integrating external vendors when needed.

Designing a risk scoring model that your team can actually run

Risk scoring fails when it becomes either:

- A black box that compliance cannot explain, or

- A spreadsheet that engineering cannot operationalize

A practical approach is a hybrid:

- Deterministic rules for hard stops and must-review events.

- A transparent risk score to prioritize queues and drive step-up controls.

Baseline risk vs dynamic risk

Baseline risk is what you know at onboarding. Dynamic risk is what the player is doing now.

| Risk layer | What it answers | Examples | Typical action |

|---|---|---|---|

| Baseline risk | “How risky is this relationship by default?” | High-risk jurisdiction, payment method mix, business model exposure (affiliate-heavy) | Set monitoring intensity, thresholds, review cadence |

| Dynamic risk | “What changed recently that increases suspicion?” | Deposit and withdrawal pattern shifts, rapid method switching, linked accounts, abnormal wagering throughput | Step-up checks, holds, EDD, case creation |

| Event risk | “Is this specific action risky enough to interrupt?” | Large withdrawal after minimal play, multiple failed deposit instruments, destination wallet risk spike | Block, hold, require additional verification, escalate |

A simple, auditable signal framework

Instead of arguing about exact weights, start with signal categories and clear definitions. The goal is consistency and auditability.

| Signal category | Example signals | Why it matters in iGaming |

|---|---|---|

| Velocity and structuring | Many deposits just under internal thresholds, rapid repeat deposits across rails | Classic structuring pattern adapted to online rails |

| Source and destination inconsistency | Frequent payment method switching, mismatched account holder attributes, new withdrawal destinations | Indicates layering attempts or account compromise |

| “Throughput” behavior | Low entertainment pattern, high turnover with minimal variance, fast cashout after bonus clearing | Can signal funds movement rather than gameplay |

| Network and linkage | Shared devices, shared instruments, linked wallets, affiliate clusters behaving similarly | Helps identify rings, mule networks, and collusion |

| Jurisdiction and product exposure | High-risk geos, cross-border access attempts, unusual location hops | Jurisdictional risk and regulatory expectations |

If you want a broader risk program beyond AML, Spinlab’s Building a Risk Matrix: Prioritizing Threats in Online Casinos is a good companion piece, but AML monitoring should remain laser-focused on actionable typologies.

Monitoring patterns that scale across fiat and crypto

Scalable monitoring is less about “more rules” and more about choosing a small set of patterns that cover most risk, then tuning continuously.

Pattern 1: Fast in, fast out

This is one of the most important patterns operationally because it is also one of the most expensive if you get it wrong.

Common triggers:

- High deposit followed by withdrawal request with minimal gameplay

- Withdrawal immediately after bonus clearing

- Multiple small deposits followed by one consolidated withdrawal

Best-practice response is usually staged:

- Step-up verification or refresh KYC

- Apply proportionate payout holds or limits (depending on jurisdiction and terms)

- Require additional source-of-funds or source-of-wealth evidence for elevated cases

Pattern 2: Rail hopping and method cycling

When players switch between cards, APMs, bank transfer, and crypto rapidly, monitoring should ask “why”. Some legitimate reasons exist (failed approvals, fees), but the pattern is also compatible with layering.

This is where an integrated payments layer helps, because method cycling often looks harmless when each PSP is viewed in isolation.

Pattern 3: Linked-account value movement

In iGaming, “linked” does not always mean “same name”. Rings often use:

- Device reuse

- Shared IP and behavioral patterns

- Affiliate clustering

This is also why KYC and fraud tooling should not live in separate operational silos. A scalable approach uses one shared account graph and lets different teams apply different policies.

Pattern 4: Crypto-specific exposure (without overblocking)

Crypto AML monitoring should not default to blanket friction. It should be risk-based by design.

Practical guardrails include:

- Treat stablecoins and volatile assets differently in monitoring thresholds (your operational risk is different).

- Maintain clear policies for unhosted wallets and for situations where Travel Rule messaging is expected.

Spinlab’s Travel Rule Compliance for Crypto Casinos can help you map where Travel Rule obligations touch cashier flows.

Making the operations team faster (without weakening compliance)

Scaling monitoring is as much an operating model problem as it is a technical one.

Queue design: prioritize by risk and value

If every alert is “high priority”, nothing is.

A scalable case queue typically has:

- P0 interrupt: blocks/holds required immediately (event risk).

- P1 review: must be reviewed within a defined SLA.

- P2 monitor: no immediate action, but watchlist with automated re-triggering.

The key is that each queue has a defined disposition set and evidence requirements, so analysts do not invent their own process on every case.

Tuning cadence: treat AML like a product

Good monitoring improves over time. Set a weekly cadence with three outputs:

- False positive review (what rules generate noise)

- Miss review (what incidents were not caught early)

- Threshold adjustments tied to jurisdictions, payment rails, and promo calendars

A common “scale trap” is tuning monthly, which is too slow for fast-changing promo, affiliate, and payments behavior.

Explainability: every alert must answer “why”

For each case created, store:

- The exact trigger (rule ID or score rationale)

- The feature values that caused it (for that moment in time)

- The player timeline snapshot (deposits, withdrawals, wagering summary)

This is not just for audits. It is what allows your team to tune rules quickly without breaking coverage.

Audit readiness: what regulators and banking partners actually test

When compliance reviews fail, it is often not because the operator had zero monitoring. It is because they could not show consistency and evidence.

Aim to make these questions easy to answer:

- Can you reproduce the decision? Same inputs should yield the same outcome for that historical point in time.

- Can you show who did what and when? Analyst actions, timestamps, and justifications.

- Can you show the policy basis? Why your thresholds and controls are proportionate for your risk assessment.

This is also where “compliance-by-design” trends matter. For example, jurisdictions tightening ongoing monitoring expectations will look for continuous controls, not just onboarding checks. If you operate under Curaçao exposure, Spinlab’s Curaçao Reform 2025: What Operators Need to Change is worth reading alongside your internal AML gap analysis.

A 30-60-90 day implementation plan

You can build scalable risk-based monitoring incrementally, as long as you start with the correct data model and evidence design.

| Timeline | Focus | Deliverables you should have |

|---|---|---|

| 0–30 days | Baseline monitoring foundation | Normalized event schema, baseline risk tiers, first rules for fast in-fast out, case dispositions, audit logging of triggers |

| 31–60 days | Dynamic risk and linkage | Rolling-window features, device and payment linkage graph, risk-score prioritization, SLA-based queues |

| 61–90 days | Automation and resilience | Step-up control automation (limits, holds, refresh KYC), false positive tuning loop, audit-ready snapshot exports, playbooks for incident spikes |

If you are launching from scratch, this monitoring plan should be coordinated with your onboarding funnel design, because KYC friction and monitoring outcomes are linked. For common pitfalls, see 10 Common KYC & AML Mistakes New Casino Operators Make and How to Fix Them.

Frequently Asked Questions

What is AML monitoring in iGaming? AML monitoring in iGaming is ongoing surveillance of player behavior, transactions, and withdrawals to detect suspicious activity and apply proportionate controls.

How is risk-based AML monitoring different from basic AML? Risk-based monitoring adjusts intensity based on player and activity risk, prioritizes alerts, and applies step-up controls dynamically instead of relying on static thresholds.

Do crypto casinos need different AML monitoring than fiat casinos? Yes. Crypto monitoring typically adds wallet and transfer context (custodial vs unhosted, destination risk, Travel Rule touchpoints) and requires policies tailored to crypto rails.

How do you reduce false positives without missing real risk? Use a hybrid approach: keep a small set of high-signal rules, add a transparent risk score for prioritization, and run weekly tuning based on dispositions and incident reviews.

What evidence should be stored for audits? Store trigger rationale, feature values at the time of alert, a timeline snapshot of relevant activity, analyst actions, and policy references supporting the decision.

Build AML monitoring that scales with your casino

If your AML process relies on manual reviews, disconnected payment providers, and after-the-fact spreadsheets, scaling will eventually force a trade-off between growth and compliance.

Spinlab’s modular iGaming platform is built to reduce that trade-off with integrated payments (crypto and fiat), KYC and AML tooling, real-time analytics, fraud prevention, and an open API for plugging in specialist vendors. If you want to see how risk-based monitoring can run as a live system instead of a backlog, explore spinlab.studio and book a walkthrough of the platform.